Global| Mar 27 2015

Global| Mar 27 2015French Households Begin to Feel Better... But Not Well

Summary

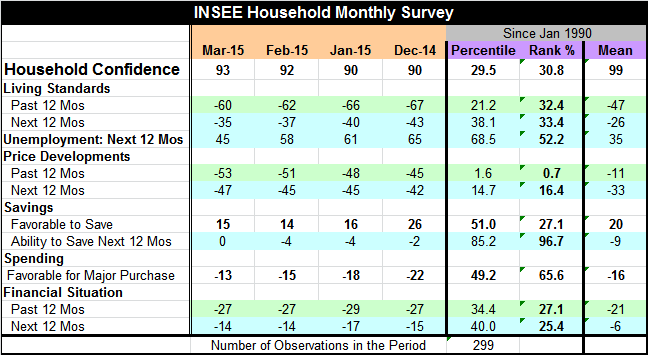

The French household confidence reading has been stuck in a range of mostly the mid- to high-80s from August 2012 through November 2014. In just the last four months, the household indicator has broken out. Its reading of 93 is the [...]

The French household confidence reading has been stuck in a range of mostly the mid- to high-80s from August 2012 through November 2014. In just the last four months, the household indicator has broken out. Its reading of 93 is the highest since a one-month higher reading in November 2010. But early-2010 was the last time that there was more than just one month in a row with a higher reading and only data before January 2008 show readings that persisted at a high level. If household confidence can advance by one more point on this indicator and hold the gain, it will be back to its pre-crisis level.

The French household confidence reading has been stuck in a range of mostly the mid- to high-80s from August 2012 through November 2014. In just the last four months, the household indicator has broken out. Its reading of 93 is the highest since a one-month higher reading in November 2010. But early-2010 was the last time that there was more than just one month in a row with a higher reading and only data before January 2008 show readings that persisted at a high level. If household confidence can advance by one more point on this indicator and hold the gain, it will be back to its pre-crisis level.

Having said that, this is still not a terribly solid reading for confidence. But any journey begins with a single step and France is finally taking steps in the right direction. It must start from where it is which is at a really depressed level. Still, some of the confidence components are making more considerable strides.

Household confidence at a level of 93 is below its mean (99) and stands only in this 30th rank percentile. That means the indicator is weaker only 30% of the time.

The assessment of living standards is also weak in its lower 32nd rank percentile and the outlook for the next 12 months is only at its 33rd rank percentile. But the assessment of living standards has risen by seven points in the last four months and the outlook has improved by eight points, putting momentum in the right direction.

Expected unemployment has a 52nd rank percentile standing which is still above its mean (diffusion value of 35) and it means that the prospect for unemployment is approaching a neutral historic level (the 50th percentile). Still, this is an advanced stage of the business cycle expansion and the expected unemployment standing should be far below its median- not close to it or barely above it.

The assessment of price developments still shows that current and expected inflation are at an extremely low level. Past inflation is assessed as having been lower only 0.7% of the time while expected inflation is lower only 16% of the time. So some let up of disinflation pressures is expected, but inflation is still expected to be historically quite low.

Consumers are expecting some let up in economic pressure as well as the ability to save is assessed as only harder 27% of the time while ahead the ability to save is assessed as only easier 4% of the time. That is a huge switch.

The environment for spending is assessed as one of the stronger readings. At a -13 raw diffusion reading in March, it is above its mean of -16 and stands in the 65th percentile of its historic queue of data. That means the spending environment is better only about 35% of the time. That should put the French consumers in a position to help move the recovery ahead - at least if these expectations turn out to be true.

One fly in the ointment is the same one we see in the U.S. The past and future financial situation is assessed as being a bottom 27% to 25% conditions. The financial situation is worse only about one-quarter of the time. In U.S. readings consumers are saying the same thing; their concerns about their financial situation or that they have weak income expectations. It's a global problem, not just a French problem.

Consumers and workers in the most developed nations have had their jobs taken away by firms that moved to lower wage countries to set up production. This has reduced the opportunities for employment and reduced the attractiveness of the opportunities that remain there. Meanwhile, because China and other fast-developing countries have set their plans for growth to mine the domestic demand in the higher income countries, the financial crisis, the slowdown and the structural change it all caused has diminished their ability to grow in that way anymore. Hence even the former fast-growing countries are having problems maintaining their growth.

There is a worldwide problem of excess supply and insufficient demand and we see the blow-back from it in consumer surveys. While conditions in France are improving, the absolute conditions are still quite bad for this stage of a business cycle recovery. The pace of progress has been very slow. Moreover, there has been no sorting out of the forces that brought this condition of excess supply into being. And since those forces are still at work, it is making recovery that much more difficult to take hold. While I am not a recovery pessimist, I think that the `risk' of global growth accelerating significantly is quite low. Monetary policy is about tapped out and there is still little risk that inflation will be created. Fiscal policy has been overused and is not an option. Trade policy is at the root of the problem and countries are not talking about it. This is a global story and problem, but it is affecting France as much as anywhere.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief