Global| Feb 11 2010

Global| Feb 11 2010Federal Reserve Injects Liquidity Into Banks

by:Tom Moeller

|in:Economy in Brief

Summary

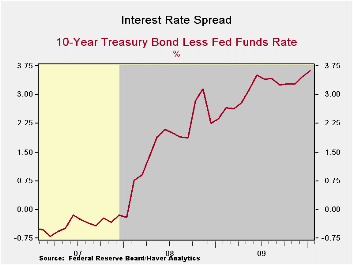

Injection of liquidity by the Federal Reserve into the banking system typically raises inflationary concerns in the credit markets. And this time is no different. Long-term interest rates have remained fairly stable as the Fed funds [...]

Injection of

liquidity by the Federal Reserve into the banking system typically

raises inflationary concerns in the credit markets. And this time is no

different. Long-term interest rates have remained fairly stable as the

Fed funds rate has lingered near zero for over one year. The steepened

yield curve thus suggests a future inflationary problem.

Injection of

liquidity by the Federal Reserve into the banking system typically

raises inflationary concerns in the credit markets. And this time is no

different. Long-term interest rates have remained fairly stable as the

Fed funds rate has lingered near zero for over one year. The steepened

yield curve thus suggests a future inflationary problem.

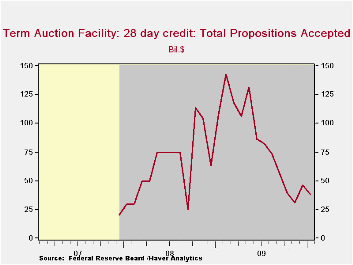

Not only has the Fed held interest rates low, it's provided liquidity to the banks, particularly through its Term Auction Facility (TAF). Through last year this provision fell as banks re-liquefied. But so far, it has not stimulated bank lending and money supply growth has decelerated sharply. Instead, the liquidity has been used to shore up balance sheets.

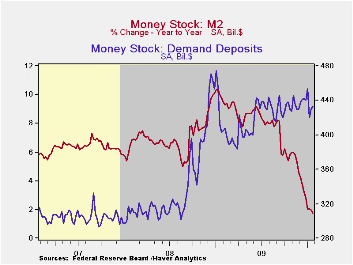

Indeed, money supply growth (M2) has decelerated as demand deposit balances have been flat since the middle of last year. Precaution remains the operative word for banks as they lend and also for individuals who remain cautious about job prospects.

The data referenced above can be found in Haver's WEEKLY database.

Interest on Required Balances and Excess Balances from the Federal Reserve Board is available here. Earlier this week, Chairman Bernanke indicated in Congressional testimony that the interest rate shown here would become a key tool in the Fed's liquidity management going forward. These data are also in Haver's WEEKLY database.

| Liquidity Measures | January | 2009 | 2008 |

|---|---|---|---|

| Reserve Bank Assets - Term Auction Facility | $3,8531M | $7,518 | $450,319 |

| Yield Curve (10 Yr. Treas. less Fed Funds) | 3.62% | 3.10% | 1.74% |

| Money Supply - Demand Deposits | -0.5% y/y | 24.4 % y/y | 11.3 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief