Global| Oct 14 2016

Global| Oct 14 2016European New Auto Registrations Show Prevarication

Summary

European auto registrations rose in September following a huge gain in August. The August spurt followed a nearly identically massive drop in July. The registration series has become outlandishly volatile. For this reason, we plot [...]

European auto registrations rose in September following a huge gain in August. The August spurt followed a nearly identically massive drop in July. The registration series has become outlandishly volatile. For this reason, we plot vehicle registrations in the raw monthly activity format instead of as percentage changes. Despite the volatility that clearly shows up in the chart, this treatment actually gives a more stable view of the series. What the chart shows is that since December of last year, registrations have been extremely variable even by their own volatile past standards. And there is little sense of uptrend left. If we try to estimate a trend line through monthly sales level data from December on, we get a very poor-fitting result with a negligible R-squared value. In short, the uptrend in auto sales and registrations is fading.

European auto registrations rose in September following a huge gain in August. The August spurt followed a nearly identically massive drop in July. The registration series has become outlandishly volatile. For this reason, we plot vehicle registrations in the raw monthly activity format instead of as percentage changes. Despite the volatility that clearly shows up in the chart, this treatment actually gives a more stable view of the series. What the chart shows is that since December of last year, registrations have been extremely variable even by their own volatile past standards. And there is little sense of uptrend left. If we try to estimate a trend line through monthly sales level data from December on, we get a very poor-fitting result with a negligible R-squared value. In short, the uptrend in auto sales and registrations is fading.

On that same chart, we plot retail sales also in terms of its monthly sales instead of as a percentage change or annualized growth rate. Retailing shows the same slowing pattern we see in auto registrations although it has more consistently showed growth since December. Sales volumes for euro area countries have only recently come to surpass the level of sales attained back in 2007.

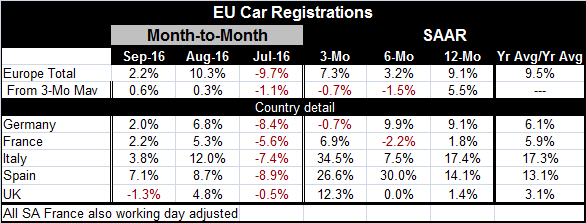

The smoothed growth rates calculated from three-month moving averages show declining registrations over three-month and six-month with year-on-year 'sales' up by 5.5%. The unsmoothed calculations are even stronger (at least for this month) with a 7.3% three-month growth rate and a 9.1% 12-month gain but with a slower rise of 3.2% (annualized) logged over six months.

Country level data show all countries in the table posted sales declines in July, but each country has since posted monthly gains except for the U.K. whose August rise in sales was followed by a 1.3% setback in September.

Over three months, sales gains are strong with Italy and Spain posting massive annualized growth rates of 34% and 26%, respectively. The U.K. reports a rise at a 12.3% pace with French sales up at a 6.9% pace. Only Germany reports a drop over three months.

Over six months, only France reports a slip of 2.2%. Despite the German weakness over three-month, the six-month gain for German registrations is still a sold 9.9%, ahead of Italy's 7.5% pace and ahead of flat sales out of the U.K. However, Spain continues to log a 30% rate of growth in registrations over six months.

Over 12 months, there are gains in all these reporting countries without exception. Italy logs the largest year-on-year gain at 17% followed by Spain at 14%. Germany posts still-strong registrations at 9% while France's gain is a thinner 1.8% and the U.K.'s an even thinner 1.4%.

The consumer has been the backbone of European growth. There is some sign that auto sales in the aggregate and especially when smoothed are slowing down. While scandals at automakers may have damped the mood of consumers to buy a new vehicle, it appears the Volkswagen sales to China may be starting to pick up despite those issues.

As for retail sales, past gains have been solid, but there are signs of some losing momentum in the more recent sales reports. However, fresh trade data for the EMU region for August show an import gain, a potential sign of a pick-up in EMU region domestic demand. Manufactured imports are up by 6.1% in August after a 4.1% drop in July. The three-month growth rate for this group is at a 14.9% annual rate, a clear escalation from its 5.4% rise over 12 months. But the trade data, like vehicle registrations has become a volatile series making it hard to draw conclusions from the month's data.

Volatility in data often is a sign of a turning point or an important inflection point for growth rates. This means that despite the turbulence we should keep a close eye on the economic data. In the U.S., the auto sector has been an important driver of the consumer sector. But vehicle sales in the U.S. have clearly slowed and it makes sense to vet Europe for the possibility of a similar slowing trend. Still, Europe's auto sector is doing well and the level of sales shows a significant recovery. But unlike vehicles sales in the U.S. or even retail sales volumes in Europe, vehicle registrations in Europe are still well short of the sort of selling pace that had prevailed in 2009 and before 2008. That could mean that the sector has much more room to run than in the U.S. Or it could be that Europe has been wounded more than the U.S. in the financial crisis and that a new tighter cap on auto sales will prevail there.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief