Global| Jul 23 2014

Global| Jul 23 2014French Business Climate Struggles

Summary

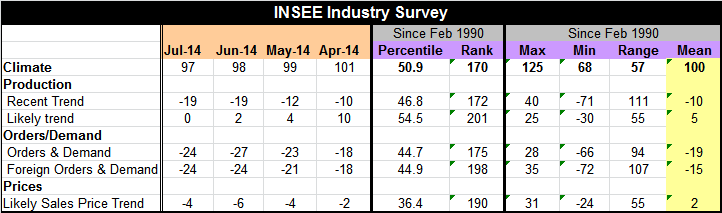

The French business climate indicator from the INSEE survey fell in July, continuing a streak of erosion. The indicator was last lower in September of last year. It sits in the 39th percentile of its historic queue of data back to [...]

The French business climate indicator from the INSEE survey fell in July, continuing a streak of erosion. The indicator was last lower in September of last year. It sits in the 39th percentile of its historic queue of data back to February 1991. The French climate indicator is weak and on a continuing path of erosion. It has fallen for three consecutive months. However, the metric is still 2 points higher than it was one year ago- but it is slipping.

The French business climate indicator from the INSEE survey fell in July, continuing a streak of erosion. The indicator was last lower in September of last year. It sits in the 39th percentile of its historic queue of data back to February 1991. The French climate indicator is weak and on a continuing path of erosion. It has fallen for three consecutive months. However, the metric is still 2 points higher than it was one year ago- but it is slipping.

The recent trend for production is at a reading of -19 in July. At that level, the reading stands in the 39th percentile of its historic queue and compares to an average reading of -10.

The likely trend has a value of zero, which seems stronger. But, in fact it is weaker; it stands in its 28th percentile and compares to an historic average of 5.

Orders and demand improved to -24 in July from -27 in June. The July value stands in the 37th percentile of its historic queue. Foreign orders and demand are similarly weak with an even weaker queue standing in the 29th percentile of their queue.

The likely sales prices trend rose to -4 in July from -6 in June. It stands in the 32nd percentile of its historic queue.

On balance, France is still struggling. Manufacturing is still weak and a similar survey for manufacturing finds the likely trends for that sector assessed at the 26th percentile, an extremely low reading. French manufacturing is really struggling.

The French services sector is similarly weak with its climate indicator standing in the 36th percentile of its historic queue, virtually as weak as business overall and as weak as manufacturing. The outlook for sales in the services sector is weak, below the 40th percentile of its historic queue for that metric.

The French surveys are consistent in their assessment of branding the economy as weak and floundering. There is no uptrend to speak of in any of the sectors.

France remains the weak man of Europe and it is also the second largest economy in the euro area. It is hard to see how France is going to dig itself out of this hole. All of Europe has been registering some weakness in economic data in recent months. But France is already so weak that further weakening would be devastating. Still, given France's size and importance, the heath of the euro area depends on France getting better. And France has few options left. It is obviously hoping that the new ECB lending program will help since France already has been given some leeway in getting its budget deficit back into shape. It is unlikely to get any more slack on that. Since the euro area controls the exchange rate and money supply mechanisms, government finance tinkering is all that France has left as a policy tool.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief