Global| May 10 2021

Global| May 10 2021Exports, Debt, Deficits, Covid-19

Summary

Baltic dry index points to more international freight demand Export trends show only four of eleven of these countries with exports higher over 12 months as of February. However, over six months, 10 of eleven countries show net export [...]

Baltic dry index points to more international freight demand

Baltic dry index points to more international freight demand

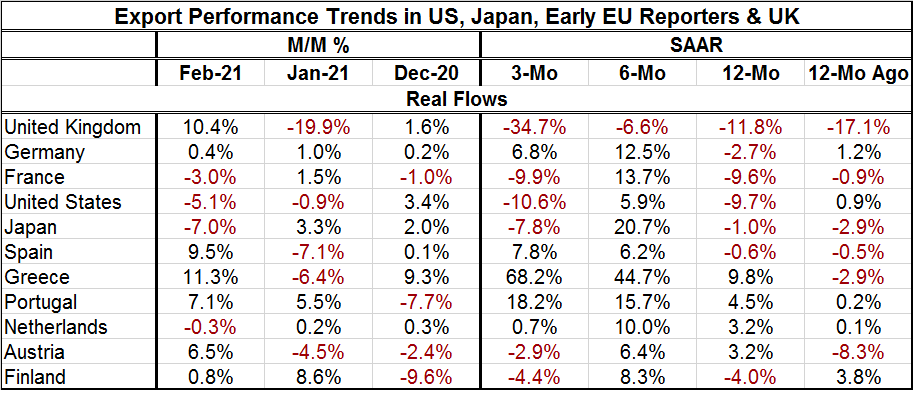

Export trends show only four of eleven of these countries with exports higher over 12 months as of February. However, over six months, 10 of eleven countries show net export gains. Over three months, the picture is mixed with only five countries showing net gains. It does look like exports and growth are reviving, but the speed of revival is uneven.

Covid-19 recovery

The recovery after the Covid-19 infection struck still appears to be in gear, but challenges remain. Not only is Europe mostly 'under-vaccinated, except for the U.K.' but it is clear that the virus continues to change and India's virus assault has to be worrisome beyond just the impact on India. The fact of this virus is that it mutates. While that is normal, some mutations have become very dangerous. And by its nature, mutation is something that cannot be controlled before-hand but rather must be chased after the fact. The U.K. did a good job of reacting to a more lethal and contagious form of the virus when it emerged. That demonstrated that mutations may be able to be dealt with although all we know for sure is how we have dealt with the particular mutations we have seen- not the one we have not seen.

While export revival and shipping volumes globally appear to be on the rise, a number of countries have debt and deficit issues of various sorts.

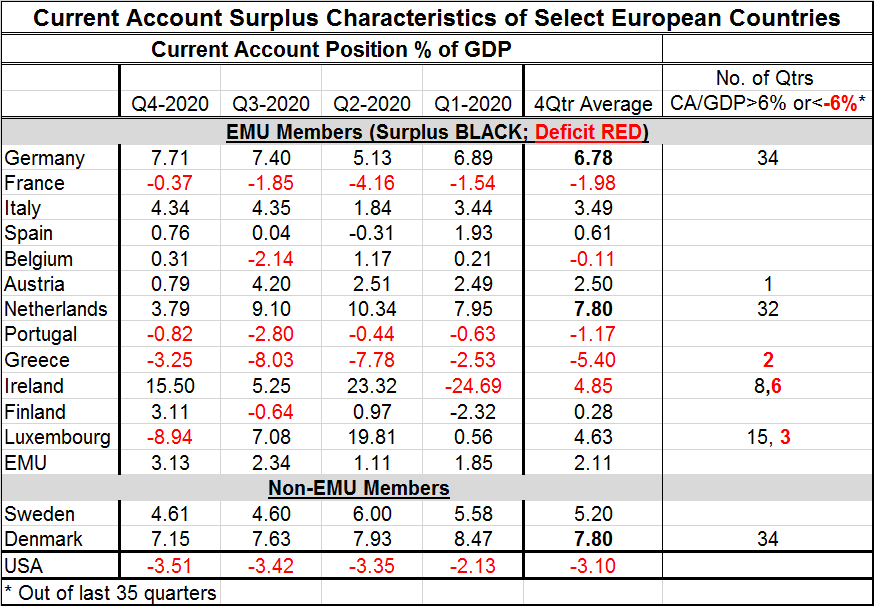

The ratio of the current account position to GDP is long-watched measure to assess balance of payments positions. The table below shows Germany, Denmark and the Netherlands to pursue persistent current account surpluses of a quite substantial magnitude. Denmark and Germany have 34 quarters of surpluses over 6% of GDP over the past 35 quarters while the Dutch have 32. No other countries in the table come close. While the U.S. runs very persistent deficits, its deficits are not as large in a relative sense as the German, Dutch, and Danish surpluses. Greece, Ireland, and Luxembourg are countries that have run large deficits as a share of GDP.

Running persistent surpluses tends to build up a country's foreign exchange reserves; however, it may also mean it is allowing its currency to be 'too weak' and could with a stronger currency increase national purchasing power buy goods abroad more cheaply. A too cheap currency also tends to support domestic exporting, deter importing and support domestic employment. Trade restrictions could also feed into the picture. In the case of EMU countries, conditions are mixed since much of their trade occurs in a frictionless intra-community environment where 'exchange rates' and trade restrictions are not relevant since they all use the same currency and trade under the same rules; only a portion of trade is outside the EMU region where currency values explicitly come into play.

In the wake of Covid-19, countries have run a number of policies that have strained normal fiscal channels and rules.

Ratio-nomics

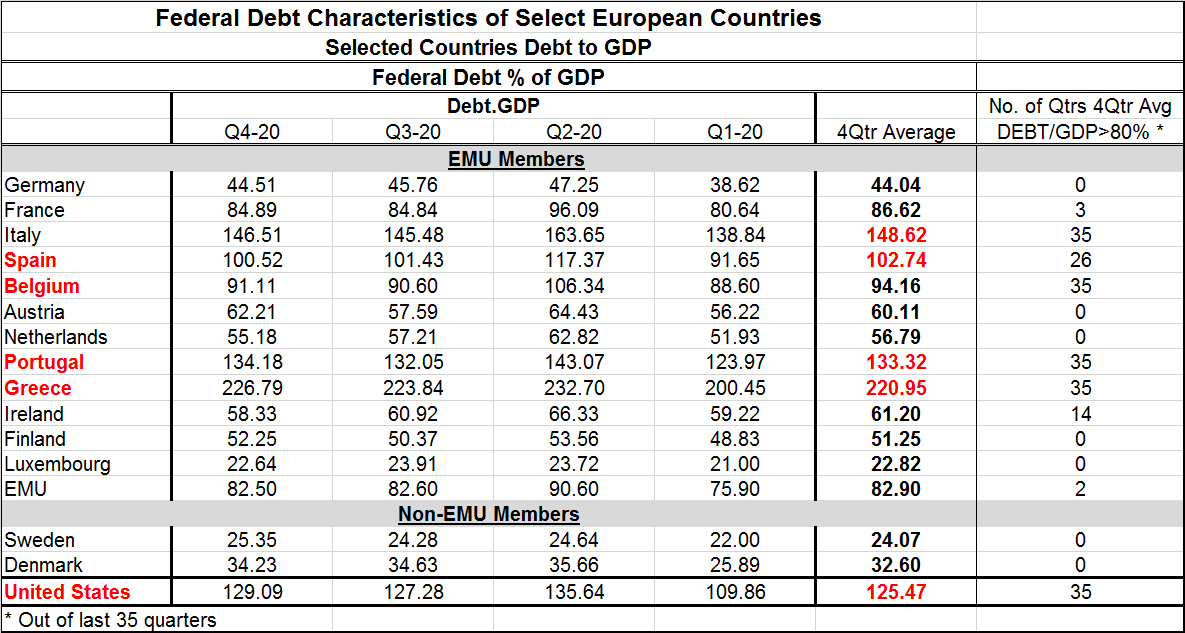

A relatively recent economic book by Rogoff and Reinhart ('This Time It's Different', written in the wake of the Great Recession) found that GDP growth was impaired after national debt levels rose above 100% of GDP. It's not a magic line, more like a crude rule-of-thumb. Greece, Italy Portugal, the U.S., and Spain flash warning signals on this metric as of the end of 2020. And U.S. fiscal spending is still in high gear as 2021 begins.

These calculation are always disputed. This treatment simply looks at central government's stock of debt or in the case of the U.S. 'Federal Debt' as a ratio to GDP. The calculations ignore any other local debt at all.

Of the 16 countries in the table below, only one (Ireland) has a lower debt-to-GDP ratio over five quarters. The biggest increase in the ratio is in Greece, followed by the U.S., Italy, Spain and Portugal. The smallest increases in the ratio are in Ireland, of course, followed Sweden, the Netherlands, Luxembourg and Germany. The 5-quarter percentage point rise in the ratio of debt-to-GDP in Greece and the U.S. surpasses the overall ratio of debt-to-GDP in Luxembourg. The Greek increase nearly equals the ratio of debt-to-GDP in Denmark.

The correlation between a country having a high debt-to-GDP ratio and ranking high on the increase in its debt-to-GDP ratio is 0.8 (0.65 in R-Square terms). Debt begets debt.

Interestingly, the countries of Northern Europe where the economic system is often call 'the third way' tend to have low increases in the debt ratios over the last five quarters. Sweden, Denmark and Finland rank 15, 11, and 9 respectively out of 16 countries in terms of the increase in their debt-to-GDP ratio over five quarters. The U.S., the country with the most capitalist system and the smallest amount of safeguards has the second largest increase in its debt-to-GDP ratio. After that the countries that had the most persistent debt and inflation problems before the EMU was formed tended to rank very high: Greece (1), Italy (3), Spain (4), Portugal (5), and France (8).

However, if we view a small rise in the debt-to-GDP ratio as evidence of financial or institutional preparedness, that did not translate to handling the virus better. Among this group, especially among large economies, the U.S. and the U.K. have done the best; among smaller countries the Danes have done quite well too. I think if there is a lesson, it is that it is better to have a healthcare response at the national level since the EU Commission seems to have stumbled badly setting behind recovery efforts across all of Europe.

What are ratios good for?

Financial ratios are never going to tell us all we want to know. And some economists are trying to decouple policies from the practice of looking at these ratios arguing that interest rates are low so higher debt-to-GDP ratios can be afforded. Well, there's a circular argument if ever I heard one. It is a tautology and for that reason it is useless. We need to know first for a fact that rates are going to stay low before we use that FACT (not possibility) to justify higher debt-financed public spending. Since we do not know what rates will do, asserting a result does not help with the decision process. There is also modern monetary theory that asserts among other things that a country can borrow great amounts as long as it can borrow in its own currency. That is another rule on thin ice since the country that can borrow in its own currency then slips up and over-borrows going past its limit and finds capital market access shut-off suddenly no longer fits the bill but it probably still has a financial situation established that required more borrowing.

Policymaking with uncertainty

Assessing borrowing power and optimal debt is difficult and the solutions people get are really nothing more that the assumptions that the make- if you look closely at these things. I think the key issue in optimal borrowing is: what policy makes sense given that there is uncertainty? Would you really want a program set up to borrow vast sums side-tracked while in progress after losing access to capital markets? Or after having raised debt-to-GDP levels, would you like to find interest rates were not going to stay low after all? What is gained by this borrowing binge compared to what is risked? Viewed in that way, I think the old metrics on debt-to-GDP ratios looks much more attractive and insightful. They create the kind of guidelines that would allow central bankers and others who worry about policy to sleep at night.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief