Global| Dec 28 2006

Global| Dec 28 2006Existing Home Sales Also Up in November; Prices Are Down Slightly, but Supply Overhang Shrinks a Bit as Market [...]

Summary

After existing home sales had increased modestly in October, economists looked for them to retreat in November by about half of their October rise. Instead, the National Association of Realtors reported this morning, these home sales [...]

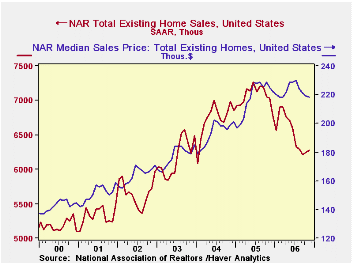

After existing home sales had increased modestly in October, economists looked for them to retreat in November by about half of their October rise. Instead, the National Association of Realtors reported this morning, these home sales increased further. It's a mild gain of just 0.6%, following October's 0.5% and these sales are still more than 11% lower than year-ago volume. But as with the new home sales report yesterday, the unexpected move suggests that the housing market may well be stabilizing. Sales of single-family homes inched ahead 0.2%, and October volume was revised slightly higher to a 1.5% rise from 1.3% reported initially.

By region, sales rose 6.0% in the Northeast and 0.8% in the West. They were flat in the Midwest and continued to fall in the South, this time by 1.6%.

Home prices fell by 0.5% for all existing home sales and by 1.1% for single-family houses alone. October's prices for total sales were revised down, so they now show a mild decline then and four monthly decreases running. Notably, though, prices in the Northeast and in the West both had good increases, 5.1% and 2.6%, respectively.

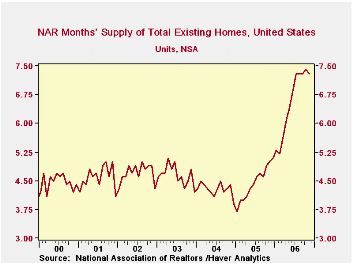

The inventory of "homes on the market" fell by 1.0%, renewing the slight downtrend that had begun in August, after a 2.0% rise in October. At current sales rates, it now amounts to 7.3 months' of sales, just below October's 7.4 months.

The entire housing market, new and existing, experienced rising sales in November. These increases were small but unexpected. Inventories of unsold homes also fell in both market segments, improving the underlying condition of the markets. We don't want to make too much of these developments, but they are encouraging. Support from more moderate interest rates, flexible pricing and lower energy prices all surely helps.

The broad aggregate data on existing home sales are included in Haver's USECON database; details about prices by region and inventories are available in the REALTOR database.

| Existing Home Sales (SAAR, 000s) | Nov 2006 | Oct 2006 | Sept 2006 | Year/ Year | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|---|

| Total Sales | 6,280 | 6,240 | 6,210 | -11.1% | 7,074 | 6,782 | 6,176 |

| Single-Family Sales | 5,520 | 5,510 | 5,430 | -11.5% | 6,178 | 5,962 | 5,444 |

| Median Single-Family Home Price (NSA,000s) | $217.2 | $219.6 | $221.1 | -3.6% | $217.5 | $192.8 | $178.3 |

by Carol Stone* December 28, 2006

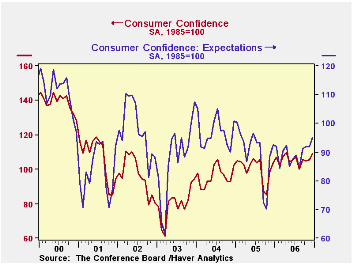

Consumer confidence rose in December, according to the Conference Board's monthly survey. It went up 3.7 points to 109.0 (1985=100), the highest reading since April. November's figure was revised upward by 2.3% from 102.9 reported a month ago. Both major components, assessments of present conditions and expectations for the coming six months, contributed to December's rise, adding 4.5 points and 3.2 points, respectively. This outcome differs from the University of Michigan survey, which eroded a bit on diminished expectations. It also differs from consensus forecasts, which had looked for a decrease from the original 102.9 to 102.1.

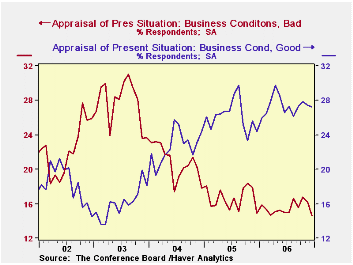

"Present conditions" are measured by responses about general business conditions and the status of labor markets. This month, ironically, fewer consumers said they see business conditions as "good", but the number saying they are "bad" decreased more. There appears to be some improvement in the availability of jobs, as the number seeing jobs as "plentiful" increased 1.2 points, although at 26.9%, that remains below the first seven months of 2006. The proportion of consumers believing jobs are "hard to get" also rose a bit, but just 0.9 point; this too has a less favorable reading than what prevailed in the first half of 2006.

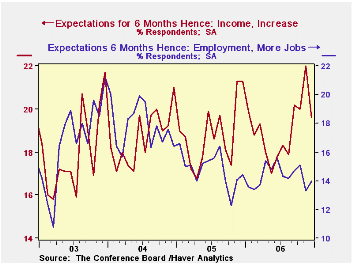

Expectations are mixed. The share of consumers looking for "more jobs" increased 0.7 point to 14.0%, but paradoxically the share expecting their income to go up decreased by 2.4 points. Sources of the rise in expectations are actually more "back-handed": fewer people expect business and employment conditions to worsen.

So, despite the favorable appearance of the overall consumer confidence indexes, the details suggest that people remain skittish. Results concerning interest rates and the stock market also indicate this ambivalence: while many fewer people are looking for higher interest rates, the number of people looking for higher stock prices is down and the number looking for lower stock prices is up. Stay tuned!

| Conference Board (SA, 1985=100) |

Dec 2006 | Nov 2006 | Oct 2006 | Dec 2005 | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|---|

| Consumer Confidence Index | 109.0 | 105.3 | 105.1 | 103.8 | 105.8 | 100.3 | 96.1 |

| Present Conditions | 129.9 | 125.4 | 125.1 | 120.7 | 130.1 | 116.1 | 94.9 |

| Expectations | 95.1 | 91.9 | 91.9 | 92.6 | 89.6 | 89.7 | 96.9 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief