Global| Jun 22 2007

Global| Jun 22 2007European Orders Fall by 0.4% in April

Summary

European orders fell by 0.4% in April, less than expected, as bulk orders rose and boosted the headline. And while bulk orders do count they can often blur the trend and mask changes. That is probably the effect right now as [...]

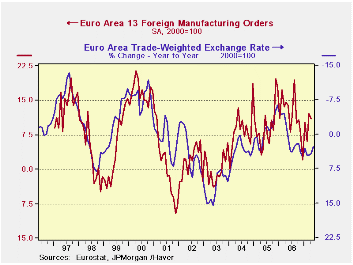

European orders fell by 0.4% in April, less than expected, as bulk orders rose and boosted the headline. And while bulk orders do ‘count’ they can often blur the trend and mask changes. That is probably the effect right now as European industrial orders are headed for a fall while everyone is ignoring that FACT. That’s right, not an opinion, but a FACT of history. The trend for orders GROWTH is already lower and orders GROWTH follows closely movements in the euro exchange rate and follows that inversely. The EURO – broadly defined, weighted by trade and inflation adjusted - has been rising and still is. In terms of its level the EURO is VERY strong. Orders have showed some resiliency. But the chart on the left shows that there always are flares of countertrend movements that eventually prove to be not sustainable. AND orders, while on an upswing, are still contained within the confines of a descending channel much like a rally in a bear chart for bonds or stocks.

For now order trends in the EU are still looking OK (see table). But MFG sales within the Euro area have slowed and slowed sharply for consumer goods and even have slowed for the nearly bullet-proof Capital Goods sector. Domestic orders have showed a sharper fall-off than foreign orders but foreign orders are still obeying the BIG PICTURE law that says with a strong euro they too must fall (it is this series that is plotted on the chart, but the overall series plots almost as well). For the moment two factors are supporting orders in EU. One is this short-term monthly bump up in bulk orders. This sort of thing comes and goes. We expect orders will bulk up from time to time but by smaller amounts moving forward. The other factor is the fact that a lot of the Euro area orders are to non-euro area or aspiring euro area countries that are close by, maintain a tight ‘peg’ to the euro and where historic ties continue to confer advantages to EMU producers. The longer the Euro remains strong, the more likely that competition (apparently the new ‘dirty word’ in the EU) will take hold in such places. Eurol exports to the US already have dropped very sharply. That is a function of slower US growth but also of the nose-bleed euro FX valuations. The strong euro is leaving plenty of ‘fingerprints’ around.

The table shows that on most measures orders growth over the past three months is still pretty strong. In April, however, there are three sizeable declines among the four largest economies in the EU. Of course one of the reasons that the three-month growth rates for these countries are still firm is that in one of the previous months each had a sizeable increase in orders. You cannot hang your hat on any monthly number as evidence of a trend change. Instead we appeal to the chart above.

The chart plots the real broad (trade-weighted) euro VS foreign order performance in the euro area since March of 2000. The relationship is reasonably tight and quite clear: euro up orders down; euro down orders up. Any questions? The euro is up and orders are still in a downtrend although they ‘flared’ to the top of their downward sloping channel this month. Betting that this relationship between orders and the euro will not repeat itself seems to be a grasp at a straw.

Moreover, if we plot orders against the LEVEL of the real exchange rate you see another reason to be a pessimist on order/export strength. The LEVEL of the real FX rate is extremely high. If short term movements in the rate matter, the level surely must matter. Some of the euro’s strength could have been seen in advance and hedged. But the longer the euro stays strong the more that profit margins are squeezed or eliminated and the less help that hedging can offer. We conclude that while it is volatile, the slowing trend in EMU orders is for real. Don’t you?

| SAAR except m/m | % m/m | Apr-07 | Apr-07 | Apr-07 | Apr-06 | Apr-05 | ||

| Euro area Detail | Apr-07 | Mar-07 | Feb-07 | 3-Mo | 6-mo | 12-mo | 12-mo | 12-mo |

| MFG Orders | -0.4% | 2.9% | -0.6% | 7.2% | 8.8% | 9.0% | 9.5% | 4.0% |

| MFG Sales | 0.0% | 0.3% | 0.5% | 3.3% | 6.6% | 6.3% | 7.5% | 2.9% |

| Consumer | 0.0% | 0.0% | 0.1% | 0.4% | 2.1% | 3.5% | 7.5% | 2.9% |

| Capital | 0.4% | 0.6% | 0.7% | 6.8% | 8.2% | 8.1% | 4.0% | 1.3% |

| Intermediate | 0.3% | 0.2% | 0.4% | 5.2% | 5.7% | 7.9% | 7.1% | 2.4% |

| MFG Orders | ||||||||

| Total Orders | -0.4% | 2.9% | -0.6% | 7.2% | 8.8% | 9.0% | 9.5% | 4.0% |

| EA13 Domestic MFG orders | -0.7% | 2.3% | -0.4% | 5.2% | 5.7% | 7.9% | 5.9% | 0.2% |

| EA13 Foreign MFG orders | -1.1% | 4.4% | 0.0% | 13.4% | 13.9% | 11.0% | 14.6% | 3.1% |

| Countries: | Apr-07 | Mar-07 | Feb-07 | 3-Mo | 6-mo | 12-mo | 12-mo | 12-mo |

| Germany | -1.0% | 1.0% | 4.2% | 17.5% | 11.3% | 9.7% | 14.5% | 1.0% |

| France | 2.1% | 5.2% | -7.8% | -3.9% | 12.0% | 18.3% | -0.1% | 1.5% |

| Italy | -1.1% | 4.8% | 0.4% | 17.2% | 4.2% | 2.3% | 15.7% | 2.0% |

| UK | -5.6% | 3.3% | 9.9% | 31.8% | 11.0% | -0.6% | 4.6% | 3.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief