Global| Jun 21 2007

Global| Jun 21 2007European Retail Sales

Summary

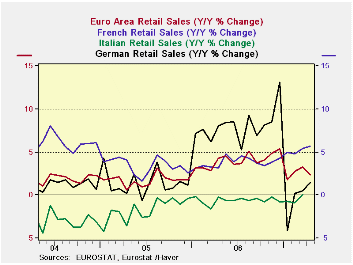

With new figures on retail sales for France and Italy we have a better idea of emerging sales in the Euro area for Q2 2007. With one months data fully out the overall retail volume trend is advancing, even if it is weaker year-over- [...]

With new figures on retail sales for France and Italy we have a better idea of emerging sales in the Euro area for Q2 2007. With one month’s data fully out the overall retail volume trend is advancing, even if it is weaker year-over-year. Euro area retail sales are up at a 3.4% pace annualized in the current quarter-to-date period (April/Q1). That’s a bit slower than the three-month annualized pace of 4.4%, but much faster than the Yr/Yr pace of 1.6% (2.4% for nonfood). France reported consumer spending for manufactured goods for May today and those figures (nominal) showed a drop for the second month in a row. Italy’s sales figures just announced for April (nominal) continue to show a picture of a struggling consumer. Italy’s nominal spending shows a drop in the current month.

While far from weak, the EMU trends are showing some softness as the second quarter gets underway. Manufacturing stats have also showed some off peak performance recently although the new NTC services indicators (PMIs) showed a rebound in today’s release. It is reasonable to question whether manufacturing and some of the foreign orders data are picking up signs of weakness relating to the strong euro. Are services doing relatively better because that sector is more insulated from trade impacts? Certainly EMU exports to the US have dropped off sharply this year. There may be something to the idea that the strong euro is finally taking some toll and consumers can feel it even though the service sector is not yet showing it. Consumer spending patterns do seem to be a bit more erratic – except, of course, in the UK where the MPC is at odds with itself over whether to hike rates again or not.

Germany’s retail trends are still a bit hard to untangle due to the VAT hike that disrupted late 2006 and early 2007 spending. The UK is showing a strong trend in spending and so is France, but the French trend may be in jeopardy due to the slide in spending on manufactured goods by consumers.

The category data for the Euro area is a bit uneven in terms of its timeliness. But we can see that through April the 3-month trends are on an upswing for the total and for the total excluding food. Through March (the shaded area of the table) a slowing in the most recent period is indicated for a broad class of consumer goods, at least in the recent three month period.

The country-level data are quite strong, at least for the large EMU/EU countries. So far it is hard to build a case for encroaching weakness but some signs that growth may be topping permeate the various reports. It’s a good time to watch these reports very closely and to pay attention to revisions.

| Apr-07 | Mar-07 | Feb-07 | 3-Month | 6-Month | 12-Month | |

| Euro area 13 Total | 0.1% | 0.5% | 0.5% | 4.4% | 1.8% | 1.6% |

| Food | 0.4% | 0.4% | 0.3% | 4.5% | 1.8% | 0.9% |

| Nonfood | 0.0% | 0.5% | 0.8% | 5.0% | 2.1% | 2.4% |

| Textiles | #N/A | 0.2% | 1.2% | 2.4% | 7.6% | 6.1% |

| HH goods | #N/A | 1.1% | 0.4% | -5.1% | 2.8% | 5.1% |

| Books news | #N/A | 0.9% | 0.3% | 1.1% | 2.4% | 2.9% |

| Pharmaceutical | #N/A | 0.4% | 0.5% | 1.3% | 3.7% | 3.4% |

| Other Nonspecialized | -0.4% | 0.8% | 1.2% | 0.0% | 1.2% | 2.4% |

| Mail Order | 1.4% | -1.8% | 3.0% | -17.5% | 2.2% | -0.2% |

| Nonfood Country detail: Volume | ||||||

| Germany | 2.1% | 0.0% | 3.5% | 24.9% | 0.8% | 1.4% |

| France | 0.7% | 0.8% | 0.3% | 7.4% | 6.6% | 5.7% |

| Italy (Total Value) | #N/A | 0.2% | -0.1% | -0.4% | -0.5% | 0.1% |

| UK (EU) | -0.1% | 0.7% | 1.7% | 9.8% | 6.7% | 5.9% |

| Shaded areas calculated on a one-month lag due to lagging data. | ||||||

| The Euro area 13 countries are Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Slovenia and Spain. | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

U.K. Headline and Core Inflation Rates Slow Sequentially as BOE Gets Ready to Meet