Global| Feb 10 2021

Global| Feb 10 2021French and Italian IP Both Decline in December

Summary

Because of the way the calendar flows across the Covid-19 infection cycle, most EMU and most economies in the world show the same patterns for IP and for growth in general over 12 months, six months and three months. Italy and France [...]

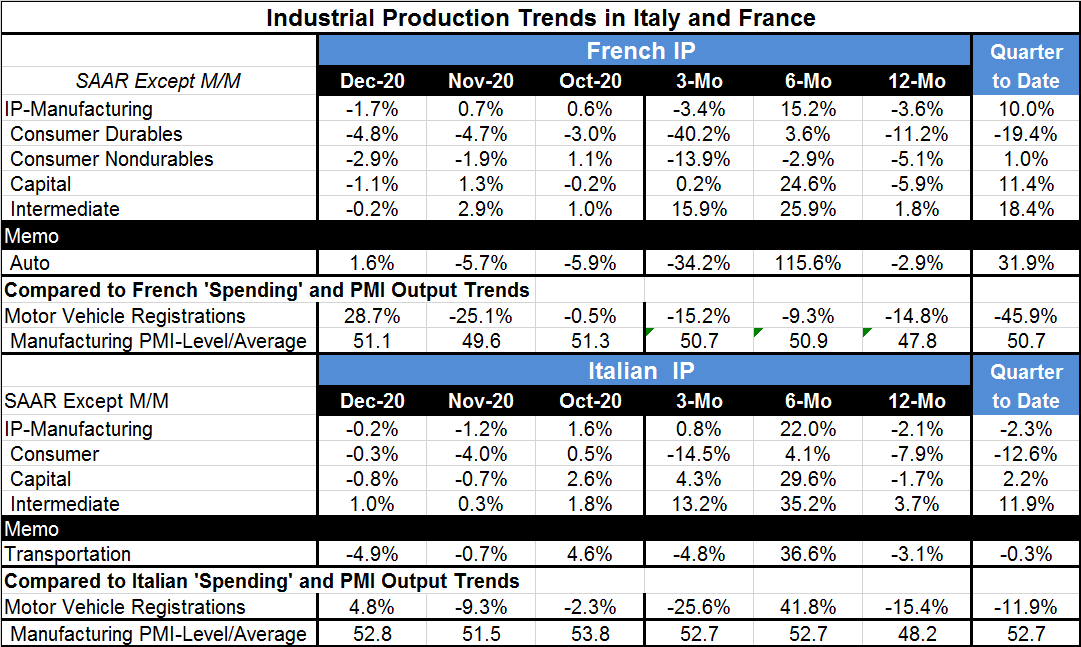

Because of the way the calendar flows across the Covid-19 infection cycle, most EMU and most economies in the world show the same patterns for IP and for growth in general over 12 months, six months and three months. Italy and France are not exceptions to this. Output is lower over 12 months, booms over six months and now is slowing or falling over three months. Growth is viral.

Because of the way the calendar flows across the Covid-19 infection cycle, most EMU and most economies in the world show the same patterns for IP and for growth in general over 12 months, six months and three months. Italy and France are not exceptions to this. Output is lower over 12 months, booms over six months and now is slowing or falling over three months. Growth is viral.

Growth rates ride the wild 'covid-19-curve'

The drop over 12 months reflects the fact that output is not yet back to its pre-covid-19 levels. The rise over six months is driven by the strong recovery after the Covid-19 meltdown. The weakness over three months is the result of a newer wave of infections that has slightly different timing across countries. As a result, in France three-month IP growth is falling at a 3.4% annual rate. In Italy output slows sharply from its six-month pace but is still eking out an annualized growth rate of 0.8%.

Growth and the virus timing

Both France and Italy show widespread declines in output across sectors in December and both show some mixed declines in November, with Italy suffering an overall decline in November IP while France notches an expansion. In December the virus was spreading in both Italy and France and both will be facing difficult times in January as the December spread worsened. In France the spread peaked in early-November and dissipated sharply into early-December when it started another gradual rebound. Death rates mirrored the infection cycle with a lag; deaths were muted relative to the size of the spread. In Italy the spread peaked more around mid-November and while it also dissipated rapidly the December levels of infection remained elevated and there was an uptick in infections in January. While the infection rate was much greater than earlier in the year, the death rates moved up to hit roughly the same peaks as earlier in the year and the elevated level of deaths lingered. So both Italy and France have ongoing virus issues, but they face slightly different timing, intensity and durations of the outbreak.

A unique signature

As the virus has spread globally, these sorts of comparison inevitably show that there are more country differences than there were in the first cycle when the virus hit most countries at about the same time. In this episode the timing, intensity and breadth of the virus can be quite variable. Of course, the U.K. even has a new strain of the virus that is spreading across Europe and has migrated to the U.S. as well. The virus does not stay cooped-up. Even with vaccines in distribution, risks seem to grow.

Different fourth quarters in Italy and France

In the now-finished fourth quarter (quarter-to-date column), France is showing a gain in IP for the quarter while Italy is logging a decline. France's IP gain is built on solid output gains in October and November offset party by a large drop in December. Italy's drop comes after a strong gain in October and as nearly as a strong fall in November followed by a small drop in December. These differences in quarterly growth evolution were also enhanced by the fact that French IP rose strongly in September boosting the level of IP relative to the Q3 average. Meanwhile, in Italy, September IP fell sharply putting the IP level in a hole relative to the Q3 average for the start of Q4. Even quarterly data have these sorts of idiosyncrasies that imbue quarterly comparisons with volatility.

Still lots of sector trends in common

But there still are similarities. Both Italy and France see the output of consumer goods is lower in Q4. Both log negative growth in double digits for consumer goods output. Both show a gain in capital goods output with Italy logging weak gain and France posting a large one. Both show double-digits gains in intermediate goods output.

Demand patterns for autos and vehicles

There are also several lines in the table dedicated to tracking demand on these timelines. Both Italy and France show double-digit declines in auto or motor vehicle registrations over three months; in France the weakness is slightly less and is less volatile. Auto production in France and motor vehicle production in Italy are both declining over three months. And while sequential growth patterns are quite different, both are down by about 3% over 12 montths.

Italian and French PMIs

Both French and Italian PMIs have been hovering around the '50' or breakeven mark in terms of their manufacturing PMIs values. The Italian manufacturing PMI has been consistently stronger in the quarter, but both PMIs show output is expanding in December at least in PMI terms despite the fact that actual output has declined.

Similarities, differences, risks

These comparisons show a lot of similarities in the Italian and French industrial sectors. While the virus sweeps across countries and regions with uneven results over time, we can see a lot of similarity in the impact on the French and Italian economies. Whether output was up or down in the quarter, both showed a good deal of output irregularity during the quarter. The year 2021 is off to a start with a good deal of virus dislocation. The UN is warning that there will be a pullback in global trade in Q1 because of the virus. The outlook is still positive because there is vaccine distribution, but there also are question marks because of the development and spread of new virus strains, some of which may be vaccine resistant – at least to the vaccines we currently have.

An outlook and a warning

Christine Lagarde, ECB President, is warning that Europe is going to need ongoing support from fiscal policy in 2021. There is a growing realization that even if the vaccines work against the virus as expected, economies are going to continue to be significantly impaired through at least mid-year and maybe longer depending on rollout issues and the emergence of rogue virus strains. The danger here is that economies start to look more normal, but they remain at risk. And even as the virus spread is slowed, until there is herd immunity people are likely to be wary of economic participation and that will hold back growth. The danger is that governments look at their bloated debt and deficits and decide to cut back support too soon. Growth forecasts already are looking pretty rosy for 2021. But the assumptions that forecasts are built on often do not come to fruition so the stimulus game is one played in real time as well as with an eye on the future and to future uncertainty. After all we do not know what we do not know and neither do we 'know' that which we forecast.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief