Global| Oct 28 2020

Global| Oct 28 2020French Consumer Confidence Slips

Summary

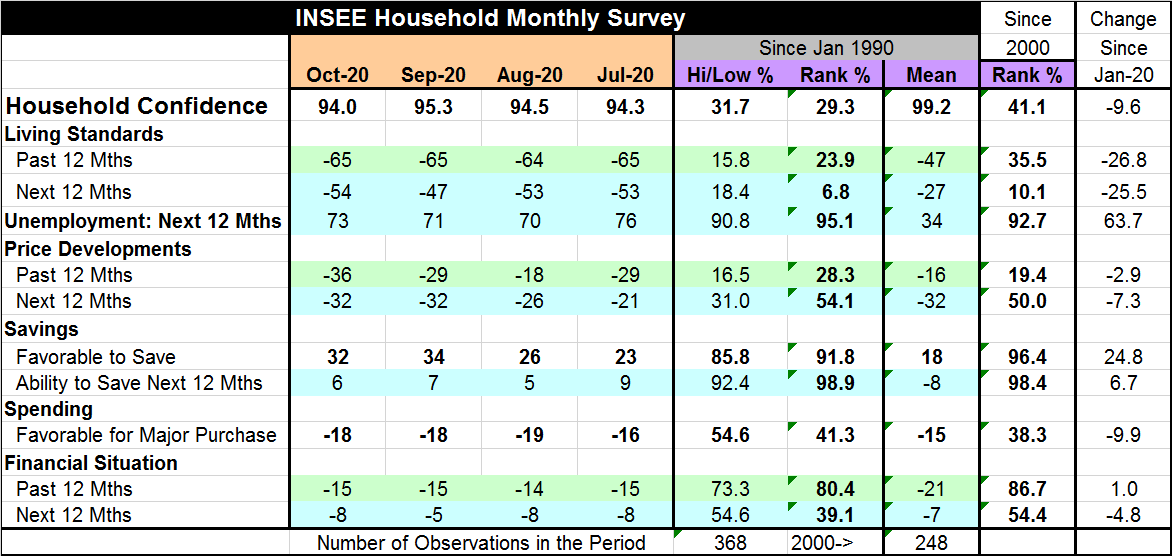

The French household sector assessment edged lower in October as it fell to 94.0 from September's 95.3 reaching its lowest level since May 2020. Confidence has a ranking in its lower 41.1 percentile on data back to 2000, marking [...]

The French household sector assessment edged lower in October as it fell to 94.0 from September's 95.3 reaching its lowest level since May 2020. Confidence has a ranking in its lower 41.1 percentile on data back to 2000, marking confidence as below its median value for that period. Compared to January 2020, just before the coronavirus struck, household confidence is lower by 9.6 points.

The French household sector assessment edged lower in October as it fell to 94.0 from September's 95.3 reaching its lowest level since May 2020. Confidence has a ranking in its lower 41.1 percentile on data back to 2000, marking confidence as below its median value for that period. Compared to January 2020, just before the coronavirus struck, household confidence is lower by 9.6 points.

Living standards over the past 12 months are assessed as barely changed over the last four months; during this period, they are evaluated to have been in the lower 35.5 percentile of their historic experience. Looking ahead after a false improvement in September, there is erosion to a -54 diffusion value which corresponds to a 10.1 percentile standing- extremely weak. Both past and expected living standards have slipped by about 25 points from their respective January levels. France is feeling the pain of a second wave.

Despite substantial help and protection from the government, expectations of unemployment rank in their 92.7 percentile and the survey response value has rising by 63.7 points since January. Unemployment expectations have crept up in the last two months but are below where they stood in July. It is an unsettling situation especially with the virus expanding again in France and lockdown responses spreading widely. France also combats a growing anti-Islam mood after a French teacher was beheaded for discussing in his class and showing a cartoon of the Prophet Muhammad.

Both past and expected prices development are weakening and have weakened especially in the last two months. Past price developments have a 19.4 percentile standing while expected price developments have a higher, 50 percentile standing, right on their median value. Past price developments have slipped by only 2.9 points from their January value while expected prices developments have fallen by 7.3 points from their January value.

Respondents evaluate the time as favorable to save and rate their ability to save strongly as well. Both rank in the top 2-4 percentiles of their respective historic queues of value back to 2000. The favorable to save response slipped a bit this month but had been rising; it is 24.8 points above its January level. The ability to save which is a forward-looking assessment has weakened, but it is still higher by 6.7 points than its January level. With lockdowns of various sorts in place, it is simply much harder to spend any money!

The spending assessment for making a major purchase is little changed over the past three months. It has a well below median 38.3 percentile standing in October and is nearly 10 points lower from its January level

Assessments of the financial situation both past and expected have changed little over the past four months. However, the past assessment has a much higher, 86.7 percentile standing, while the future assessment has a much lower, but still above median, 54.4 percentile standing. The past response is one point higher than it was in January while the look-ahead response is 4.8 points lower.

The small table below compares the INSEE rankings for the Household, Services and Manufacturing sectors from January to October, monthly. Two of three evaluations show a sharp fall in March (exception: household) and a sharp fall in April (no exception). Condition assessments remain extremely depressed though July. In August there is some pick up the service sector that lasts through September but then falls back in October. Manufacturing continue to build and improve in September, holding most of those gains in October. The household evaluation gets back to a ranking of 47.2 in September, its highest since June, but then slides back to 41.1 in October.

The second wave

The second round of the virus is now fully enfolding France. As August began, France had logged 187,919 cases of COVID (Source here). At that time, the curve of cases was starting to rise. By September 1, the case load had risen to 286,007. By October 1, it was up to 577,505; by October 27, that had climbed to over a million cases at 1,198,695. In early-September, France began to have a daily infection rate that surpassed its peak rate of April. That began to ring some alarm bells. From that date, the infection spread took hold and has risen sharply leading to a series of moves to suppress the spread. On October 25, the daily infection rate surpassed 52,000 per day, but in the last two days that reading has diminished. Still, France clearly is in the middle of a very disruptive virus situation. It can be expected to continue to weigh on economic data.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief