Global| Mar 31 2009

Global| Mar 31 2009Flash Dance - Inflation Waltzes to New Lows as Risk Soars to Dizzying Heights

Summary

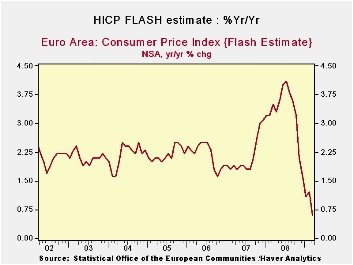

Fat Chance… The EMU FLASH HICP is at an all time low skinny 0.6% gain Yr/Yr. If it were human we’d say it is anorexic. Italy also got on the board with a weak HICP, posting the lowest reading since ‘Ed Sullivan’ and ‘Leave it to [...]

Fat Chance…

Fat Chance…

The EMU FLASH HICP is at an all time low skinny 0.6% gain

Yr/Yr. If it were human we’d say it is anorexic. Italy also got on the

board with a weak HICP, posting the lowest reading since ‘Ed Sullivan’

and ‘Leave it to Beaver’ were first run shows. (roughly 1968).

Gooey Good News

Despite al this gooey good news the pace of inflation’s drop

actually is slowing, not speeding up. The Yr/Yr at 0.6% is higher than

the six month pace of -1.4% but then over three-months the pace

flattens at 0%. Core inflation is still stepping down. But we know what

is going on and what is driving these trends. Headline inflation is

driven by food and energy and in this cycle energy has taken the wheel,

not some deity. Spot oil prices had collapsed but the have climbed back

to the vicinity of $50.bbl. It is hard to tell where oil goes short

term, but prices are the up from their lowest, meaning headline

inflation will perform that same magic trick.

Peak oil not an issue now…

In broader terms inflation is clearly under control. When the

world economy grows again there will once again be all those questions

about peak oil or not. China is a new factor underpinning demand. But

we can put those questions off for a while.

Reality bites and the OECD worries

For now, and for some time to come, inflation seems to be

under control. The big news on our plate is the G-20 meeting and how

policy will respond to the current diverse challenges. The OECD

introduced a series of forecasts ahead of this meeting that have gotten

even glummer. The OECD is urging more stimulus as a result. All this is

going to put more pressure on the ECB to move rates lower, especially

with Euro-stimulus policy in the shape it’s in. The summit seems to be

a done deal as euro-stubbornness has won out. In addition French

intransigence is trying to make headway as France has threatened to

boycott if the regulation proposals are not enacted. Summit policy is

always pre-determined but it isn’t always this clear.

Policy options are alive…but not well…not even good

All in all it is not really surprising with such economic

weakness to find inflation is under control. That development puts more

leeway in the hands of policymakers. But what happens when they refuse

to take up the opportunity? Europe admits its 200bln euro plan will not

have much impact until 2010. That was Junker’s contribution to the

discussion today as the OECD ramped up the bad news. The US seems to be

living in a different world where action is required while Europe sits

back to watch. Some of this is that Europe already has a better social

safety net than the US. But that is ‘cushion’ and what the world needs

now is ‘stimulus,’ sweet stimulus. But it’s not happening in London.

London 2009 will make the same mistake as London 1977. It will reject a

chance for more stimulus and stretch out the pain. If London 1977 is a

learning experience, it launched Bonn 1978 and the result was that too

much stimulus was enacted too late. I hope that is not our true path.

On the other hand part of me says, ‘Fat chance’.

| Trends in EMU HICP: Flash Index | |||||||

|---|---|---|---|---|---|---|---|

| % mo/mo | % SAAR | ||||||

| Mar-09 | Feb-09 | Jan-09 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| EMU-13 | -0.1% | 0.3% | -0.2% | 0.0% | -1.4% | 0.6% | 3.6% |

| Core | #N/A | 0.2% | -0.2% | 0.6% | 1.1% | 1.7% | 2.4% |

| Goods | #N/A | 0.3% | -1.2% | -6.3% | -3.2% | 0.3% | 3.8% |

| Services | #N/A | 0.5% | -0.4% | 3.9% | 0.6% | 2.4% | 2.5% |

| HICP | |||||||

| Germany | -0.2% | 0.3% | 0.0% | 0.4% | -1.3% | 0.4% | 3.3% |

| France | #N/A | 0.3% | -0.1% | -0.3% | -1.0% | 1.0% | 3.2% |

| Italy | 0.0% | 0.4% | -0.6% | -0.7% | -0.9% | 1.0% | 3.5% |

| Spain | #N/A | 0.2% | -0.4% | -2.4% | -2.7% | 0.7% | 4.4% |

| Core excl Food Energy & Alcohol | |||||||

| Germany | #N/A | 0.4% | -0.1% | 1.5% | 0.8% | 1.2% | 2.2% |

| Italy | #N/A | 0.5% | -0.6% | 0.4% | 1.1% | 2.2% | 2.4% |

| Spain | #N/A | -0.2% | -0.2% | -1.3% | -0.1% | 1.6% | 3.3% |

| Blue shaded area data trail by one month | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief