Global| Feb 17 2009

Global| Feb 17 2009Exports and Imports Plunge in the Euro Area as Deficit Contracts

Summary

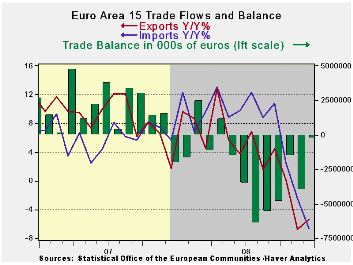

Recession has hit the Euro Area trade flows hard as exports already lower by 6.8% lower in November fell by another 0.9% in December. But imports that fell by 4.8% on November fell by a further-chilling 3.9% in December. The [...]

Recession has hit the Euro Area trade flows hard as exports

already lower by 6.8% lower in November fell by another 0.9% in

December. But imports that fell by 4.8% on November fell by a

further-chilling 3.9% in December. The confluence of these trends

shrank the EMU trade deficit in December to Eur 257mln from Eur 4.0 Bln

in November. Yr/Yr exports are lower by 5.4% compared to imports which

are down by 6.6%. Over three months the annual rates of decline are

-35% for exports and -43% for imports. Over the last six months the

pace of decline has accelerated sharply. Yr/yr numbers do not begin to

show the depth of the problem.

German finance minister Steinbrueck warned that Euro-region

countries may be forced to bail out other members of the 16-nation bloc

that face problems refinancing their debt. “Some countries are slowly

getting into difficulties with their payments,” Steinbrueck said late

yesterday in a speech in Dusseldorf. “The euro-region treaties don’t

foresee any help for insolvent countries, but in reality the other

states would have to rescue those running into difficulty.” This

underscores the degree of difficulty of economic times in Europe. Also

underlining that tough sledding is the warning by the rating agency

Moody’s today. Moody’s cautions that banks with substantial lending

exposure to Eastern Europe could be downgraded. Thus another class of

assets (Eastern European loans) has gone bad. Of course the banks with

the most of this type of lending are European. Emerging Europe is being

called the ‘sub-prime’ of Europe.

| Euro Area 13 - Trade trends for goods | |||||

|---|---|---|---|---|---|

| m/m% | % Saar | ||||

| Dec-08 | Nov-08 | 3M | 6M | 12M | |

| Balance* | €€ (257) | €€ (4,005) | €€ (1,922) | €€ (3,760) | €€ (2,235) |

| Exports | |||||

| All Exp | -0.9% | -6.8% | -35.3% | -17.1% | -5.4% |

| Food and Drinks | -- | -3.0% | -7.1% | -3.3% | 1.6% |

| Raw materials | -- | -13.0% | -60.4% | -34.9% | -12.2% |

| MFG | -- | -4.0% | -24.7% | -10.8% | -6.6% |

| Imports | |||||

| All IMP | -3.9% | -4.8% | -43.4% | -21.0% | -6.6% |

| Food and Drinks | -- | -2.9% | -15.1% | -7.8% | -3.7% |

| Raw materials | -- | -0.4% | 4.5% | 4.8% | 8.3% |

| MFG | -- | -0.5% | -8.2% | -1.8% | -1.3% |

| *Eur mlns; mo or period average; Gray shaded areas lag one month | |||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief