Global| Apr 16 2021

Global| Apr 16 2021European New Car Registrations Remarkably Strong Yet Forgettable

Summary

How can sales be remarkable and yet forgettable? Answer: you only need to look at this month's data to see why or how. Car registrations are not going to be the only statistic that bears these dual and seemingly dueling [...]

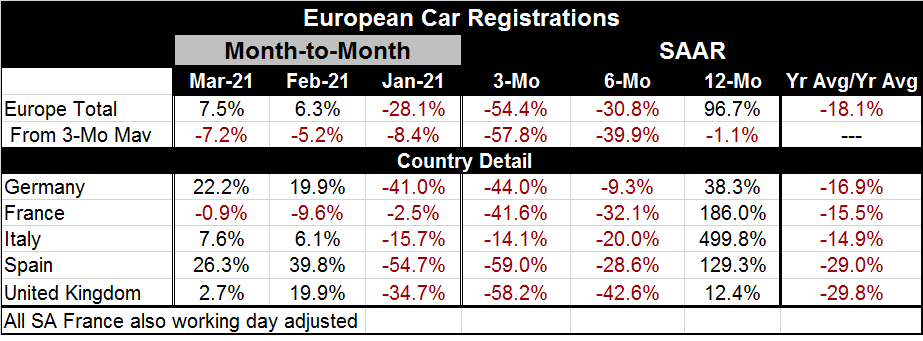

How can sales be remarkable and yet forgettable? Answer: you only need to look at this month's data to see why or how. Car registrations are not going to be the only statistic that bears these dual and seemingly dueling characteristics. The simple answer to this riddle is 'because of base effects.' We will see it coming U.S. inflation statistics where base effects have been much discussed already. We see it in Chinese GDP with a year-on year surge reported; and we see it in European car registrations. We have come to that time in the calendar when virus impact effects are a year in the past. As a result, when we calculate growth from the year-ago depressed base, the current year-on-year growth rate springs to life and to almost unimaginable excess. The 12-month growth rates for registrations in France, Italy and Spain all are in triple digits! Wow! German gains are 'only' 38.3% over 12 months. The U.K. registrations reveal a 12-month gain of 'merely' 12.4%.

How can sales be remarkable and yet forgettable? Answer: you only need to look at this month's data to see why or how. Car registrations are not going to be the only statistic that bears these dual and seemingly dueling characteristics. The simple answer to this riddle is 'because of base effects.' We will see it coming U.S. inflation statistics where base effects have been much discussed already. We see it in Chinese GDP with a year-on year surge reported; and we see it in European car registrations. We have come to that time in the calendar when virus impact effects are a year in the past. As a result, when we calculate growth from the year-ago depressed base, the current year-on-year growth rate springs to life and to almost unimaginable excess. The 12-month growth rates for registrations in France, Italy and Spain all are in triple digits! Wow! German gains are 'only' 38.3% over 12 months. The U.K. registrations reveal a 12-month gain of 'merely' 12.4%.

Total European registrations are up by 96.7% over 12 months. But when we shift the growth calculation away from the base period of 12-months ago. the European growth rate shrinks to -30.8% over six months, and -54.4% over three months (both annualized). These shorter term growth rates are still exceptionally weak as the virus has been recirculating in Europe. These depictions of growth are no match for the year-on year blockbuster rates and it is hard to understand how they can even be related…let along part of the same sequence. But they are. They are all part of virus and post virus and relapse of virus progression of data. Reality continues to be a hard thing to get a grip on.

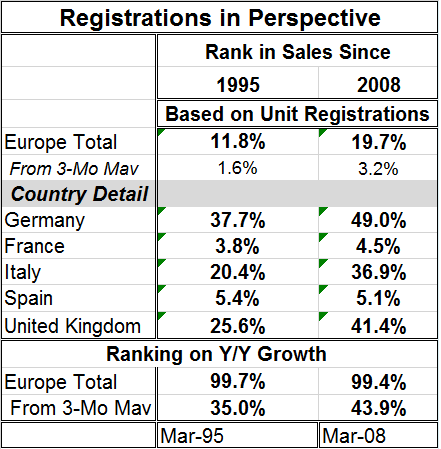

This table (left) offers a different take. It is a device by which to compare the growth rate rankings with selling rate rankings. The differences are remarkable, to say the least.

This table (left) offers a different take. It is a device by which to compare the growth rate rankings with selling rate rankings. The differences are remarkable, to say the least.

The bottom of the table shows ranking statistics based on the year-on-year growth rates and these are eye-poppingly strong with the rank of this month's year-on-year growth rate in its 99.4 queue percentile on data since 2008 and at a ranking of 99.7% on data since 1995. These are strong because they are rankings based on annual growth rates.

But the top portion of the chart uses the same queue ranking concept applied to the 'pace of registrations.' That is the pace expressed in thousands or millions of units. It is the pace of registrations rather than the growth rate. It is a calculation made over one month compared to results gleaned in all other months without regard to a particular base period. When we evaluate registrations based on their pace, the ranking of European sales plummets to a 19.7 percentile standing on data since 2008 and to an 11.8 percentile standing on data since 1995. 'The pace' simply looks at the registration rate over a fixed period (in this case one month) and ranks it against a history of like data. There is no base period as there is with percentage change calculations. Percentage changes are drive by the change in a metric from period one to period two and by the level of the variable in period one.

Of course, the chart at the top of this report already basically told you that in general terms. While you may not be able to discern by the bare eyeball that the trough lows from a year ago begin to form in March, and got even lower in April, that is the case here. The chart does make it crystal clear even with the large jump from the trough lows of 2020 to the current pace, that conditions are not very strong. We have to go back to the early days of recovery from the financial crisis in early-2014 to find the pace of registrations persistently weaker than this month's reading despite the fact that there are now two sizeable monthly increases in a row.

The bottom line for car registrations is that the figure for year-over-year growth is an artifact of the virus and not really relevant to anything else. The recent growth rates over three months and six months both for overall trends as well as for individual countries are disappointing. In contrast, the recent two months of data are encouraging except for France where registrations have declined for three months in a row as well as in seven of the last eight months.

The weakness in car registrations is also reflected in weak retail sales. The consumer sector in Europe is still struggling. The virus is still spreading as well as lurking. And Europe, for the most part, is still lagging in getting vaccinations going. Meanwhile two major vaccines have been halted in various places because of collateral effects that were undiscovered until the products went into mass distribution. Despite the stunning headline on auto registrations, Europe is still struggling. This month's sharp rise in year-over-year sales is not a signal of clear sailing ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief