Global| May 21 2014

Global| May 21 2014European Trade Trends Show Divergence

Summary

European Union member trade trends have shifted from their past trends early in 2014. The exports of Finland, Portugal, France and Germany have turned lower after showing signs that the growth rate of exports may have bottomed in [...]

On the import side, we see persistent weakness and contraction in Italian imports with no sign of an incoming pickup. French exports have been weak as well, but they are also moving sideways at a growth rate that is essentially zero. Greek imports never did rise with a boost from domestic demand that these other EMU member countries experienced in 2010 and 2011. During that period, Greek imports remained weak, continued oscillating around the zero line and showed contraction in 2012. In late 2012/early 2013 imports around the euro area weakened. However, over the past six months or so, Greek imports have been flat with perhaps a slight tendency to increase. Germany, the strong man of Europe, shows only a very recent tendency for its imports to increase. In March, their increasing growth and trend bent slightly lower. French imports are still flat and Italian imports are still dropping.

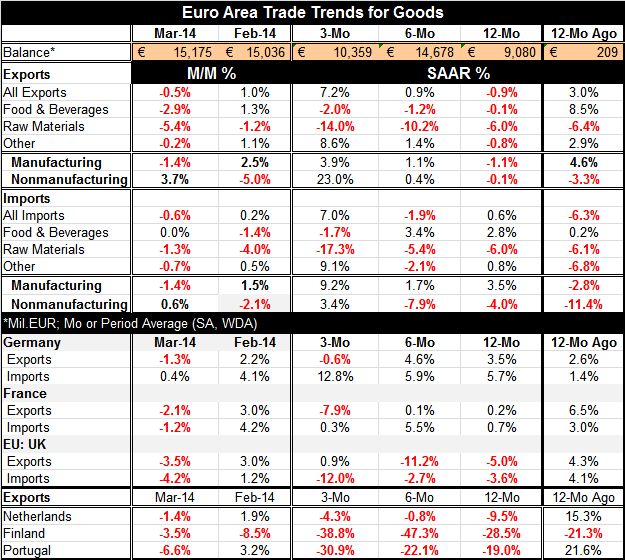

The comprehensive trade data for the European Monetary Union shows a slight increase in the surplus in March compared to February. The trade surplus has increased sharply compared with 12-month average, but it's actually lower than it was in March 12 months ago. Over 12 months, exports have fallen by 0.9% and imports have increased by 0.6%. But trends show both exports and imports gaining momentum with both of them growing about 7% at an annual rate over three months. For imports, that's a pickup from -1.9% over six months while for exports, it's a pickup from a growth rate of 1% over six months. The trade trends for the monetary union have not yet established themselves. The recent acceleration is encouraging but far form decisive.

For manufacturing, exports show acceleration in progress to 3.9% at an annual rate over three months compared 1.1% over six months and -1.1% over 12 months. Manufacturing imports are up 3.5% over 12 months, at a pace of 1.7% over six months and up to a pace of 9.2% over three months. The view of acceleration for imports depends importantly on the three-month growth rate, which can vary quite a lot.

The same trends are true for nonmanufacturing. Nonmanufacturing exports progressed from being flat over six months and 12 months to rising at a 23% annual rate over three months. Nonmanufacturing imports, on the other hand, were contracting at a progressively larger pace, moving from -4% over 12 months, to -8% over six months; they have revived to grow to 3.4% annual rate over three months. Again, this is encouraging, but not decisive.

Both manufacturing and nonmanufacturing exports and imports seem to be following more or less the same trends. So there may be relevant shifts in the growth rates of demand for these products that underlie the individual rates of export and import growth. However, the trends are too fickle to be very sure of. Contrarily, German exports are lower over three months and so are French exports. In addition, for the exports of the Netherlands, Finland and Portugal, all are falling over three months. Finland and Portugal show export drops at a substantial pace.

The unexpected slowdown in the EMU in the first quarter may be taking a toll on these trends. When you look at the exports of the EMU itself, you are looking at exports from countries of the union to outside destinations. However, when we look at the exports of a single country, we include sales to any destination beyond the border, including shipments to EMU members.

It's possible that as of March one of the factors taking a toll on what have become somewhat irregular exports is the program of sanctions placed on Russia. The sharp drop in Finland's exports hints that might be the case. The mild weakness in German exports supports the notion, too. However, it doesn't look like any kind of stepped-up sanctions are planned on Russia. Maybe the worst of this weakness will soon be behind the EMU. Russian troops are backing away for Ukraine and no one really will benefit from further actions there.

Another factor hampering exports has been the ongoing strength of the euro. However, the European Central Bank has its eye on that and is trying to calibrate monetary policy to stop the euro from gaining strength and moving the euro area toward deflation. If it's successful, that would also help exports to regain footing in the months ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief