Global| Nov 27 2018

Global| Nov 27 2018For the U.K.: A Brexit Christmas

Summary

With the U.K.'s Brexit process in its final deal-or-no-deal stages, the Confederation of British Industry survey turned up some retail optimism. However, despite the bump up in the surveyed components in November, the levels of the [...]

U.K. Retailing Shows Resilience But in the End Not Enough

With the U.K.'s Brexit process in its final deal-or-no-deal stages, the Confederation of British Industry survey turned up some retail optimism. However, despite the bump up in the surveyed components in November, the levels of the readings are still not very inspiring as retailers head into the all-important Christmas selling season. It's sort of like Department Store Santa but without enough stuffing in his belly and a really bad fake beard. No one really is fooled one bit by the costume, but we all go along with the gag.

With the U.K.'s Brexit process in its final deal-or-no-deal stages, the Confederation of British Industry survey turned up some retail optimism. However, despite the bump up in the surveyed components in November, the levels of the readings are still not very inspiring as retailers head into the all-important Christmas selling season. It's sort of like Department Store Santa but without enough stuffing in his belly and a really bad fake beard. No one really is fooled one bit by the costume, but we all go along with the gag.

In the distributive sales survey in November, sales compared to a year ago jumped to a 19 reading from 5 in October. Orders evaluated relative to the time of year also surged to a 15 reading from -10, breaking a four month string of declines. However, sales for this time of year were still assessed with a net negative of -10; nonetheless, that's an improvement from the October reading of -22. The stock-to-sales ratio moved higher, with a 22 net reading in November, up from 9 in October.

Wholesaling also made improvements from one month ago as its November metrics exceeded their October counterparts in all survey categories except for the stock-to-sales ratio.

Expectations in retailing show improvement in most areas. The exception is for orders for this time of year as the reading falls to 15 for December from 23 in November. Still, the last two months both are positive readings and represent a turnaround from a three-month string of negative assessments. Expectations in wholesaling show improvements in all categories for December compared to November.

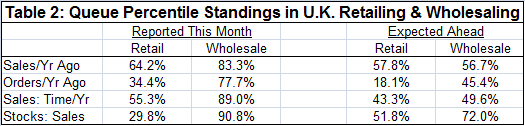

These comparisons show that there has been an improvement in the month-to-month assessment of retailers with data ordered up in several ways to account for 'seasonality.' We can also assess the absolute response levels instead of just asking if they improved or deteriorated month-to-month. Table 1 presents assessments for that purpose in the far right hand column as rank queue percentile standings. These metrics rank the most recent month's observation against its own historic time series of responses placing this month's observation in a queue designating its relative position as a percentile standing in that queue. A 100% standing is at the head of the line (the strongest reading) while a 0% standing is at the end of the line (the weakest reading). For this assessment, each series' median occurs at its 50th percentile. Data are ranked on observations back to 1995. For convenience in comparison, I have transcribed this data into the table below (Table 2).

In Table 2, several facts jump out immediately. One is that wholesaling this month has the strongest readings of any of the four columns of assessments and consistently so. The next is that retailing has weaker expectations for December sales (on either sales measure) than the reality it is reporting in November. Of course, wholesaling has weaker results for December expectations than for November reality. Also note that despite November differences for retailing and wholesaling for both of them, sales metrics expectations in December are very similar in both retailing and wholesaling.

Having made those points and even in the presence of such strong wholesaling results in November, this report grades out poorly. Orders have a below median position for retailing in November and that weakness even worsens in its December expectation. Expected wholesale orders even fall below their median with a 45.4 percentile standing for December. Sales for this time of year are barely above their median in retailing in November (55.3%) then slip below their median to a 43.3 percentile standing along with wholesaling for December where expectations at 49.6% fall just shy of its own median as well. The next metric that we care about is sales compared to a year ago. For retailing in November that reading is at its 64.2 percentile, a modestly firm reading, that slips to its 57.8 percentile in December expectations alongside a similar 56.7 percentile reading for wholesaling expectations in December. Both retailers and wholesalers are expecting stock-to-sales ratios to be relatively elevated, which could become a problem.

On the whole, the high November standings for wholesaling give the overall report a feeling of lift. But when we look more closely at retailing and at the sales and orders categories we care about the most, we find some of the weakest results and with weakness creeping into the wholesale sector on its December expectations as well. Aggregating all of the readings, wholesaling averages a rank of 85.2% in November, but that drops to a 55.9% for all expectations in December. The average standing in retailing for the three sales and orders categories in November is 51.3% and that falls to 39.7% for retail expectations in December; for wholesaling the same combination falls to a 50.6 percentile standing. Compare that to wholesale's 83.3 percentile standing for all sales and orders in November.

The problem with this report is the peaking of activity in wholesaling in November and the fall off of metrics in their December expectations as well as the overall low percentile standings with the exception of wholesaling in November.

While the headline changes in the CBI offer some hope, the level that these indicators have actually attained and what they aspire to in December are still markers well short of what we would need to call them solid. So in the end, I guess the U.K. will have itself a very Brexit Christmas.

And so what exactly is a Brexit Christmas? According to the National Institute of Economic and Social Research it amounts to the celebration of this:

"If the government's proposed Brexit deal is implemented, then GDP in the longer term will be around 4 percent lower than it would have been had the UK stayed in the EU" (Source here).

The leavers won their Brexit vote. The U.K. voted for a return of the control of its borders and it has paid a steep price for it. What NIESR does not assess is the impact or value of any new trade deals that the U.K. might strike. But it will need to do a lot just to get back lost potential growth let along to make claims that it is better off with the EU-tether to Europe cut.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief