Global| Jun 30 2015

Global| Jun 30 2015European Trends Are on Hold as Greece Boils

Summary

EU unemployment was steady in May as the same 9.6% rate as in April. EMU unemployment was steady at 11.1%. The number of unemployed continues to fall in both the EMU and the EU but not enough to lower the month-to-month unemployment [...]

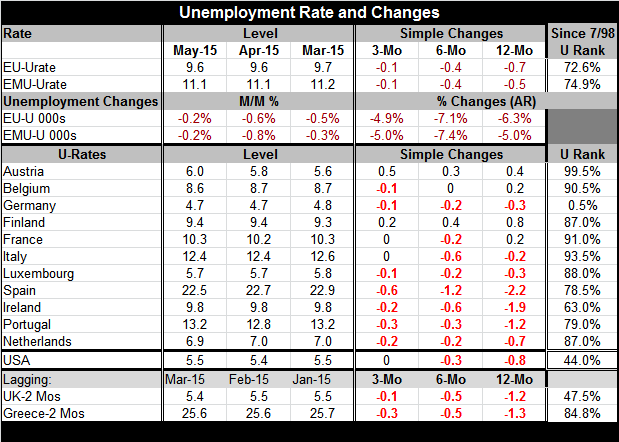

EU unemployment was steady in May as the same 9.6% rate as in April. EMU unemployment was steady at 11.1%. The number of unemployed continues to fall in both the EMU and the EU but not enough to lower the month-to-month unemployment rate. Year-over-year, the number of unemployed in the EU is lower by 6.3%, and in the EMU it is lower by 5.0%. The EU unemployment rate is lower by 0.7 percentage points year-over-year and the EMU rate is lower by 0.5 percentage points.

EU unemployment was steady in May as the same 9.6% rate as in April. EMU unemployment was steady at 11.1%. The number of unemployed continues to fall in both the EMU and the EU but not enough to lower the month-to-month unemployment rate. Year-over-year, the number of unemployed in the EU is lower by 6.3%, and in the EMU it is lower by 5.0%. The EU unemployment rate is lower by 0.7 percentage points year-over-year and the EMU rate is lower by 0.5 percentage points.

By EMU member countries with data available through May, the unemployment is higher year-over-year in four countries: Austria, Belgium, Finland and France. These are not peripheral nations. Unemployment is lower in seven countries; unemployment lower by one percentage point or more in three countries (Portugal, Ireland and Spain, three of the countries that have struggled with austerity). Over three months, unemployment is net higher in only one country, Austria. Greece's unemployment data lag but they show a drop in its unemployment rate of more than one percentage point over 12 months. Greece has declines logged over three months and six months. That is at least up through March, more recently all the protesting may have created a setback.

The HIPC inflation rate that had been on the rise in the EMU, backtracked in June, rising by just 0.2% over 12 months, lower than the 0.3% 12-month rise logged the month before. But there is little evidence of any relationship between inflation and unemployment trends for the EMU. Both the unemployment rate and the inflation rate have been falling over the past several years.

The EMU and EU regions are still struggling but making progress. However, in some countries progress, has been more painful than in other places. Greece has been making economic progress, but it has found the cost of progress too severe and is in the midst of a full-scale rebellion with its lending overlords. For the time being, Spain and Portugal are still on board with the EMU and making progress, but Spain has a Podemos, an anti-austerity party that has gained in popularity. Portugal and Italy could be candidates for unrest over austerity depending on the future speed of growth and on what precedent is created in Greece.

Progress at this point is not enough. Countries have endured such high rates of unemployment for so long that they need not just progress, but greater speed for growth. While Greece's situation will not necessarily spawn contagion, its circumstance could open the door for others to be introspective about their future. If one country leaves the EMU, it is unclear how international investors will view the remaining euro area, as stronger or as more likely to fracture again.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief