Global| Mar 26 2018

Global| Mar 26 2018Eurozone Economic Outlook from IFO, Istat and KOF

Summary

According to the Eurozone Economic Outlook that is jointly published by the IFO Institute, Italy's statistical office Istat and the KOF Swiss Economic Institute, EMU area GDP is projected to grow 0.6% each in the first and second [...]

According to the Eurozone Economic Outlook that is jointly published by the IFO Institute, Italy's statistical office Istat and the KOF Swiss Economic Institute, EMU area GDP is projected to grow 0.6% each in the first and second quarters of 2018. Growth is expected to slow slightly to 0.5% in the third quarter. The forecast sees investment as the main force behind the expansion (find forecast here). This group forecasts over a period of three quarters: the current quarter and the next two. Today’s projections cover Q1, Q2 and Q3 of 2018.

According to the Eurozone Economic Outlook that is jointly published by the IFO Institute, Italy's statistical office Istat and the KOF Swiss Economic Institute, EMU area GDP is projected to grow 0.6% each in the first and second quarters of 2018. Growth is expected to slow slightly to 0.5% in the third quarter. The forecast sees investment as the main force behind the expansion (find forecast here). This group forecasts over a period of three quarters: the current quarter and the next two. Today’s projections cover Q1, Q2 and Q3 of 2018.

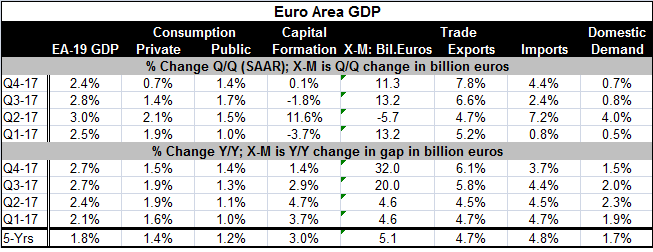

This outlook is very different from the path the EMU economy has taken to get here. The first half growth rate corresponds to a pace of 2.4% which is the same as the EMU pace for Q4 2017 and slower than the 2017 year-on-year pace of 2.7%.

Looking at year-on-year growth trends over the four quarters of 2017, the growth of investment in the EMU has generally been fading. Consumption was weak in the four quarters ending in Q1 2017 and in the four quarters ended in Q4 2017 but in the middle two quarters’ consumption had picked up.

One leading force for growth in the EMU has been net exports. Their impact over four quarters has steadied growth throughout 2017 as export growth more or less steadily accelerated. At the same time, import growth gradually and slightly backed off. Domestic demand as a whole was week in Q4 and in Q1 and was more solid in the middle quarters of 2017 following the pattern of private consumption. Public consumption in the EMU gradually strengthened in 2017.

The Eurozone Economic Outlook also sees inflation remaining well below its objections (of just less than 2%) in 2018, but it is still expected to accelerate. The group’s inflation forecast assumes that oil stays at $66/barrel and that the USD/EUR exchange rate stays at 1.23 over the forecast period.

The group’s forecast is fresh enough to contain some statements with caveats about the new Trump trade tariffs and the potential for world trade to be disrupted. All economists worry about these things. Trade wars are dangerous and very disruptive in this age with such advanced and intertwined global supply chains. Europe is also at risk to the decision of the ongoing Brexit negotiations.

Europe is especially worried about the new trade environment. German nominal exports are at a ratio of 48% to GDP with imports at 40% of GDP. Europe is extremely trade dependent. Of course, a lot of that trade never crosses the exchange rate since it is intra-union trade. Still, anything that interrupts trade patterns will worry Europeans.

The freshest news on the Trump trade action is that maybe it is more clever and impactful than most gave it credit for. The early analysis about the steel and aluminum tariffs was that they were not well designed and not even well articulated. But over the weekend, the U.S. has announced that it has a modification on the six-year-old trade agreement with South Korea that Trump has sought. Further lowering tensions are reports that the U.S. and China are talking about trade. President Trump has said that it is possible for the U.S. and China to resolve their differences without ever imposing these tariffs.

While many have viewed Trump as a bull in the international china shop being not careful and breaking things it took years to establish, it appears that the Trump strategy was to make a lot of noise, get a lot of attention, raise some fears then cut some deals. Those Trump critics have generally made three mistakes. They underestimate him, they saw tariffs as a permanent fixture not as crow bar to use to gain leverage and they have misinterpreted Trump’s views on deficits which are a good deal more sophisticated than what he simply says in public.

On balance, Europe looks set to continue to grow. I’m not so sure that it will be investment-led growth as this forecast has it, but certainly global growth and trade will be supporting factors. We have a more hopeful situation in which the trade troubles may be dealt with more smoothly in the wake of the news of this weekend about a deal stuck with South Korea. There are still dangers lurking. But the trade environment is looking less hostile and potentially more promising for the U.S.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief