Global| Sep 28 2020

Global| Sep 28 2020Finland's Sector Confidence Indicators Waffle

Summary

Finland's EK sector survey shows a great deal of lingering weakness in Finland despite some clear signs of revival in progress. The diffusion data by sector rank retailing as the strongest with a September value of 7 followed by [...]

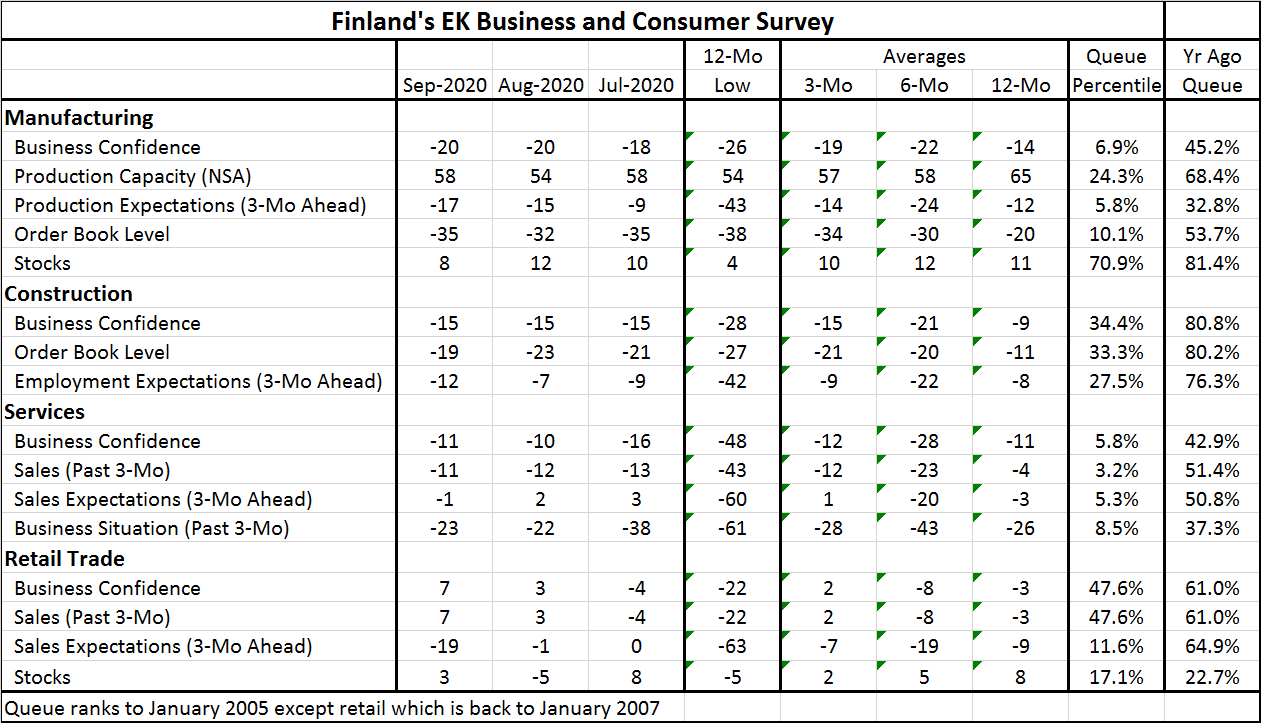

Finland's EK sector survey shows a great deal of lingering weakness in Finland despite some clear signs of revival in progress. The diffusion data by sector rank retailing as the strongest with a September value of 7 followed by services (-11), construction (-15) and manufacturing (-20). The ranking by the queue standing of the diffusion indexes show retailing (47.6%), construction (34.4%), manufacturing (6.9%), and services (5.8%). The queue standing put the current diffusion readings in a ranked queue of observations based on data back to 2005 or 2007.

There is not a great deal of difference in these rankings and those sectors that switch ranks generally are otherwise close in values with only construction and services having a huge difference between their diffusion value comparisons and their queue rank comparisons.

The chart shows the sharpest rebound is from services, but then services had the sharpest fall and tends to have the highest diffusion values.

The chart shows the sharpest rebound is from services, but then services had the sharpest fall and tends to have the highest diffusion values.

The comparisons of current diffusion values to their 12-month lows clearly flags the services sector as the most recovered from the Covid-19 impacted lows. Business confidence in services is up by 37 diffusion points from its 12-month low reading, compared to 29-point rise in retailing, a 13-point rise in construction and a 6-point rise in manufacturing.

For manufacturing the rebound from the 12-month low is weak, but the change in production expectations for three-months ahead is a very much stronger at 26 diffusion points. Still, production expectations even with that 'pop' have a very low 5.8% standing in their historic queue of values. Manufacturing order books are off their 12-month lows, but not by much and carry a 10.1% historic queue ranking. I don't know where 'production expectations' come from, but they clearly are not now linked to order book levels. Historically these two series have a correlation of 0.76, but that is not the case at the moment as the 12-month correlation has dropped to less than 0.5.

Services are up very strongly from their 12-month lows but like manufacturing continue to post weak queue standings – in the bottom ten percentile for all categories. And despite this strong rebound, the momentum change indicated over the last several months has run out of gas; sales expectations have even weakened since July. Other services metrics are making ongoing but weak improvements.

Retail trade shows strong gains from their 12-month lows led by expectations for sales three months ahead. Business confidence in retailing has a solid 29 diffusion point rise from its 12-month low. But even with these changes afoot, business confidence in retailing has only a 47.6 (below median) percentile standing. Despite their 12-month gains, sales expectations have only an 11.6 percentile standing and have just eroded sharply in September. While retailing has some of the strongest values, its expectations module is weak.

Construction was a high-flying sector; one-year ago it had an 80th percentile standing for business confidence. Today that is chopped back to a 34.3 percentile standing. Business confidence in construction is up from its lows but not strongly and the largest gain in diffusion points is for 3-month ahead employment expectations that are up by 30 points but strangely are leading – and leading by a lot - the 8-point rise in order books. That is odd. Jobs do not lead; they follow.

On balance, Finland still shows substantial lingering effects from the ongoing coronavirus setback. There is some recovery afoot, but the signs of recovery are not supported by some of the core readings we would like to see like order books rising and leading the parade. When employment expectations lead or production expectations lead even as order books dally, it is hard to have confidence in that optimism.

Of course, Finland is also well plugged into Europe as an EMU member and it may be that revival in the rest of Europe is a stronger positive than its own domestic metrics at the moment. But the virus is emerging again in Europe. In Finland, the sweep of the infection curve has been turning up again although it recently made a relatively sharp move lower on September 24. As always, any confidence about growth has to be filtered through the prospects for the virus. While Finland does have clear lift off from its virus-worst levels, manufacturing and construction show little change in the readings of last three months as services make progress and retailing seems to be caught in the cross currents of change and ongoing infection.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief