Global| Jan 22 2016

Global| Jan 22 2016European PMIs Sag in January

Summary

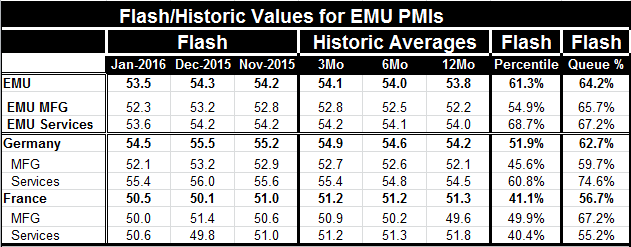

The EMU private sector PMI slipped to 53.5 in January from 54.3 in December. The index is at an eight-month low. Both the manufacturing and services sector PMIs ratcheted lower in January. Manufacturing was last lower in October and [...]

The EMU private sector PMI slipped to 53.5 in January from 54.3 in December. The index is at an eight-month low. Both the manufacturing and services sector PMIs ratcheted lower in January. Manufacturing was last lower in October and the service sector was last lower in May.

The EMU private sector PMI slipped to 53.5 in January from 54.3 in December. The index is at an eight-month low. Both the manufacturing and services sector PMIs ratcheted lower in January. Manufacturing was last lower in October and the service sector was last lower in May.

The sequence of moving averages from 12-mo to 6-mo to 3-mo nonetheless is still moving higher Both manufacturing and services are still gaining momentum on this score.

Germany also posted flash values for January and its headline slipped in addition to slips in both of the sector gauges. Germany's headline and sector gauges are still making headway as momentum is still higher on a moving average basis.

The French flash readings showed an improvement for the private sector overall with manufacturing slipping and services improving. France still does not have upward momentum in its private sector moving average, although manufacturing is showing an ongoing momentum gain.

We can also evaluate these various metrics by the strength of their current standing. The queue standings show that the EMU private sector index stands in the 64th percentile of its historic queue, a moderate position. This reading tells us that the overall private sector is this weak or weaker 64 percent of the time and by implication stronger only 36 percent of the time. Taken separately both components are slightly stronger than this with manufacturing in its 65th percentile and services in its 67th percentile.

For Germany the overall private sector percentile queue standing is in its 62nd percentile. Manufacturing is lagging with a 59th percentile standing compared to services with a 74th percentile standing. In relative terms the German service sector is doing better.

For France the overall private sector index has a 50th percentile standing. Manufacturing has a 67th percentile standing and services has a 55th percentile standing. In France the manufacturing sector is the relative strongest sector.

EMU also reported debt to GDP ratios today. At least the weak growth has been bearing fruit in terms of debt to GDP ratios. The EMU-wide government debt to GDP ratio fell to 91.6% in the third quarter from 92.3% previously. The highest debt to GDP ratio in EMU was recorded as 171% for Greece, with Italy ranked second and Portugal third. The lowest debt to GDP ratio was in Estonia at 9.8%. For the EU-28 the debt ratio decreased to 86% from 87.7% previously.

Debt reduction is taking place and, by putting fiscal policy out of reach, growth is being held back but progress on debt reduction is in train. Still, this policy remains controversial in some places- nowhere more so than in Spain, where Podemos is trying to be part of an active government and seeks to throw off the mantle of austerity there.

All in all Europe has been relatively eventless with yesterday's promise by the ECB that it can do more and that it might step up its actions as the highlight of recent European events- apart, of course, from stock selling which has become a new global pass-time. Migrants continue to be an issue for Europe with bad behavior in Germany getting the most press and some migrants being linked to terrorist acts. There were recent new arrests in Belgium of persons believed to be linked to the Paris attacks. Overnight a new ship of migrants headed for Greece sank with over 40 lives said to be lost. Obviously Europe is still struggling with most of the same issues it struggled with for most of last year. Today's weakening in the flash PMI's reminds us that progress on the economic front remains slow and may not be impervious to recent market-jarring events.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief