Global| May 22 2014

Global| May 22 2014Flash PMIs Show EMU Progress and a Lagging France

Summary

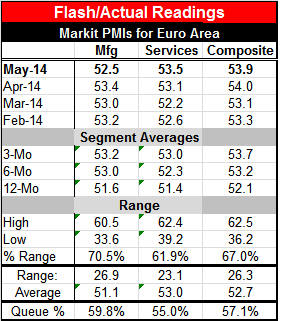

The flash PMI for the euro area ticked down to 53.9 in May from 54.0 in April. The services reading rose to 53.5 from 53.1 while the manufacturing reading slipped to 52.5 from 53.4. From mid-2011, the May composite reading is the [...]

The flash PMI for the euro area ticked down to 53.9 in May from 54.0 in April. The services reading rose to 53.5 from 53.1 while the manufacturing reading slipped to 52.5 from 53.4. From mid-2011, the May composite reading is the second-highest over that period.

The flash PMI for the euro area ticked down to 53.9 in May from 54.0 in April. The services reading rose to 53.5 from 53.1 while the manufacturing reading slipped to 52.5 from 53.4. From mid-2011, the May composite reading is the second-highest over that period.

The data in the first table combine actual with flash observations. We use actual data for all months except the current month where we only have the flash available. For this purpose, we treat the flash as an estimate of the actual number in the current month, rather than as a separate time series. We position trends in these series back to 1998.

Despite the fact that the services reading was relatively stronger this month when we position the services and manufacturing indices in their historic ranges, manufacturing is stronger. Its current flash reading stands in the 70th range percentile while the services reading sits back at 61st percentile. The range reading establishes the current observation between the highest and lowest observations historically, expressing that standing as a percentile.

On balance, however, the EMU readings are all above 50, indicating progress in the monthly slippage in manufacturing is minor. This table deals in only flash data which extend back only to 2006. Some of the percentile data will be different than in the table above it which has a longer time horizon and uses actual data for its historic calculations back to 1998 instead of past flash data. One of the main differences is that over the longer time horizon the EMU manufacturing sector queue standing is still higher in May 2014 whereas on the shorter comparison (since 2006) the relative standing of the services sector is superior.

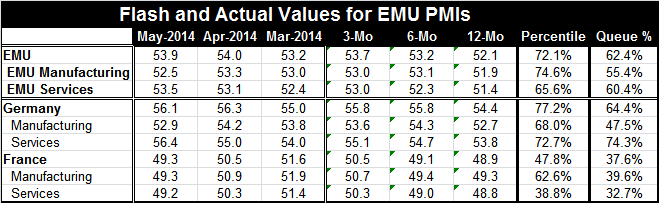

We also get percentile standings for Germany and France. The standings for France are quite disappointing. The French total PMI is down to 49.3 in May from 50.5 in April and 51.6 in March. That's a steady erosion. The averages over three months, six months, and 12 months for France show barely any elevation at all; the improvement over three months compared to six months depends heavily on the relatively firm reading in March 2014, which has eroded over the past two months. French manufacturing has slipped in each of the last two months. Although its sequential averages show a slight firming, once again, the firming trend owes itself to a strong reading in March that has since evaporated. The services reading shows contraction in May as well, slipping from April which had also slipped from its March level. Its three-month, six-month, and twelve-month sequential averages show only a slight firming. The strength over three months owes substantially to the firm reading in March which once again has since dissipated. The readings for France are quite disappointing. Note that the queue percentile standings of its PMI metrics are all in the 30th percentile of its queue, implying that these readings are weaker only 30% to 40% of the time. At this stage of a `recovery' these are abysmal metrics.

Germany also shows slight slippage in its total PMI which fell to 56.1 in May from 56.3 in April. The April reading advanced from March's 55.0. Germany's sequential averages show firming over six months compared to 12 months followed by steadiness as the three-month average stands at 55.8, the same as its six-month average. Its May value is above that, indicating that there is still momentum moving forward for Germany. Germany's manufacturing index has generally performed about the same way as its overall index except with less recent momentum. Its May figure fell back from April, while April showed a slight rise compared to March. Manufacturing shows a strengthening in the six-month average compared to the 12-month average, with some slippage over three months with the May reading below the three-month average indicating that for manufacturing momentum has been short-circuited at least for now. The German services sector is strengthening. It simply plows ahead. Its 56.4 reading in May exceeds its April value; its April value exceeds its March value. Its sequential averages move higher from 12 months to six months to three months. In addition, the May reading resides being above its three-month average, indicating the presence of ongoing and still-building momentum in services.

Here it is important to take note of the queue percentile standings. In raw terms, the German manufacturing sector is only slightly weaker than its services sector (52.9 vs. 56.4). But in terms of queue standings, manufacturing has been left in the dust by services. Germany is a capital goods/manufacturing-led economy. Its manufacturing sector is always strong. For manufacturing, a reading of 52.9 is poor; it shows only a small margin above neutrality (50). The current German manufacturing value stands below the median of its historic readings, in only the 47th percentile of its historic queue. But services are not usually so strong in Germany. That sector's 56.4 reading stands in the 74th percentile (of its own historic queue), representing more relative strength than manufacturing (more strength relative to its own past history compared to manufacturing). In this comparison, we can see and appreciate the relatively better performance of the German services sector and its obvious contribution to the EMU-wide metrics which look so solid this month.

The strength in German services could be a good sign for the European Monetary Union since services are typically a domestic economy phenomenon; manufacturing strength can come from exports and build off of foreign demand. Not so for services. As the services sector strengthens and employs more people, domestic demand in Germany should improve; new service sector workers will become consumers who should use their income increase to add to the demand for German imports, thereby helping to stimulate the rest of the EMU. This is more or less the way the German economy typically operates, being led in the early stages by its capital goods sector and export-led growth with domestic demand filling in behind. Germany, which has been the strong economy in the EMU, may find itself in a position to help to boost the rest of the union higher by adding domestic demand strength to its economy's portfolio.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief