Global| May 27 2016

Global| May 27 2016French Consumer Confidence Last Higher Eight and One Half Years Ago

Summary

Although household confidence was last higher eight and one-half year ago, it was exactly this high back in January of this year. Viewed on a much broader horizon, the current confidence readings sit only at the 50.8th percentile of [...]

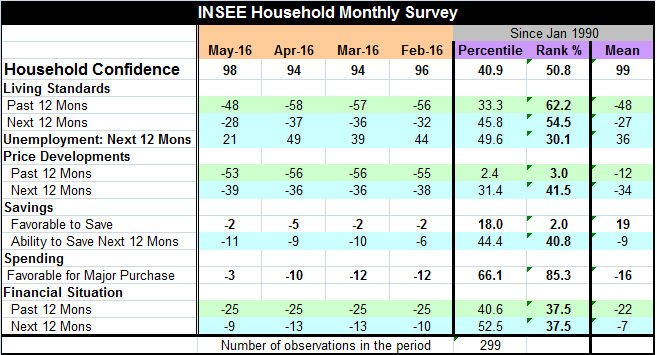

Although household confidence was last higher eight and one-half year ago, it was exactly this high back in January of this year. Viewed on a much broader horizon, the current confidence readings sit only at the 50.8th percentile of their historic ranking of observations, a very thin margin above their historic median. So this report is somewhere between (1) ho-hum back to January, (2) wow- only better eight and one-half years ago and (3) shucks only basically a middling result. That about sums up the way the French economy has been behaving.

Although household confidence was last higher eight and one-half year ago, it was exactly this high back in January of this year. Viewed on a much broader horizon, the current confidence readings sit only at the 50.8th percentile of their historic ranking of observations, a very thin margin above their historic median. So this report is somewhere between (1) ho-hum back to January, (2) wow- only better eight and one-half years ago and (3) shucks only basically a middling result. That about sums up the way the French economy has been behaving.

French workers fight for the status quo

France is currently being wracked by strike and labor market actions meant to bring the economy to its knees as labor market reforms are being opposed in the usual French way. When agriculture is involved, you can expect farmers to drive their tractors to the streets of Paris and to dump various and sundry noxious things on the roads to block them. Sometimes workers press a national air strike or rail strike or both together. France seems to rely on this sort of internal economic terrorism to resist change.

However, France, like the U.S. and everyone else, is part of this big global and increasingly interlinked economy and everybody's way of doing business is going to change as a result. Maybe this is really as good as things are going to get (the eight and one half year high). Maybe the notion that this is only a median reading will be shelved because the old levels of confidence will never be seen again and are no longer relevant as standards for comparison.

The survey's nuts and bolts

The one high-ranking response in the survey is the 85th percentile standing that conveys the sense that it is a good time to make a major purchase. Similarly the prospect for unemployment is moderately low with only a 30th percentile standing (a low probability of unemployment is good- so a low ranking is good). The probability of unemployment continues to work its way lower this month with a sharp drop in expectations for unemployment - better than halving the reading for April. Unemployment fears have not been this low since mid-2008.

Expectations for inflation are still quite moderate with expectations over the next 12 months slipping even lower. They have drift back to their January level and were last weaker in the early months of 2015.

The past and future financial situations both are rated as 37th percentile events. Expectations for the next 12 months improved significantly month-to-month to advance that standing while the assessment of the past 12 months has been stuck at a raw diffusion score of -25 for some time. The expected financial situation was last assessed as stronger in December-January at the turn of the year. But to find another episode of such a `strong' reading, we have to go back to late-2009 (one brief reading) or to late-2007 to see consistently better expectations than this.

Old dogs don't want new tricks... neither do new dogs

On balance, French households are feeling somewhat better. However, the French labor market activism that we see in progress also speaks of workers pushing back to try and keep their lifestyles from undergoing certain erosions. President Hollande has said he would not give in but the Prime Minister Manuel Valls has left the door open for some backtracking. Of course, one man's reform is another man's burden. The French government has proposed to allow employers to fire employees under 26 years of age without having to show cause. And this new rule has created great upset. Other provisions are meant to enhance labor market flexibility. But again when firms cut overhead, one man's overhead is another man's under-neck. Be careful where you cut and what you cut.

Lack of competiveness is the root cause of the malaise

Europe continues to struggle to get growth on track. Despite the low interest rates (negative yields!), we do not see a thousand flowers bloom. The bloom is off this rose because in France -like the U.S. and many other more highly developed -high-income nations do not have a lot of private sector investment project that make sense in a world where they are competing with cheap labor in China, Mexico, Vietnam, or just nearby in Eastern Europe.

The punch from the invisible hand always lands

Governments cannot legislate prosperity. Neither can labor movements impose a circumstances that will dominate international realities. Economic forces will penetrate the fog of attempts to feather-bed or otherwise keep employment levels higher than economic realities demand.

A true life story where no one wears a white hat

I am reminded of a story I saw last year of an Italian firm whose owner began shipping his factory parts off to Romania when his own workers were all on summer holiday. One worker happened to drive by the plant saw the trucks being loaded with equipment, and called other employees who came and formed a line to prevent the last of the trucks from leaving. The firm's owner was not repentant. While I don't defend him, he logically noted that he could not get wages rolled back and could not fire people. He was losing money. He would lose everything if he kept on the way things were and he could not change things. So he had no choice but to protect his investment and to move the firm to where he could be competitive. This real world anecdote sums things up. Pity the worker who came back from summer vacation to find their job gone. But pity the owner left to slowly bleed to death because labor will not renegotiate a deal that has no economic merit. There are no good guys or bad guys in this story. There are only economic realities. And the realities must be faced. In the U.S., many firms have just pulled up stakes because they can and it makes sense for their own survival. Not one in the U.S. has a clue what to do.

The G7, trade, protectionism and inaction

Trade and protectionism was big topic at the just concluded economic summit in Japan. But the leaders found no real common ground and offered nothing but platitudes. The problem now is that there is too much supply and not enough demand globally. Many countries still want to develop faster and to them it means to produce more at lower wages and to sell goods abroad. The ability for those markets `abroad' (i.e., in high income high wage countries) to absorb more goods is reaching saturation and being undermined by the market penetrations of those developing and exporting countries since they are taking jobs away from the high income nations. This clash is exposing the contradictions between the ideal of development and the operative development models being used in an economic system that does not really rationalize itself. The old model of developing countries' bootstrapping themselves by servicing richer countries needs is coming to an end. You can see it with China realizing it must develop its own domestic demand. But other countries are still on the old path. There is nothing but trouble there. And France is nose to nose with that trouble today.

France is feeling the same pain as we are in the U.S., but it has different symptoms. Don't expect the pain to go away either here or in France. Our pain is here to stay.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief