Global| Nov 01 2016

Global| Nov 01 2016Finalized Manufacturing PMIs Largely Improve in Asia and Elsewhere

Summary

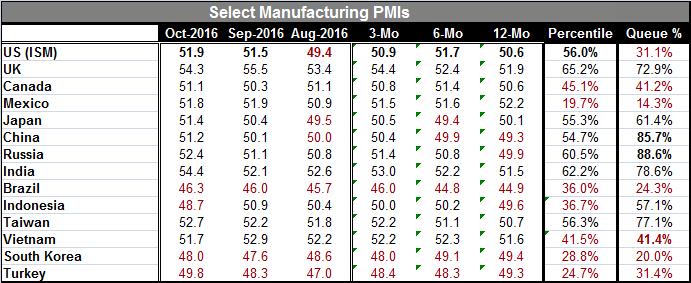

Asia area PMIs mostly improved in October as Indonesia and Vietnam were exceptions. The U.K., a Western nation with a finalized PMI, showed a drop off in October. The US (ISM) manufacturing PMI also was announced for October and it [...]

Asia area PMIs mostly improved in October as Indonesia and Vietnam were exceptions. The U.K., a Western nation with a finalized PMI, showed a drop off in October. The US (ISM) manufacturing PMI also was announced for October and it showed a slight upward tilt although it retained a low standing in its queue of data over the past six years (bottom 31%). Canada improved as well. In Latin America, Mexican conditions eased while Brazil improved but continued to contract. Turkey also improved but contracted.

Asia area PMIs mostly improved in October as Indonesia and Vietnam were exceptions. The U.K., a Western nation with a finalized PMI, showed a drop off in October. The US (ISM) manufacturing PMI also was announced for October and it showed a slight upward tilt although it retained a low standing in its queue of data over the past six years (bottom 31%). Canada improved as well. In Latin America, Mexican conditions eased while Brazil improved but continued to contract. Turkey also improved but contracted.

Despite being good signals, they are weak signals

Despite the widespread month-to-month improvement in manufacturing sector PMIs, the indices by and large are still low-valued and with a few exceptions are still quite weak or moderate even by the standards of the past six years or so when conditions have been unexceptional and for the most part trying. China and Russia both posted readings in the top 20% of this recent range. But China's PMI reading is only 51.2, a very low reading to have a top 15% standing as it does. Russia's index jumped this month. With the oil market in turmoil and Russia trying to wrestle some sort of deal with OPEC, I am frankly concerned about the veracity of the Russian numbers.

Manufacturing mostly shows growth and improved growth

Among the 14 countries in the table, only four have manufacturing indices below 50 indicating a contraction in the sector. Those countries are Indonesia, South Korea, Brazil, and Turkey. Markets today reacted well to the release of the Chinese manufacturing PMI showing a stronger move into areas that indicates expanding output.

BOJ take path of least resistance

The big economic news today was that Japan's central bank did not make any of the major alterations to policy that some had talked about. Japan played it 'safe' instead, keeping its bond purchase target in place, keeping its inflation target and keeping its policy rate but only pushing out the date by which it expects to meet its inflation objective. Of course, this is in some sense the same as cutting its inflation target near term. It is an admission that the BOJ will not hit its target on the timeline that previously was in place. But as policy changes go, it is the least obtrusive thing it could have done. Changing a schedule is different from a change in the objective of policy. Japan can argue that it has kept its objective but was forced to bend to the realities of near-term inflation resistance.

Aussies marking time

In Australia, after several rate cuts in May and in August, the Reserve Bank of Australia has gone on hold.

Fed on hold for now

Meanwhile, markets in the U.S. are focused on the two-day Fed meeting that will conclude with a policy statement on Wednesday. Because of the proximity to the U.S. general elections (presidential election cycle), the Fed is expected to stay on hold in November. But market watchers are still on alert for any signal that the Fed might give that might seem to commit it to action in December.

But Fed gets ready to fire up its Fleetwood Mac strategy and 'Go its own way'

While other central banks are still being watched for signs of providing further stimulus, the Fed is expected to make another move to withdraw some degree of stimulus. The Fed began with a withdrawal using a single 25bp rate hike in December 2015 then its vice chairman spoke of the possibility of as many as four more hikes in 2016. Instead, that talk unnerved and unhinged markets and here we are late in the year and the Fed has not followed up its December hike with a single move. The lack of follow-up move in Fed policy speaks volumes of how premature the Fed's foray was into rate hiking in December 2015. And now, even without the proper justification, the Fed is on the verge of hiking rates again and largely for the same reason it hiked rates in 2015: because so many members have said they would even though conditions do not strongly warrant it or even support it under the Fed's current policy plan.

Central banks: breaking bad?

Central bank policies around the globe have moved into a realm of rarity in which they are not very straightforward to understand. One needs to resort of all sorts of complex thoughts to explain why certain unusual things are being done in the various monetary centers. The simple notion is that central banks are trying to 'do good' but have gone so far from their normally acceptable policy actions that they may be on the verge of 'doing bad.'

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief