Global| May 16 2008

Global| May 16 2008Export Trends Are Faltering in Europe As Imports Sustain

Summary

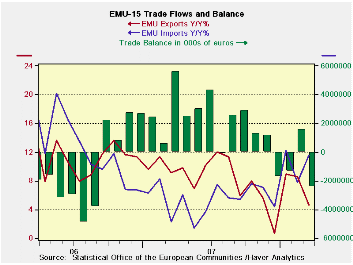

European exports fell across the board in March as imports were steady. This plunged the trade balance back into deficit. Sequential growth rates are still upbeat with exports accelerating over 12-mo to 6-mo to 3-mo. But imports are [...]

European exports fell across the board in March as imports

were steady. This plunged the trade balance back into deficit.

Sequential growth rates are still upbeat with exports accelerating over

12-mo to 6-mo to 3-mo. But imports are accelerating even faster on this

sequence. Over a broader swath of time the Yr/Yr trends show that

imports are outpacing exports and that import growth has been firmer

while export growth is fading (see chart). Indeed, there is no reason

to believe the message in the short-term sequential growth rates since

the euro keeps climbing and undermining export growth prospects. Also

growth surveys in Europe are getting progressively weaker. We did get a

surprise pop in GDP growth in 2008-Q1 – but would you want to take that

one to the bank?

Euro- Japan growth figures are less prone to adjust for the

extra leap day that we had in the first quarter. Moreover, GDP’s

‘resilience only implies that the effects of the slowdown are being

gradually phased in. Weakness in orders and in consumer confidence will

lead to weaker economic growth overall in Europe. Sometimes the lag

between what the surveys predict and what happens is longer than

expected, but the survey message is clear and so widespread it is

unlikely to be wrong.

While Germany’s DIW has hiked its growth outlook for German

growth in Q2, maybe it should be cutting it instead... Often unexpected

strong growth turns out to have borrowed growth from subsequent

quarters. One thing it does is to RAISE the level of spending to a

point that if spending goes back to trend a downside growth number will

emerge in the next quarter – that’s the arithmetic of it. In the case

of Germany and Europe I think that sort of a setback – or something

even more dramatic-- is a likely outcome in 2008-Q2.

| Euro Area 13-Trade trends for goods | ||||||

|---|---|---|---|---|---|---|

| m/m% | % Saar | |||||

| Mar-08 | Feb-08 | 3-Mo | 6-Mo | 12-Mo | 12-Mo Ago | |

| Balance* | €€ (2,382) | €€ 1,567 | €€ (714) | €€ (236) | €€ 1,144 | €€ 50 |

| Exports | ||||||

| All Exports | -2.9% | 0.6% | 18.2% | 3.2% | 4.6% | 9.1% |

| Food and Drinks | -1.4% | 0.6% | 10.9% | 4.2% | 7.4% | 9.3% |

| Raw materials | -0.4% | 1.2% | 35.4% | 10.0% | 8.4% | 11.6% |

| Other | -3.1% | 0.6% | 18.3% | 3.0% | 4.3% | 9.0% |

| MFG | -4.8% | 1.4% | 11.9% | -4.8% | -0.1% | 11.2% |

| Imports | ||||||

| All Imports | 0.0% | -1.5% | 20.3% | 12.2% | 11.6% | 2.4% |

| Food and Drinks | -3.3% | -2.0% | -11.7% | -6.3% | 7.0% | 7.5% |

| Raw materials | 0.4% | 0.6% | 10.5% | 6.2% | 5.2% | 14.4% |

| Other | 0.2% | -1.6% | 23.1% | 13.7% | 12.2% | 1.5% |

| MFG | -3.2% | -0.4% | 4.0% | -7.6% | -0.9% | 9.8% |

| *Eur mlns; mo or period average | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief