Global| Feb 10 2015

Global| Feb 10 2015European IP Recovery Shifts to the Core in December

Summary

European industrial output rose in the core EMU countries in December with Germany, France and Italy, the three largest EMU economies showing output gains. Germany and Italy have posted three consecutive monthly gains while France is [...]

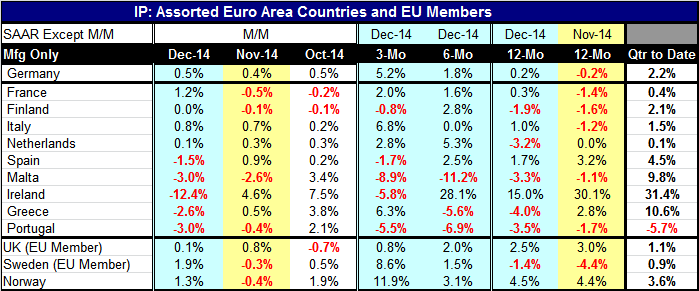

European industrial output rose in the core EMU countries in December with Germany, France and Italy, the three largest EMU economies showing output gains. Germany and Italy have posted three consecutive monthly gains while France is up for only one month. Spain, the fourth largest EMU economy, saw IP fall in December after two months of month-to-month gains. Spain joins Malta, Ireland, Greece and Portugal with IP drops in December.

European industrial output rose in the core EMU countries in December with Germany, France and Italy, the three largest EMU economies showing output gains. Germany and Italy have posted three consecutive monthly gains while France is up for only one month. Spain, the fourth largest EMU economy, saw IP fall in December after two months of month-to-month gains. Spain joins Malta, Ireland, Greece and Portugal with IP drops in December.

Malta and Portugal shows drops over the sequential periods in the table from three-months, from six-months, and from 12-months. Greece shows drops over six-months and 12-months; Finland shows drops over three-months and 12-months.

Germany, France and Italy each show no output drops over each horizon. Germany and France show steady output acceleration over the span. Italy's pattern, while encouraging, is more equivocal.

In the recently completed quarter, output is up compared to Q3 for each member except Portugal where output is falling at a 5.7% annual rate in Q4.

The EU non-EMU members are also showing output gains over the fourth quarter.

We have seen this pattern of stability begin to assert itself recently. It could be that the falling euro is finally having some impact for the EMU more or less across the board.

The plot of the (synthetic euro; extrapolated backward in time with EMU weights prior to the EMU's formation) real effective exchange rate provides a check on the PPP value of the euro exchange rate. PPP, Purchasing Power Parity is a way to assess if the exchange rate is at, above or below its proper (parity) value. PPP is applied to the exchange-rate weighted euro adjusted for prices in the EMU region relative to its trade partners. That index is now BELOW its mean, implying that it is now weaker than it generally has been. This computational device assumes that markets get the exchange rate right over long periods so the index values plotted vs the mean is a rough and ready indicator of the euro's over/undervalued state. The application is to the EMU VALUES as a whole. For individual states, we can modify these results by looking at individual country deviations from the EMU price aggregate. Obviously, since Germany has had the lowest inflation rate and smallest cumulative price rise since the EMU was formed, German competiveness is much better than this. Using the HICP gauge, German competiveness is better than the EMU aggregate by six percentage points. For Germany, there is a great deal of competitiveness in train. For Spain, Portugal and Italy, the euro is probably not quite to what would be parity for them. Still, the exchange rate is moving in the right direction to help all EMU economies and that is probably a factor in the improvement of industrial output trends. The PPP gauge has been falling for two years although the drop in January 2015 is the largest monthly drop of the period. It is obviously motivated by the expectation and announcement of the ECB QE program.

The plot of the (synthetic euro; extrapolated backward in time with EMU weights prior to the EMU's formation) real effective exchange rate provides a check on the PPP value of the euro exchange rate. PPP, Purchasing Power Parity is a way to assess if the exchange rate is at, above or below its proper (parity) value. PPP is applied to the exchange-rate weighted euro adjusted for prices in the EMU region relative to its trade partners. That index is now BELOW its mean, implying that it is now weaker than it generally has been. This computational device assumes that markets get the exchange rate right over long periods so the index values plotted vs the mean is a rough and ready indicator of the euro's over/undervalued state. The application is to the EMU VALUES as a whole. For individual states, we can modify these results by looking at individual country deviations from the EMU price aggregate. Obviously, since Germany has had the lowest inflation rate and smallest cumulative price rise since the EMU was formed, German competiveness is much better than this. Using the HICP gauge, German competiveness is better than the EMU aggregate by six percentage points. For Germany, there is a great deal of competitiveness in train. For Spain, Portugal and Italy, the euro is probably not quite to what would be parity for them. Still, the exchange rate is moving in the right direction to help all EMU economies and that is probably a factor in the improvement of industrial output trends. The PPP gauge has been falling for two years although the drop in January 2015 is the largest monthly drop of the period. It is obviously motivated by the expectation and announcement of the ECB QE program.

Having identified a competiveness underpinning for the EMU IP improvement, we should also note that the G-20 has just today announced that currency wars are a bad thing. Please don't do it. We can expect this admonishment to have no impact on anyone. But it is an admission that exchange rates are working to affect conditions in various economies around the word. It is also an admission that it is a trick that should not be utilized. As we noted in yesterday's report, these exchange rate effects are not always `rational' in the sense that many of them are underlying current account imbalances worse instead of better. At some point, the G-20 may start to worry about what such large imbalances mean for global financial stability. But for the moment, it is every country for itself; they are flailing for something to keep growth alive but at least giving lip service to what the rules of fair-play should be.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.