Global| Feb 12 2010

Global| Feb 12 2010Every Picture Tells A Story...Or Do It?

Summary

Don’t judge a book by its cover- Please pardon the bad grammar in the title. But I am hopelessly imprinted with Rod Stewart’s, “Every Picture tells, a story, don’t it?’ In this case… I wonder: does it or as SNL’s Seth Meyers might [...]

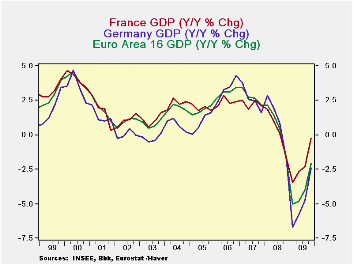

Don’t judge a book by its cover- Please pardon the bad grammar

in the title. But I am hopelessly imprinted with Rod Stewart’s, “Every

Picture tells, a story, don’t it?’ In this case… I wonder: does it or

as SNL’s Seth Meyers might ask: ‘does it, does it really?’ What I mean

is this: does the picture tell THE story? The story in the picture

above is quite clear that GDP in Europe is getting better and at a fast

rate. The DROP in GDP is cut sharply in its Q4 embodiment compared to

its Q3 embodiment for EMU, Germany and for France.

Digging deeper -- Yet read ANY market story on these results

for today. The clear theme is one of disappointment. Why are people

disappointed if the Yr-over-Yr drops in GDP are dissipating so fast?

It’s because a percentage change is a function of TWO things, the

current value and the past value that forms the base for the percentage

change calculation. And the BIG DROP OFF in the pace of GDP’s decline

Yr/Yr in Europe is more due to a shift in the base than to the result

in the new quarter. In the new quarter GDP rose by only 0.4% at an

annualized rate (that’s a thin 0.1% Q/Q). So why did the yr/yr pace

improve so much? It’s because of the shift in the base to Q4 2008 from

Q3 2008. In Q4 2008 EMU GDP fell by 7.4% at an annualized rate. Compare

that to its 2.7% decline in Q3 of 2008. What this means is that we are

comparing growth in Q4 2009 to a much lower base than we did in

2009-Q3, so even a small amount of growth (like 0.1% in the quarter)

makes the Yr/Yr comparison look much better than it did in Q3. It’s

base-illusion.

Euro-sclerosis strikes again - The simple fact is that

Europe’s recovery is slowing down. The US is speeding up. Europe’s

vaunted social welfare system may have helped to mitigate the declines

in GDP in the recession but in recovery it is providing no springboard

for growth. Meanwhile, the US recovery is powering ahead. We are set up

for the usual sort of configuration in global growth where the US

economy becomes the engine of growth for the global economy as the US

current account deficit rips a gaping hole in the US balance of

payments and feeds stimulus to the rest of world like a mother

breastfeeding her helpless infant child.

You put the load right one me…One problem with this emerging

scenario is that the US consumer is not is the shape he/she usually is

in a recovery and may not be able to suckle the global economy. While

US retail sales were better than expected in January the result is

still less that robust. It is not clear how much lift the US consumer

will add to the US recovery let alone to the economies of the rest of

the world. The US does import a lot of consumer goods. So a recovering

US consumer will purchase imports. But how many imports can the US

consumer buy if US growth goes flat as the diverted income and blunted

multiplier from surging foreign exports to the US stunt economic growth

back home?

The blame game - Get ready for the rest of the world to start

blaming the US for widening deficits even as the US consumer fuels

recovery in Europe and beyond. The simple fact is that China, Japan and

Europe- especially Germany- all want to have export-led growth. They

act as though it’s a right. If they do who will import? China and Japan

have amassed huge foreign exchange reserves, an act that clearly has

facilitated their currencies, remaining weaker than otherwise, enabling

their strategy of export-led growth while at he same time undermining

US growth and US finanical health..

Europe and the 800 pound gorilla - We do not yet have

consumption figures for Europe’s flash GDP results. Flash-GDP is

usually just a total and may be accompanied by some descriptive

comments but little or no supporting details on GDP. Be sure that this

paltry performance from GDP in Europe is not good news. The hike in

reserve requirements in China has people worried about in growth there

as well. There is a theme of growth pessimism taking hold again

clobbering global stock markets. But China is a taker- an exporter- not

a giver. It does not provide net domestic demand to the world. Its

growth merely absorbs income from elsewhere transforming it into growth

for…CHINA! In turn that helps to pressure global input prices

(commodity prices). Strong growth in China is usually not beneficial to

the West. People who profess worry over China growth prospects don’t

get it. It’s a big and growing ever more complicated world. Be sure to

know the facts. Markets often react to overall themes and only later

get more sophisticated by sorting out winners and losers. Right now

there is an emerging theme of weakness. Europe is faltering China may

slow. There are still lingering concerns about the status of growth in

the US…Weakness abroad will have repercussions for the US, but the US

recovery is still on track. So don’t throw out the baby with bath water

in your haste to dump dropping stocks. Markets will eventually ‘get it

right’ and face a truer version of reality. China may be an 800 pound

gorilla but if he is sick and starts eating fewer bananas, there are

more for you.

| European Growth for Selected Flash GDP Results | ||||||

|---|---|---|---|---|---|---|

| Q/Q Saar | Yr/Yr | |||||

| Q4-09 | Q3-09 | Q2-09 | Q4-09 | Q3-09 | Q2-09 | |

| Austria | 3.8% | 9.9% | -3.1% | -1.4% | -3.1% | -5.4% |

| France | 2.4% | 0.7% | 1.4% | -0.3% | -2.3% | -2.7% |

| Germany | 0.0% | 2.9% | 1.8% | -2.4% | -4.8% | -5.8% |

| Greece | -3.1% | -1.9% | -1.2% | -2.6% | -2.5% | -1.9% |

| Italy | -0.9% | 2.6% | -1.9% | -2.8% | -4.6% | -5.9% |

| Netherlands | 1.0% | 2.1% | -4.2% | -2.6% | -4.0% | -5.2% |

| EMU | 0.4% | 1.7% | -0.5% | -2.1% | -4.0% | -4.8% |

| Memo:US | 5.7% | 2.2% | -0.7% | 0.1% | -2.6% | -3.8% |

| Memo:UK | 0.4% | 1.7% | -0.5% | -2.1% | -4.0% | -4.8% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief