Global| Nov 06 2009

Global| Nov 06 2009Everybody Is Turning Higher Say OECD LEIs

Summary

In the OECD area everything is coming up roses. Some are more in bloom than others and some have more thorns than others but the OECD gave a very upbeat assessment to activity in the OECD areas. OECD leading indicators ... “point [...]

In the OECD area everything is coming up roses. Some are more

in bloom than others and some have more thorns than others but the OECD

gave a very upbeat assessment to activity in the OECD areas.

OECD leading indicators ... “point strongly to growth in

Italy, France, the United Kingdom and China, while tentative signals of

expansion have emerged in Canada and Germany," the OECD said. "A

recovery is clearly visible in the United States, Japan and all other

OECD economies and major non-OECD economies," it added.

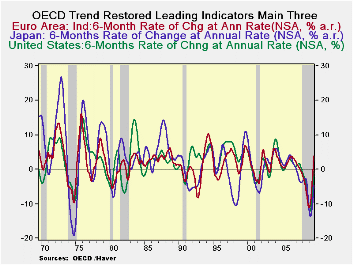

The OECD indicators selected in the table above all show

strong (double digit) increases over the recent six months expressed as

annual rates of growth. Simple three-, six- and twelve-month growth

rates are positive across all these countries/groups with the exception

of 12 month growth in Japan (see top panel of the table above). The

OECD data are up-to-date though September.

Echoing this sentiment are the new industrial orders for

September released today by Germany that find orders on the growth path

for the seventh month in row. The problem for Germany is that now

domestic orders have dropped for the second month in a row. The two

month drop which amounts to a bit more than a 3% set back comes on the

heels of a 9.5% monthly rate super spike in domestic orders for July.

Still foreign orders continue to expand and Germany’s domestic orders

are not along for the ride.

The OECD data show us why German export orders are rising:

that export oriented economy exports goods globally and the whole OECD

area is having a nice snap back. But Germany is still an important

country in EMU, the largest economy there. Having the German domestic

factory sector so weak on top of previously-reported weakness in German

retail sales, is a clear warning sign to not get too carried away by

optimism.

The OECD area is snapping back from a very ugly recession. But

the recession was so ugly that the snap back can look strong but still

fail to bring growth to a strong enough point to spur a drop in

unemployment. That’s exactly what we seeing in the US. Despite a US MFG

sector that has been posting good results, increases in industrial

production and a rise to strong level for the MFG ISM, the US is not

seeing job growth. Europe is finding some growth deficiencies as well.

Today the UK got an unexpected visit from a higher PPI. The OECD area

is not strong enough to be abele to cope with any inflation signals

just yet. Let’s hope the UK PPI is just a rogue signal. Meanwhile, we

need enough economy strengthening to create job, income and spending

growth while allowing savings to make some headway as well. It’s a tall

order that we are falling short on despite the growth path endorsed by

the OECD.

| OECD Trend-restored leading Indicators | ||||

|---|---|---|---|---|

| Growth progression-SAAR | ||||

| 3Mos | 6Mos | 12mos | Yr-Ago | |

| OECD | 15.8% | 14.9% | 1.5% | -6.5% |

| OECD7 | 16.8% | 15.3% | 0.5% | -6.9% |

| OECD.Ezone | 16.9% | 16.6% | 4.0% | -7.9% |

| OECD.Japan | 13.1% | 10.9% | -4.7% | -4.5% |

| OECD US | 16.8% | 15.0% | -0.6% | -6.7% |

| Six month readings at 6-Mo Intervals: | ||||

| Recent six | 6Mo Ago | 12Mo Ago | 18MO Ago | |

| OECD | 14.9% | -10.3% | -10.5% | -2.3% |

| OECD7 | 15.3% | -12.3% | -10.7% | -3.0% |

| OECD.Eur | 16.6% | -7.3% | -12.3% | -3.3% |

| OECD.Japan | 10.9% | -18.1% | -9.2% | 0.4% |

| OECD US | 15.0% | -14.2% | -9.8% | -3.5% |

| Slowdowns indicated by BOLD RED | ||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief