Global| Aug 10 2017

Global| Aug 10 2017French and Italian IP Go Their Separate Ways in June But Stay on the Growth Path; European Growth Continues to [...]

Summary

Both French and Italian IP seem to be on growth paths in the wake of the release of their respective industrial production reports for June. In the case of France, there may be a bit more need to hold your nose when reading through [...]

Both French and Italian IP seem to be on growth paths in the wake of the release of their respective industrial production reports for June. In the case of France, there may be a bit more need to hold your nose when reading through the details. But all in all, French IP does not seem to be making a misstep just yet. For Europe as whole, the industrial sector is still in a solid growth gear.

Both French and Italian IP seem to be on growth paths in the wake of the release of their respective industrial production reports for June. In the case of France, there may be a bit more need to hold your nose when reading through the details. But all in all, French IP does not seem to be making a misstep just yet. For Europe as whole, the industrial sector is still in a solid growth gear.

French IP and trends

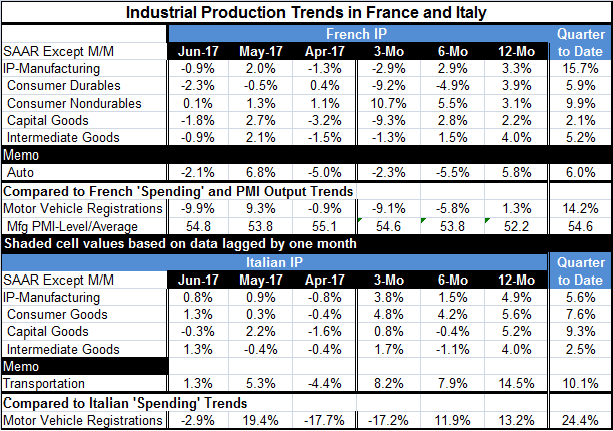

While French IP fell by 0.9% in June, it grew by 2% in May following a sizeable drop in April. The French three-month growth rate is at an annualized -2.9% compared to growth rates of 2.9% over six months and 3.3% over 12months. Three-month growth is being pushed into negative territory by consumer durable goods weakness, a drop in capital goods output and a drop in intermediate goods output. Over three months, only nondurables output is gaining, at a strong 10.7% pace. Despite this news, the French manufacturing PMI gauge rose to 54.8 in June from 53.3 in May mixing up the growth/no growth signals for June among indicators. In the quarter-to-date, however, IP itself is showing strong growth with the headline index up at a 5.6% pace in Q2 and all components showing increases in growth. The transportation sector shows a positive output growth rate on sequential horizons as well as a strong 10.1% growth rate in Q2. But vehicle registrations in France have hit a soft spot as they fell in June and are on balance lower in Q2.

Italian IP and trends

Italian IP grew by 0.8% in June, building on a 0.9% gain in May. April saw a striking 0.8% drop in Italian IP. All in all, Italian IP is growing and hitting the occasional pot-hole. Sequential growth rates show IP growth rates of 3.8% over three months, 1.5% over six months and 4.9% over 12 months. In June, the only sector with falling output is capital goods. Over three months IP gains are present in all major sectors. Consumer goods have consistently the strongest output gains. Italian transportation sector gains are positive and strong for all sequential growth rates. In the quarter-to-date, all sectors show solid to strong rates of growth. As we saw with France, there is some weakness creeping into motor vehicle registrations as they fell in June and are lower on balance over three months but did continue to grow strongly in Q2.

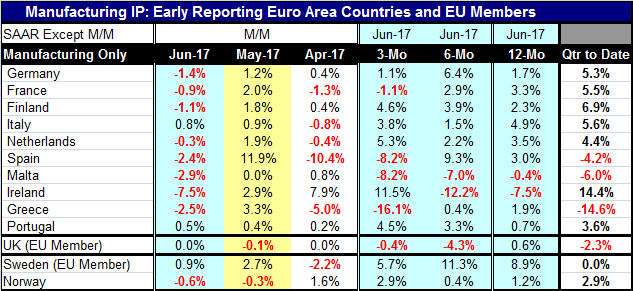

The full results for EMU IP are not yet available, but we do have manufacturing IP for many of the key European economies including most of the original EMU members. Among the group of 10 original EMU members in the table, eight show IP drops in June. We have already seen that June data have been 'unkind' to the German economy as exports and imports fell along with IP. Across the EMU, only Italy and Portugal saw IP gains in June. This result is less ominous when we also observe that IP fell in none of these reporting EMU nations in May although IP fell in five of 10 members in April.

More importantly, IP is falling over three months in only four countries: France, Spain, Malta and Greece. Spanish IP is notoriously volatile. Malta is a small country but experiencing more persist declines in output. Greece has been struggling with growth for some time and yet, despite its 16.1% annualized output drop over three months, it manages output increases over six months and over 12 months. Year-on-year only Malta and Ireland show IP declines; Ireland has been experiencing a good deal of volatility in its industrial sector.

In the quarter-to-date (i.e., the just completed Q2), IP is lower on balance in Spain, Malta and Greece. Apart from them, the weakest QTD growth rate is from Portugal at a 3.6% pace. This shows the Q2 trend to quite solid overall and broad-based.

Sweden, Norway and the U.K. also have IP gauges available. For these countries, the U.K. shows the most protracted weakness with negative growth rates over three months as well as over six months. Sweden's growth rates are solid except for one monthly decline in April that has undercut output trends in the quarter-to-date leaving them flat despite sizeable gains in May and June. Norway has output declining in each of the two most recent months, but its sequential growth rates still all positive and it logs a near 3% growth pace in the second quarter.

On balance, European trends appear solid with growth spread across the EMU area. This month France like Germany and a number of other EMU members hit an air-pocket and saw a downdraft in growth. But EMU countries generally are coming off a solid month's growth in May and sequential trends feature expansion and strength in Europe's most important economies as a rule. The only fly in the ointment is the U.K. where Brexit fears clearly have been getting in the way of growth.

European IP Growth

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief