Global| Oct 09 2020

Global| Oct 09 2020European Manufacturing Recovery Slows; Everything Goes 'Viral' Except Growth

Summary

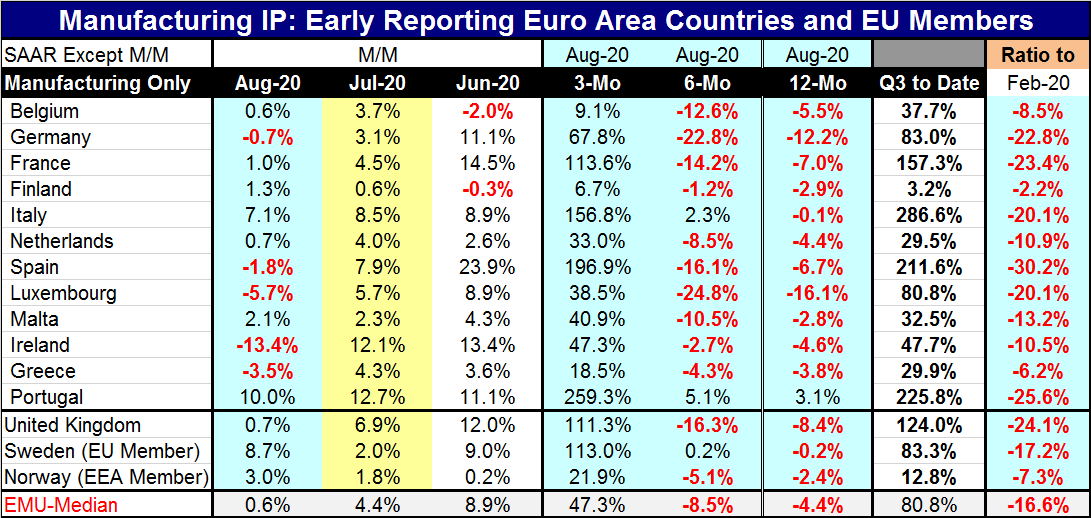

Europe is recovering, but recovery is slowing. In August, 7 of 12 early reporting EMU economies showed increases in industrial production. However, the exceptions were significant as they included two of the four largest EMU [...]

Europe is recovering, but recovery is slowing. In August, 7 of 12 early reporting EMU economies showed increases in industrial production. However, the exceptions were significant as they included two of the four largest EMU economies, Germany and Spain.

Europe is recovering, but recovery is slowing. In August, 7 of 12 early reporting EMU economies showed increases in industrial production. However, the exceptions were significant as they included two of the four largest EMU economies, Germany and Spain.

The notion of slowdown may not seem obvious in the table since there is a clear reversal of weakness in the three-month growth rates that are powerfully strong across all of Europe. In fact, the median of the EMU-twelve country three-month (annualized) growth rates is 47.3%! This follows a median decline of 8.5% over six months and a median decline of 4.4% over 12 months.

However, the monthly data show the slowing quite clearly. There we find a median monthly growth rate of 8.9% in the EMU as of June followed by a gain about half that speed of 4.4% in July and a gain that slows sharply to just 0.6% in August.

This has been the part of the recovery that has been 'V'-shaped. After a stunning, deep, but brief, downturn, the European economy has come roaring back but its roar is now clearly diminishing and the 'V'-shaped part of the recovery process now seems to be over. European growth may even face some questions of sustainability especially as the virus is circulating again in Europe and has caused countries to implement various local programs to stop the spread of it…again. If Europe was more successful in stopping the first phase of the virus, it now looks like it is the U.S. that is more successful in dealing with the second phase or the reflux of it. Don't expect Donald Trump to get any credit for that.

The virus hit Q2 growth in Europe and globally very hard. Now, in Q3, with two months of data in, the quarter-to-date, growth in Q3 has a median pace of 80.8% (annualized) in the EMU. Even so, the recovery is still some ways from being complete.

The far right column in the table looks that the growth in manufacturing IP from February to date. This compares the current index of IP to its value in February. The median short fall of current production from its February pace is 16.6%. The largest shortfall by country is in Spain (-30.2%), followed by Portugal (-25.6%) and by France (-23.4%) then by Germany (-22.8%). The smallest shortfalls are Finland (-2.2%), Greece (-6.2%) and Belgium (-8.5%).

The virus continues to dominate any analysis of the economy and its outlook. The spread of the virus has become a real issue in Europe. France continues to engage in piecemeal shutdowns as more areas around Paris face restrictions such as bar closings and other actions as it struggles to contain the spread. Spain has declared a 15-day state of emergency in Madrid to get control of the virus. In England, the intensity of the spread is rising as the reported R-factor is rising. Europe continues to face a growing problem from the virus. And that means growth is facing a harder-blowing head wind.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief