Global| Jul 15 2013

Global| Jul 15 2013Export Trends Tell an Uneven Story of Growth

Summary

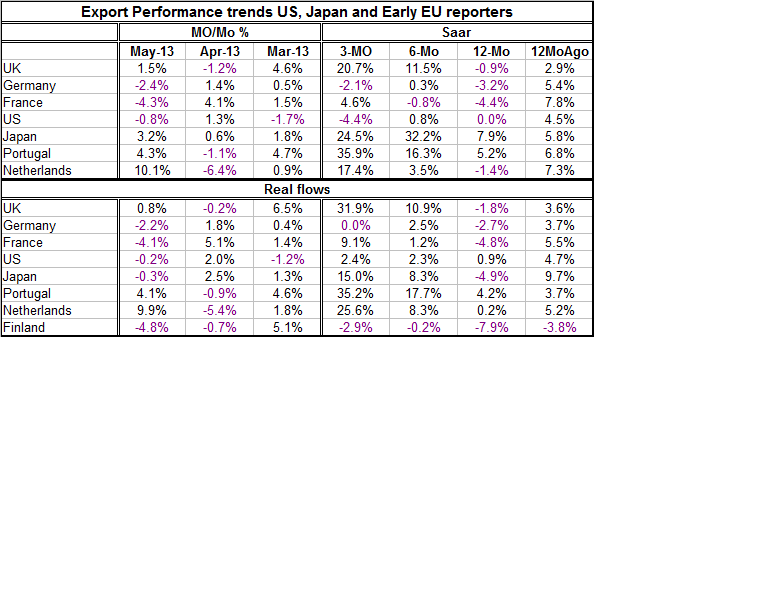

Export trends in the current month appear to be negative with real export flows in five of eight countries in the table showing negative trends in May and four of them showing negative results in April. However, over three months [...]

Export trends in the current month appear to be negative with real export flows in five of eight countries in the table showing negative trends in May and four of them showing negative results in April.

Export trends in the current month appear to be negative with real export flows in five of eight countries in the table showing negative trends in May and four of them showing negative results in April.

However, over three months there is only one country with declining real exports that's Finland at -2.9% with Germany - surprisingly -at zero.

Over six months again there are positive trends in all the countries except Finland where flows are still declining.

Year-over-year, the data that appear in the chart above are among the most dismal trends with declines in five of the eight countries and relatively weak growth in two others.

These results suggest that exports, while mostly lower year-over-year, are beginning to find some traction and may be headed for stronger growth ahead. The strongest trends are in Portugal, in the UK and in the Netherlands followed by some considerable strength in Japan at least over three months. Portugal has done a good job in expanding markets outside of the Economic Union which continues to have a good deal of weakness. Germany, which we traditionally look at as the most competitive of the European economies, may be seeing the repercussions of having reallocated too much of its export volume to China where the growth rate is still one of the best in the world but where growth is increasingly challenged.

From six months Japan, with the adoption of its new monetary policy and some weakness in the yen, sees its export growth beginning to pick up. Growth rises to 8.3% over six months from -4.9% over 12 months and has recently accelerated to a 15% annual rate over the most recent three months.

The US, where domestic growth continues to underperform historic norms but where there is some hope that there will be some acceleration, shows very little life in its exports with real flows up 0.9% year-over-year and then running at approximately at 2.4% annual rate over three months and six months. US flows are facing not only weak global markets but also some increase the dollar's strength.

The surprising story in this table is the story of improvement Portugal and in the Netherlands as well as the building strength in the UK.

Eurozone growth is still faltering. Growth in the BRIC countries remains under pressure. In reality there is a dearth of domestic demand to drive exports. Over short periods of time exports can find some purchase and send growth rates higher but a show of volatility may not represent strength

We would judge Japan to be experiencing volatility that represents renewed strength because the Japanese flows are underpinned by a substantial improvement in competitiveness; the yen has declined in value. As for Portugal, the Netherlands and the UK all the trends are impressive and do extend back at least six months. Still question marks remain. Of these, Portugal may have the most solidity to its flows because it has improved competitiveness and it has sought out third markets outside of the European Union to try to secure its exports.

The big question mark is of course Germany. Real German export orders have continued to grow slowly rather than to contract. Is the slowing in China really hurting German exports so much?

Global trends continue to make it difficult to buy into notions of very strong export growth anywhere. We will watch the upstart trends for countries that seem to be showing export strength to see if it's real or just volatility. These trends for the moment raise a few more questions than they answer. There really isn't evidence of a pick-up in global demand to support expanded exports nor do we see in The Netherlands or the UK a shift in competitiveness to explain exports' renewed vigor.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief