Global| Jan 07 2014

Global| Jan 07 2014French Households Continue to Struggle

Summary

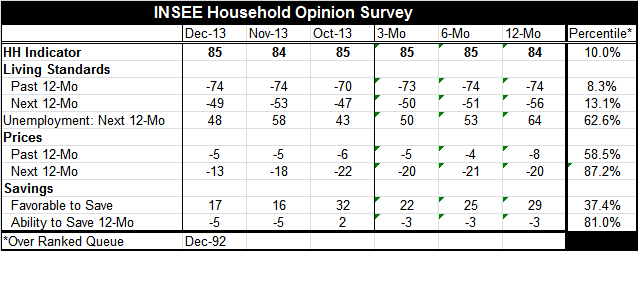

The INSEE French household indicator rose to 85 in December from 84 in November. The reading is the same as its three-month average, its six-month average and only one point above its 12-month average. Consumer confidence in France is [...]

The INSEE French household indicator rose to 85 in December from 84 in November. The reading is the same as its three-month average, its six-month average and only one point above its 12-month average. Consumer confidence in France is stagnant and it is stagnant at a low level.

The INSEE French household indicator rose to 85 in December from 84 in November. The reading is the same as its three-month average, its six-month average and only one point above its 12-month average. Consumer confidence in France is stagnant and it is stagnant at a low level.

At the far right of the table, we get an assessment of the standing of the household indicator. Its percentile standing is 10%. That means the indicator is in the lower 10% of its range and has been stronger than this about 90% of the time. Clearly that is a very poor assessment by French households.

Assessed living-standards over the last 12 months remain steady at -74 in December, the same as November. November had produced a sharp drop from its October reading. However, the living-standard assessment is about the same as it has been over the last three, six, and 12 months. The assessment for the next 12 months improved from -53 in November to -49 in December; that level represents slight ongoing improvements from the 12-month reading at -56. Still, all of these are very weak assessments. The level of the past 12-month response is at an 8% standing. The assessment for the next 12 months, which represents an improvement month-to-month, is still only a bottom 13% standing. French consumers and households are wary of the future even though they expect some slight improvement. One reason for this is that unemployment expectations remain high. Still, there is an improvement in these expectations because the index was at 64 over 12 months and at 53 over 6 months and at 50 over 3 months. It has improved sharply from November's level to a level of 48 in December. However, this is still a 62nd percentile standing for the indicator which means it is above the midpoint of its queue (which resides at 50). Still, it is not a draconian reading; it is just a negative reading.

As for prices the month-to-month assessment is unchanged at -5 at the 58th percentile standing for the past 12 months. Inflation, looking ahead to the next 12 months, is seen as rising to -13 from a level of -18 in November. Its December level is an 87th percentile standing. Inflation expectations over the next 12 months are heightened.

The standing for the response on whether it is favorable to save or not, rose slightly in December compared to November. The November value had halved its level in October. The figure for December at +17 compares to an average of 22 over three months, 25 over 6 months and 29 over 12 months. There has been slow, but clear, erosion in this response over time. The current percentile standing is in the 37th percentile overall; it is not very favorable to save. The ability to save over the next 12 months has been fairly steady over 3, 6, and 12 months and is only slightly weaker in December than those readings. December's reading of -5 is an 81st percentile standing which implies that the expected ability to save is relatively good.

On balance, French consumers and households are not in a very favorable mood. This response fits into the readings we have seen over the past several days updating the French metrics by the purchasing managers on their manufacturing and service sectors. France continues to be the most lagging economy of the large European Monetary Union members. The household indicator is only up-to-date through December, so we can't conclude that much has changed for the consumers or that the outlook has shifted in any way. But the readings on the current assessment as well as for the outlook by the consumer simply seem to put a rubber stamp on the weak readings we have seen from the manufacturing and services sectors. All in all, they indicate a poor environment for policymaking in France.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief