Global| Aug 27 2015

Global| Aug 27 2015French Business Climate Holds Recent Gains

Summary

The INSEE business climate indicator was at 103 in August, the same level as July and May, compared with June's lower reading of 100. Through March of this year, the index has been fluctuating in a range of 99 to 100. In May, the [...]

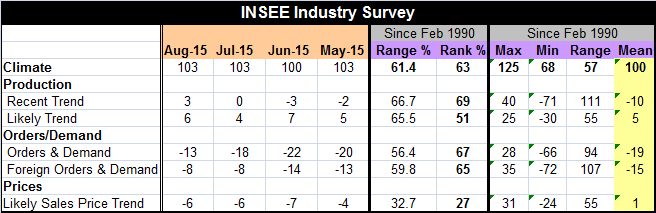

The INSEE business climate indicator was at 103 in August, the same level as July and May, compared with June's lower reading of 100. Through March of this year, the index has been fluctuating in a range of 99 to 100. In May, the index jumped and now - for two months running- it is holding that higher level. The 103 level on the climate index represents a 63 percentile standing in the index's historic queue of data. While this is a very moderate percentile standing, it is higher than the percentile standing of the manufacturing PMI offered by Markit. On this survey, French industry looks to be making moderate gains instead of showing ongoing contraction as with the Markit survey.

The INSEE business climate indicator was at 103 in August, the same level as July and May, compared with June's lower reading of 100. Through March of this year, the index has been fluctuating in a range of 99 to 100. In May, the index jumped and now - for two months running- it is holding that higher level. The 103 level on the climate index represents a 63 percentile standing in the index's historic queue of data. While this is a very moderate percentile standing, it is higher than the percentile standing of the manufacturing PMI offered by Markit. On this survey, French industry looks to be making moderate gains instead of showing ongoing contraction as with the Markit survey.

The recent trend for production stands at 3 in August, up from zero in July. That reading, while not strong, is nonetheless the highest since July 2011. The metric has a 69 percentile standing in its historic queue, a value that starts to look a bit more like normalcy. However, the likely trend for IP, which also has risen month-to-month to a value of 6 from 4, has a weaker standing.

The likely IP trend has a 51st percentile standing which is just above its midpoint reading. The problem here is that the likely trend is weaker than the recent trend on a percentile standing basis. Of course, the raw score is higher for the likely trend, but the raw diffusion scores are better understood as part of each category's time series that by trying to compared raw score for different measures in the same period. What the percentiles tell us is that the likely trend is weaker relative to its normal standing than is the recent trend and that is not encouraging.

The overall reading for orders and foreign orders are showing outright negative readings, but negative readings that are rising compared to their values in recent months. Indeed, the percentile standings of these negative values are quite moderate in the 67th percentile for demand overall and in the 65th percentile for foreign demand. These are much stronger percentile values than one would expect to see on such negative readings. But that just tells you something of France's history. While the outright negative value is off-putting, the queue percentile standing tells us that these are relatively moderate values for the French industrial sector by historic comparison. The mean for overall orders is -19 and the mean value for foreign orders is -15. Relative to those values both gauges are better than average which is what the percentile standing also tells us.

However, prices remain weak. There is a slight improvement in the price metric for the likely sales price trends in July and August relative to June but both are stronger than in May. Price expectations are lower only about 27% of the time. Their historic mean is 1.

Summing up

What we see in this French survey is some sense of improvement in the sector. The recent trend value is very encouraging. But the likely trend does not help us to feel that will continue. Orders and foreign demand are outright weak but better than they have been and much better than their respective historic norms.

France, of course, is competing in this same difficult global economy. The euro exchange rate has steadied in the recent month but has held to a historically weak level. Still, global growth is so weak and France has not been able to take great advantage of this pick up in its competitiveness outside the euro area.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief