Global| Aug 24 2015

Global| Aug 24 2015Finland's PPI Continues to Show Declines; Will World Events Accelerate It?

Summary

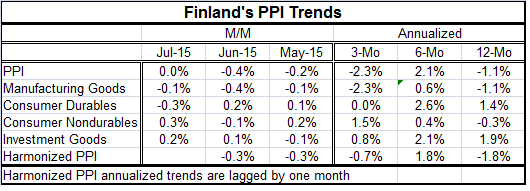

Finland's PPI was flat in July, but it is still falling at a 2.3% annual rate over three months. The index was up at a 2.1% pace over six months but lower by 1.1% over 12 months. Finland continues to experience downward prices [...]

Finland's PPI was flat in July, but it is still falling at a 2.3% annual rate over three months. The index was up at a 2.1% pace over six months but lower by 1.1% over 12 months.

Finland's PPI was flat in July, but it is still falling at a 2.3% annual rate over three months. The index was up at a 2.1% pace over six months but lower by 1.1% over 12 months.

Finland continues to experience downward prices pressures. The trends for manufactured goods mirror those for the headline but with less price pressure over six months.

Consumer nondurable prices are showing some increasing pressure. But that trend is not shared by durable goods. Investment goods show steady inflation trends around 2% until the last three months when its increases gave way to a drop at under a 1% pace.

Finland shows the dilemma of Europe. Inflation is no longer showing persistent deceleration. But prices are weak and in the case of the headline, falling at a modest pace year-over-year. It's a victory of sorts to stop the trend toward deflation. But over the last year or so inflation still tends to be negative and now with global chaos oil prices are collapsing and the risk to growth are on the rise. The decline in commodity prices will crimp growth in the developing world.

China is, of course, at the epicenter of this collapse; it is sending its shock waves worldwide but the impact is concentrated in Asia. Global stock markets are the clearest place for find impact as expectations about future growth play out in stock indices. And today stock markets are down sharply. Asian markets are off by 4.5% to 85% on the day. In European trading the French market is off by 7%, Germany by less than 6%. In early trading in the U.S., markets were off by 4.6% to 7.8%.

In these circumstances, the prospect for inflation to take hold in Finland -or elsewhere- looks remote. Declines in the stock market destroy wealth and that have an adverse impact on consumption and will obviously also cause investment plans to be trimmed. U.S. auto firms operating in China already have cut back their operating rates and are below capacity for the first time since producing there. There will be knock on effects from the global stock market declines and there will be real sector weakness as well. All previous forecasts are off. The Kansas City Fed is having its annual conference in Jackson Hole Wyoming. We will expect to hear something from the Fed about the impact of this crisis on its policies even though Janet Yellen is not attending the conference.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief