Global| Dec 19 2008

Global| Dec 19 2008French Business Climate Goes South for the Winter

Summary

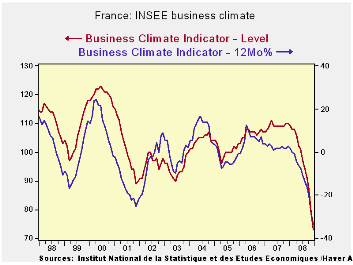

Business climate fell to 73 from 79 to a low since January of 1990 and tied for a life of series low last reached in June 1993 in this 35 year series. The recent trend and likely trend responses are also at their lowest since 2000. [...]

Business climate fell to 73 from 79 to a low since January of

1990 and tied for a life of series low last reached in June 1993 in

this 35 year series. The recent trend and likely trend responses are

also at their lowest since 2000. Order and foreign orders are now at

their lowest since 2000 but they are very weak, in the bottom 5% to 7%

of their respective ranges.

With this survey in hand INSEE now looks for France to suffer

a deeper recession than previously thought. Exports are diving and

plummeting sales now restrain and depress the manufacturing sector. The

euro zone's second-biggest economy would probably contract by 0.8

percent quarter-on-quarter in the final three months of 2008 after

growing just 0.1 percent between July and September, INSEE said in a

quarterly report. In Q1 2009 INSEE forecasts that the economy will

shrink by 0.4 percent and by 0.1 percent in the following quarter. In

its previous quarterly report, published in October, INSEE had

predicted a 0.1 percent decline in gross domestic product (GDP) in the

third and fourth quarters of 2008. Its view clearly has worsened.

Slowing global demand will continue to harm French exports, limiting

any advantage gained from recent softening in the euro, the statistics

office said (of course since this time the euro has strengthened

significantly making this point all the more forceful). INSEE said that

companies' efforts to run down surplus stocks are a further restraining

factor on manufacturing output, especially in the fourth quarter.

| INSEE Industry Survey | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Since Jan 1990 | Since Jan 1990 | |||||||||

| Dec 08 |

Nov 08 |

Oct 08 |

Sep 08 |

%tile | Rank | Max | Min | Range | Mean | |

| Climate | 73 | 79 | 87 | 91 | 0.0 | 221 | 123 | 73 | 50 | 101 |

| Production | - | - | - | - | - | - | - | - | - | - |

| Recent Trend | -72 | -68 | -65 | -41 | 0.0 | 222 | 44 | -72 | 116 | -6 |

| Likely trend | -35 | -26 | -19 | -9 | 0.0 | 222 | 30 | -35 | 65 | 6 |

| Orders/Demand | ||||||||||

| Orders & Demand | -56 | -43 | -31 | -26 | 6.9 | 216 | 25 | -62 | 87 | -15 |

| Fgn Orders & Demand | -53 | -47 | -26 | -27 | 5.6 | 214 | 31 | -58 | 89 | -11 |

| Prices | ||||||||||

| Likely Sales Price Trend | -8 | -1 | 9 | 14 | 31.9 | 176 | 24 | -23 | 47 | 1 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief