Global| Mar 09 2010

Global| Mar 09 2010French Deficit Shrinks

Summary

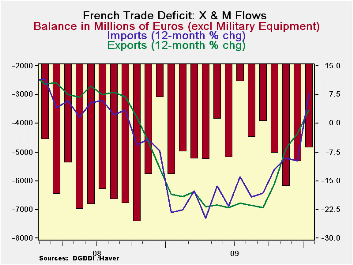

French exports and imports show a classic impact on those two flows as the domestic and global recessions hit. Now that recovery is in gear, the trade flows reflect that as well. Exports and imports plunged at the onset of the [...]

French exports and imports show a classic impact on those two flows as the domestic and global recessions hit. Now that recovery is in gear, the trade flows reflect that as well. Exports and imports plunged at the onset of the recession, imports fell because French domestic demand shriveled up; exports contracted because foreign demand shut down. The impact on the balance of trade was erratic. Generally, however, the size of the French goods trade deficit was reduced. But late in 2009 the trade deficit began to surge again reaching a monthly maximum (deficit) of over €6bln. But over the last two months this bulge in the deficit has diminished.

Exports have outpaced imports Yr/Yr, nearly doubling the growth rate of imports. Over six months exports contracted as imports began to surge. But over the last three months exports are back solidly outperforming imports, helping to shrink the French deficit.

The Yr/Yr trends in the chart tell a broad-brush story of surging trends. Both exports and imports are on a clear and solid upswing over that period. Over shorter periods export and import growth both are more chaotic. But the year-over-year statics tell a clear story of an international sector in rebound. Trade figures across the globe echo these same trends. Trade flows tell a story of an international economy in a clear state of rebound not a story of tentative and sputtering domestic growth which is the story we are often fed about the various national expansions. Why do the trade data speak clearly to the subject of revival while various national data do not? It is because the goods sector which dominates trade is in a clear rebound while the services sector, the sector that dominates job growth domestically, has been slow to catch on. To make the various national recoveries durable, services industries have to catch on and job growth must get into gear.

| French Trade trends for goods, Excl Miliarty Equip | |||||

|---|---|---|---|---|---|

| m/m% | % Saar | ||||

| Jan-10 | Dec-09 | 3M | 6M | 12M | |

| Balance* | -€ 4,863.00 | -€ 5,346.00 | -€ 5,472.67 | -€ 4,983.00 | -€ 4,756.25 |

| Exports | |||||

| All Exp | 2.7% | 0.4% | 19.5% | -3.4% | 7.6% |

| Food, Bev &Tobacco | -2.6% | 0.8% | 14.5% | -4.4% | 0.5% |

| Transport Equip | 8.4% | 6.2% | 16.2% | -8.7% | 26.6% |

| Other Exp | 1.7% | -1.2% | 21.3% | -1.4% | 3.5% |

| IMPORTS | |||||

| All IMP | 0.9% | -2.1% | 13.9% | 11.1% | 3.6% |

| Food, Bev &Tobacco | 0.5% | -0.2% | 7.8% | -4.7% | -2.8% |

| Transport Equip | 0.1% | -0.9% | 12.0% | 13.1% | 11.5% |

| Other Imp | 1.1% | -2.5% | 14.8% | 12.3% | 2.6% |

| All data seasonally adjusted *Eur mlns; mo or period average | |||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief