Global| Jul 16 2004

Global| Jul 16 2004Foreign Purchases of U.S. Securities Ease in May Amid Wide Volatility

Summary

The US Treasury today published its array of monthly data on foreign investors' purchases and sales of "long-term" US securities (having maturity greater than one year) for May. Known as the "TIC" data for Treasury International [...]

The US Treasury today published its array of monthly data on foreign investors' purchases and sales of "long-term" US securities (having maturity greater than one year) for May. Known as the "TIC" data for Treasury International Capital", this extensive collection of information on foreign participation in US capital markets is contained in Haver's USINT database in the section "US International Investment Tables", shown by security type and country. In May, net foreign purchases of securities traded in US markets totaled $56.4 billion, down from April's $76.1 billion.

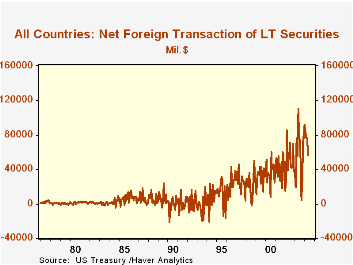

The first graph above shows a simple history of these net foreign purchases of securities in US markets. Besides the simple fact that these transactions have expanded dramatically since about 1985, the most recent periods have also shown significant volatility. Simple explanations are often offered for this activity: a large current account deficit that must be financed, fear of a weakening dollar, the impact of a rising dollar, and so on. Indeed, the current account relationship is significant: aggregated on a quarterly basis, the value of these transactions has had a 90% negative correlation with the current account balance over the past 20 years. But the wide swings in the capital flows, particularly over the past year-and-a-half, suggest that causes for foreign moves in and out of US markets must be much more complex.

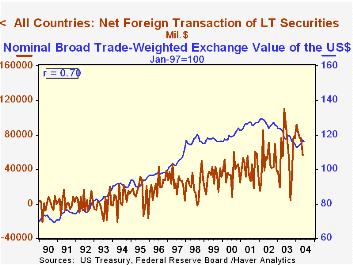

The second graph examines the interaction in these data with a broad gauge of the exchange rate. Using the Fed's "Broad" trade-weighted dollar index, we see an attractive-looking 70% correlation over the past 15 years. However, this correlation coefficient changes markedly over varying time periods. So while the fit may be pretty good over the years we illustrate, during the last 10 years, that drops to just 44%. An earlier 10-year period, 1986-1995, shows a mere 1%. Thus, it's hard for investors and traders to count on a particular securities market response to foreign exchange developments. And these relationships deteriorate further when individual countries are examined. The correlations between the yen and net capital flows of Japanese investors generally run in the mid-20% area.[Note that all our comments are based on examination of data properties revealed using Haver's DLXVG3 software alone. With the "correlation" tool turned on, scrolling across the graph using the arrow keys shows the evolution of the correlation ratio through time.]

| Net Foreign Purchases of Securities in US Markets (Billions US$) |

May 2004 | Apr 2004 |

Mar 2004 |

May 2003 |

Monthly Average

|---|---|---|---|---|

| 2003 | 2002 | 2001 |

| Total | 56.4 | 76.1 | 76.8 | 109.9 | 58.4 | 47.9 | 41.8 | |

|---|---|---|---|---|---|---|---|---|

| Treasuries | 21.9 | 35.3 | 61.5 | 41.1 | 22.7 | 10.0 | 1.5 | |

| Federal Agencies (mostly "GSEs") | 20.7 | 31.0 | 3.9 | 31.9 | 13.6 | 16.3 | 13.7 | |

| US Corporate Bonds | 19.9 | 16.8 | 30.4 | 27.4 | 22.7 | 15.2 | 18.5 | |

| US Corporate Stocks | -7.6 | -1.8 | -13.4 | 6.6 | 3.1 | 4.2 | 9.7 | |

| Foreign Bonds | 7.4 | 6.1 | -1.7 | 13.5 | 2.2 | 2.4 | 2.5 | |

| Foreign Stocks | -5.8 | -11.3 | -4.0 | -10.9 | -6.0 | -0.1 | -4.2 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief