Global| Mar 25 2015

Global| Mar 25 2015French Business Climate Erodes and Momentum Flattens Out

Summary

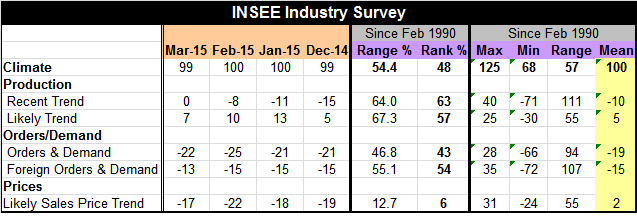

The INSEE survey of French business climate slipped to 99 in March from 100 (in January and February), dipping below its historic mean (100). The reading is now slightly subnormal and below its median (rank % = 50 is its median) and [...]

The INSEE survey of French business climate slipped to 99 in March from 100 (in January and February), dipping below its historic mean (100). The reading is now slightly subnormal and below its median (rank % = 50 is its median) and slightly above its range midpoint (Range % is above 50, which is the range mid-point).

The INSEE survey of French business climate slipped to 99 in March from 100 (in January and February), dipping below its historic mean (100). The reading is now slightly subnormal and below its median (rank % = 50 is its median) and slightly above its range midpoint (Range % is above 50, which is the range mid-point).

However, at this point in the business cycle, `normal' would be a reading that is a lot higher than just average. After a steep drop in 2008 and 2009, the INSEE indicator has risen. But it dipped again during 2012-2013 and its current recovery from that slippage is again in doubt as a too brief recovery in 2013 has given way to slippage and sideways movement in 2014 and early-2015 with momentum turning dead flat.

The good news is that while the climate reading may be dead flat the production trend reading is positive. Its historic average is at -10, making this month's reading of zero a relatively firm one and a clear improvement from -8 in February. The range and queue percentile standings confirm this with rankings in the low 60th percentile range. These are not strong readings, but they are firmer than most readings and could become the basis for improvement. For one thing, we continue to look for evidence that the weaker euro is having a positive impact on industry. The INSEE survey is from March and so its results could reflect a good deal of euro weakening.

The likely trend for production is also hopefully firm. At 7 in March, the reading is the lowest in the last two months, but it is above its historic mean and median with range and queue rankings of 67 and 57, respectively.

The forward-looking orders series is less optimistic. At -22, orders and demand are not much different than readings over the last four months and the March reading resides below its historic mean. It is below its median (queue ranking is below 50 at 43) and it has a 46 percentile range standing, below its historic range midpoint. However, looking at just the foreign sector, foreign orders and demand are better relative to their historic mean and with a queue rank of 54 are above their median with a range percentile standing of 55. These metrics look at demand outside France and the relatively better standing on this score (compared to overall orders/demand) may indicate that the weak euro is having some success in tapping French producers into external demand flows with improved competiveness. Nevertheless, the readings on foreign orders, while better than historic norms and better than for overall orders/demand, are still not very strong.

The ECB has been grappling with deflation fears. It has launched its QE program to try to stimulate growth. But in France expectations for prices are still poor. The -17 reading in March is only marginally stronger than the readings in recent months. The reading for March compares to a historic mean reading of 2. The historic rank for the March reading is in the bottom six percentile of its historic queue- a very weak expectation for prices, rarely lower. And the range assessment also finds the current reading in the lower 12% of its historic high-low range.

From this survey, we can ascertain France as having several types of problems. It has a real-sector problem with domestic demand being weak and weaker than foreign demand. Foreign demand for French products is improving but still very moderate. Despite that, there is some upswing in the recent production trend and even the likely trend is showing some improvement. Still, deflation is an issue. Price inflation is viewed as likely to remain very low. So far we can likely conclude that the lower euro may be helping France in stimulating external demand, but it is not yet a strong effect. The inflation expectation reading tells us that France has a lot at stake and is heavily invested in the success or failure of the ECB's QE effort.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief