Global| Apr 20 2009

Global| Apr 20 2009French and Italian Orders: Some Divergence Between These Siamese Twins

Summary

European orders are still on bad trends. But France is showing some life in February. As life signs go it’s still a weak vital sign despite its apparent vigor. Orders did jump by 5.2% in nominal terms in February, just one month after [...]

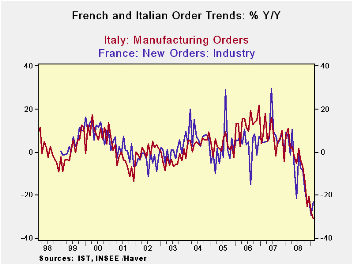

European orders are still on bad trends. But France is showing some life in February. As life signs go it’s still a weak vital sign despite its apparent vigor. Orders did jump by 5.2% in nominal terms in February, just one month after falling by 2.1%. But orders are still down by 23% over 12 months as the annual rate over three months has shot up to a positive 4.3%, a rare positive three-month reading in the e-zone. Still, the accompanying chart puts the French figures in context. The French Yr/Yr drop had been much worse than the similar decline in Italy since about may of 2008. With the large bump up in orders for France in February, France ’s Yr/Yr decline has braked and left Italy with the weaker trend, but this is nothing unprecedented.

For France the order revival is a domestic affair as foreign orders continued to fall by 0.6% in February, a drop but one with less vigor. Still the 5.2% rise in orders speaks of a sharp rebound domestically, possibly following the striking activity in France . So I’d be wary of reading much into it.

Compared to Italy , French foreign order growth has been much weaker over the last three months. Of course, one reason might be that Italy ’s ‘foreign’ orders have benefited from some uptick in domestic activity in France this month. By comparison, French exports have had no such favor in Italy , where the domestic economy is still struggling. Apart from that the two nations face a similar array of trading partners but with their own specific concentrations of trade, of course. Both countries show ongoing weakness in sales or in industrial output at home. As I said above, there is not much to sink your teeth into, if you are an optimist, despite the rise in French orders this month. Given the performance in the rest of Europe, especially Germany , and given the way the persisting French strikes have wracked the French economy, I’d be wary to read much into this rebound in French orders in February.

| Italy Orders | ||||||

|---|---|---|---|---|---|---|

| Saar except m/m | Feb-09 | Jan-09 | Dec-08 | 3-month | 6-month | 12-month |

| Total | -1.5% | -3.9% | -2.1% | -26.2% | -39.3% | -31.0% |

| Foreign | 3.5% | -3.0% | -2.1% | -7.2% | -37.6% | -30.2% |

| Domestic | -4.1% | -4.4% | -2.0% | -34.8% | -40.3% | -31.5% |

| Memo: | ||||||

| Sales | -3.1% | -4.0% | -3.3% | -34.6% | -33.1% | -23.0% |

| French Orders | ||||||

| Saar except m/m | Feb-09 | Jan-09 | Dec-08 | 3-month | 6-month | 12-month |

| Total | 5.2% | -2.1% | -1.9% | 4.3% | -30.8% | -23.3% |

| Foreign | -0.6% | -11.5% | 0.0% | -40.1% | -44.0% | -37.7% |

| IP ex Construction | -0.1% | -5.0% | -2.3% | -25.8% | -28.0% | -17.8% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief