Global| Mar 26 2013

Global| Mar 26 2013French Consumer is Still Flat

Summary

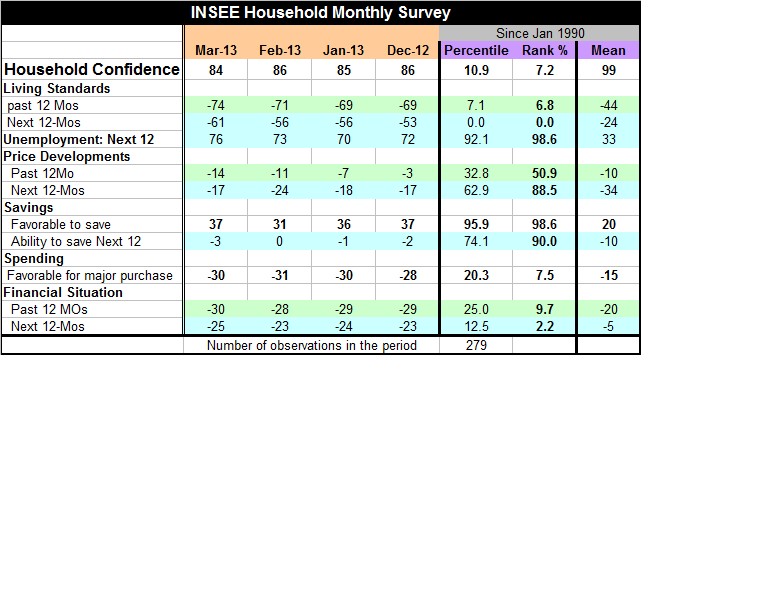

France's household confidence according to the INSEE statistical agency fell by two points in March to a level of 84 from a level of 86 in February. At its March level confidence stands at about the 7th percentile in its historic [...]

France's household confidence according to the INSEE statistical agency fell by two points in March to a level of 84 from a level of 86 in February. At its March level confidence stands at about the 7th percentile in its historic rank. That means that it has been higher about 93% of the time. Going back to 1990 the average for this measure has been 99 compared to the current reading at 84.

France's household confidence according to the INSEE statistical agency fell by two points in March to a level of 84 from a level of 86 in February. At its March level confidence stands at about the 7th percentile in its historic rank. That means that it has been higher about 93% of the time. Going back to 1990 the average for this measure has been 99 compared to the current reading at 84.

The survey assesses living standards, unemployment, price developments, savings, spending and the financial situation of French households. All of these readings are weak and are consistent with ongoing intensifying weakness in the French economy.

Living standards of the past 12 months have fallen to a level -74 compared with a reading of -71 in February; back in January December this reading was at -69. At the March level, living standards are assessed to have been so low over the past 12 months that historically they had only been worse about 7% of the time. Looking at living standards over the next 12 months the assessment falls to -61 from a -56 in February. At this level France is looking at the weakest reading ever for expected living standards over the next 12-months back to 1990.

The survey assesses households' expectations for unemployment over the next 12 months. This reading has been steadily stepping up. In March the raw reading moved up to 76 from 73 in February; in February it moved up to 73 from 70 in January. At its March level unemployment expectations are in the top 2% of their historic queue or rank. That means that expectations for unemployment have been worse only about 2% of the time going back to 1990. This is a very bad reading. The average reading for unemployment expectations has been in the neighborhood of 33 that compares to the current raw reading at 76 in March.

The survey on price developments shows deterioration over the past 12 months to a reading of -14 from -11 in February. The past12-months reading of -14 compares to -3 in December. Price developments over the past 12 months sit more or less in the middle of the historic range for that category. Looking to the next 12 months ahead, the reading has improved to a value of -17 from a value of -24 in February. The March reading is relatively high when compared the history of the series, standing the top 12% of all historic observations. So while inflation has been subdued there are concerns about what inflation will do in the period ahead - even in the face of the zone-wide push for austerity. This reading seems to suggest French households do not believe that the push to austerity will be long-lived.

The savings responses are quite positive. Households responded by indicating that it's a favorable environment in which to save. The response "favorable to save" went up to 37 in March from 31 in February. At that level it's back to its December value. In terms it's ranking it's in the top 2% of its historic responses. The ability to save in the next 12 months is assessed at a -3 a slight drop from February. This reading is also relatively strong by the standards of this component. The -3 reading stands the top 10% of its historic range. If the environment is favorable for savings it's not favorable for spending. Consumers can do two things with the money (income) they earn: save it or they can spend it. We saw the same sort of thing in the Italian survey that had an explicit purchase metric and it weekend when the saving response rose. So too, the French survey has an explicit spending metric. And we see this metric moving opposite to the direction the savings is moving as we would expect. The assessment of the favorability for spending actually improved slightly month-to-month but remains at a very weak -30 reading. That reading stands in the bottom 7% of its historic range implying that the environment for spending has been worse than this only about 7% of the time. This reading fits nicely with the readings for savings. Household is saying it's a favorable time to save and because it's a favorable time to save it is an unfavorable time to spend and that's exactly what were hearing from the Italian consumers as well.

The financial situation over the past 12 months and for the next 12 months both slid in March compared to February both series are weak. For the past 12 month period, the standing of the response is in the bottom 10 percentage points of the historic range of that component. While expectations are even worse, residing in the bottom 2% of their historic range for that component.

It's hard to say if there is any fall-out in France from the situation in Cyprus. The French survey from INSEE is for March. The Cyprus bank closure occurred on March 15, in the middle of the month. When the closure first happened it was looked upon as a Cyprus problem, the same as the Greek situation is/was looked upon as a Greek problem. But as the euro group and the Troika began to negotiate with Cyprus the sorts of things that began to be proposed, and that were eventually rejected, broadened the impact of Cyprus. A small Cyprus now looms large as a potential template for what might be done elsewhere. While the Dutch finance minister said exactly that he later recanted arguing that it was no template and that Cyprus was a special case. Of course, if it's a template that approach will put bank crises on a hair-trigger as even the whiff of one will send depositors scurrying elsewhere creating a self-enforcing run on the bank. But then the Dutch minster recanted saying that Cyprus is a special case and not a template. Of course, Greece was a special case. Of course, Spain and Portugal will be special cases. Certainly Italy is a special case. Ireland was a special case and it would like to have its case reviewed and its treatment improved compared to the sorts of treatment that has been given other countries.

One problem with the European monetary union is that everything is a special case. Europe needs to set a procedure that can be understood instead of persisting in one that is constantly in flux and is misunderstood. It needs to think about what its approach should be so it doesn't stumble and lead investors to suspect that pro-cyclical policies are in play that will make crises more likely

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief