Global| Jul 23 2013

Global| Jul 23 2013French Businesses Are More Upbeat - Do They Know Something?

Summary

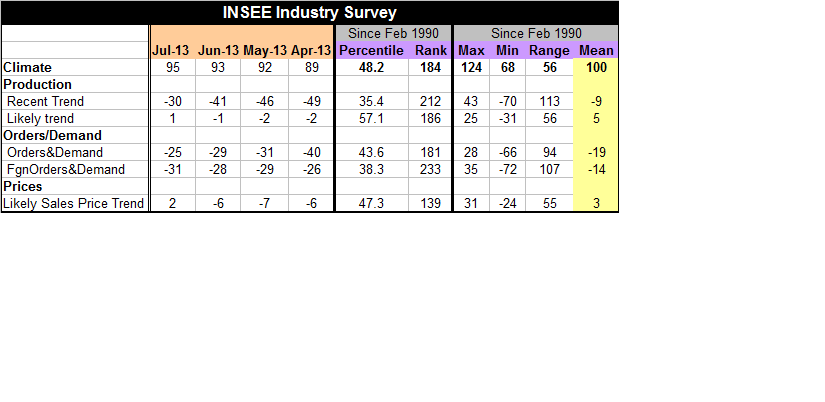

French business climate improved by two points in July, with the index rising to 95 from 93 in June. The standing of the index is its highest in 15 months. The reading for the recent trend improved much more sharply to -30 in July [...]

French business climate improved by two points in July, with the index rising to 95 from 93 in June. The standing of the index is its highest in 15 months. The reading for the recent trend improved much more sharply to -30 in July from -41 in June. The reading for the 'likely trend' switched over into positive territory, registering a plus-one reading in July after a -1 reading in June. That's the first positive reading since February of this year although still it's below the February level.

French business climate improved by two points in July, with the index rising to 95 from 93 in June. The standing of the index is its highest in 15 months. The reading for the recent trend improved much more sharply to -30 in July from -41 in June. The reading for the 'likely trend' switched over into positive territory, registering a plus-one reading in July after a -1 reading in June. That's the first positive reading since February of this year although still it's below the February level.

Orders and demand improved to a -25 reading from -29 in June, making it the strongest reading since September of last year. Conversely, foreign orders and demand deteriorated, slipping back to -31 from -28 in June. Apparently the improvement in France is home-grown. The foreign orders and demand reading is the weakest the since January of this year.

Despite the widespread improvement the French metrics remain. The industry climate index sits in the 48th percentile of its high low range since February 1990. But if we position it in its rank of observations historically: its standing is still barely above the bottom third of its historic queue of values sitting at the 34.8 percentage point of its ordered queue (that is to say, that it is weaker than this only about 35% of the time). Similarly the 'recent trend' standing is in the 25th percentile of its ordered queue, the 'likely trend' is in the 34th percentile of its ordered queue. Orders and demand are in the 36 percentile of their ordered queue with foreign orders and demand much weaker in the lower 17th percentile of their ordered queue. The data for France are showing some near-term life but the readings continue to be weak in historic context. But that has to be clear from plot in the chart.

There are other signs of improvement in the euro-Zone, although none of them really help us to understand why French business confidence is improving. The Bank of Spain for example still sees recession but sees recession forces abating in the second quarter. In the UK exports are giving off the strongest reading since the recession according to a survey of UK exporters.

However, debt to GDP ratios are still rising in the European Monetary Union as a result of austerity. Austerity has continued to drive up debt demands across the euro-Zone while the straitjacket of austerity has prevented growth from restarting thereby making debt to GDP ratios even worse (higher).

Globally a new plan announced by China to try for public works programs that will employ some of its domestic industries that are the slackest, was greeted well by markets yesterday.

On balance we welcome these signs of improved activity in the euro-Zone and in France. The improving survey in France adds to some signals from the PMI surveys of manufacturing and services improvement there that tell us also that the extent of weakness is abating.

The July reading for services industries and for manufacturing industries each separately improved in in France. It's another encouraging signal for the French business sector. However, the household sector, where data lag by one month and are currently only available through June does not show the same sort of improvement. The index of household confidence slipped in June by one point compared to May after May fell by four points from April's level. While overall business confidence might be the highest in 15 months, compared with its level of one year ago, the household confidence index, at 78, is well below its value of 90 from one year ago. French businesses are feeling better without engendering any improved feeling of well-being on the part of households. Indeed, household rankings back to January 1990 are the weakest on record as are the statistics on living standards for the past and future 12 months. French consumers continue to evaluate their financial situation extremely poorly. The environment for spending is in at least the bottom 10 percentile of what it's been historically.

Against this background, while it is encouraging to see some improvement in the attitudes of French businesses it's unclear where that comes from or how long it can last. Apparently it isn't underpinned by improved foreign demand, judging from responses in the survey itself. Clearly it's not improved because of improved domestic spending conditions or household confidence. Since we continue to get reports of extremely difficult international trading conditions it's hard to imagine that France, given its competitiveness challenges, is doing better on the world stage of competition. And the French fiscal deficit and deficit outlooks is poor enough that it's really not possible for the French government to make any additional promises to French business to ineffectively underpin improved attitudes. While I don't doubt the results in the French business survey, I have to declare that I can't completely understand what they're based on. I feel much more comfortable understanding them with regard to how low they are in their historic standing rather than gaining any comfort from the degree to which they've improved in recent months.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief