Global| Mar 28 2016

Global| Mar 28 2016French Consumer Confidence Hits 7-Month Low; It Was Last Lower One Year Ago

Summary

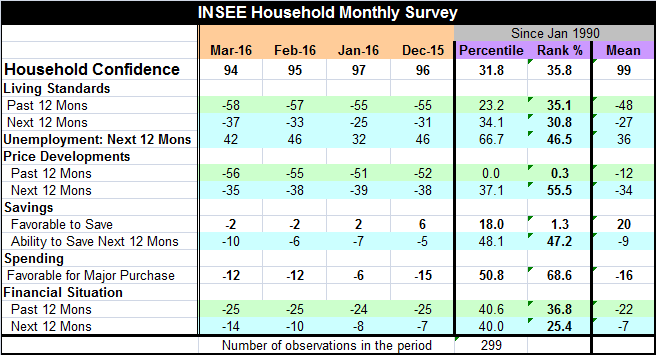

French consumer confidence fell to 94 in March from 95 in February. The index has a weak 35th percentile standing at its March level (it is this weak or weaker 35% of the time). Living condition assessments for the past 12 months as [...]

French consumer confidence fell to 94 in March from 95 in February. The index has a weak 35th percentile standing at its March level (it is this weak or weaker 35% of the time).

French consumer confidence fell to 94 in March from 95 in February. The index has a weak 35th percentile standing at its March level (it is this weak or weaker 35% of the time).

Living condition assessments for the past 12 months as well as those expected for the next 12 months slipped in March. The past 12-month response holds a 35th percentile standing; the next 12-month has a 30th percentile standing. However, improving were unemployment expectations as that response index fell to 42 in March from 46 in February to a 46th percentile standing- below its median value (which occurs at a 50th percentile ranking). The fear of unemployment is fading.

The response for `favorable to save' stayed at -2 at an extremely weak 1.3 percentile standing. The ability to save response fell to -10 in March from -76 previously to post a 47th percentile standing.

The spending environment stayed at its -12 reading and at a 68th percentile standing.

Households rate their financial situation as unchanged at -25 for 12-months ago, the same as they did last month. For 12-months ahead the index fell to -14 from -10 in February. The standing of the 12-month ago index is in its 36th percentile while for 12-months ahead there is a 25th percentile standing index. Both are weak.

Summing up the survey results

On balance, household responses to the survey questions this month are poor. The overall index slipped by just one point in March, but that is after slipping by two points one month ago. There is a two-month string of losses. Still, the overall index has been in a range of 94 to 97 since April 2015. In March 2015, one year ago the index was busy transiting to a higher level as it reached 93 after having been as low as 86 just five short months before that. The chart shows the string of strong increases then followed by the more recent move to an even higher level and the very recent step-down from that. While the recent upward momentum is `still mostly in-place', the problem is that even on that optimistic assessment of momentum, the levels for household confidence are still extremely low. On balance, that leaves little to like in this report apart from the reduced probability of unemployment that households see. They find that they are `worse off' in a variety of ways but have much of a fear of the ultimate loss, that of their jobs. And that counts for something.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief