Global| Jan 07 2020

Global| Jan 07 2020European Inflation Turns Higher...Still Extremely Low; Does Anybody Really Care?

Summary

Unlike the Federal Reserve and most central banks, the European Central Bank operates with a single policy directive. That directive is to keep inflation just under 2%. The Fed has a 2% inflation target but also the mandate to achieve [...]

Unlike the Federal Reserve and most central banks, the European Central Bank operates with a single policy directive. That directive is to keep inflation just under 2%. The Fed has a 2% inflation target but also the mandate to achieve maximum sustainable growth with full employment. Such a directive is often ‘at odds with itself' causing policymakers to make judgement calls that are not really clarified by the policy directive. But this conflict does not enter the realm for the ECB whose duty is clear.

Unlike the Federal Reserve and most central banks, the European Central Bank operates with a single policy directive. That directive is to keep inflation just under 2%. The Fed has a 2% inflation target but also the mandate to achieve maximum sustainable growth with full employment. Such a directive is often ‘at odds with itself' causing policymakers to make judgement calls that are not really clarified by the policy directive. But this conflict does not enter the realm for the ECB whose duty is clear.

Central banks do not control inflation perfectly and until this cycle it was assumed that inflation could be tamed and policy targets hit by rising interest rates. But this cycle brought a new dimension and challenge to policy making: inflation that is chronically too low and unresponsive to interest rates that plunge even to zero and then require added policy ingenuity to try to bring stimulus to the table. Central banks responded by driving rates below zero, using large scale asset purchases (QE) to expand their balance sheets or a shift to special loan programs (LTRO) in addition to in some places yield curve twisting (the U.S.) and yield curve control (Japan). On balance, nothing has been particularly effective. But the drop of the price level has stopped. Inflation continues to undershoot, however.

Europe is faced with a true policy conundrum

The ECB's inflation undershooting continues. And that is now interacting with one of EMU safeguards that no longer looks like such a ‘safeguard.' When the EMU was formed, the union was established as a set of countries with exchange rates fused together but with independent fiscal policies. To insure the union against excessive fiscal expansion, the Maastricht rules were put in place enforced by the EU Commission to limit annual deficits and separately to limit the ratio of debt-to-GDP in each member state. Now when monetary stimulus is failing or has reached its practical limits, countries for the most part find themselves constrained from the use of fiscal policy by the Maastricht rules. Germany has kept its fiscal flexibility, but right now it is choosing to run the opposite strategy, fiscal surpluses.

The surprising deviation by Europe's policy hawks

In this circumstance, we find the policy hawks at the ECB are sticking to their long-term biases. Despite the ongoing ECB inflation undershoot, monetary experts in Germany want the ECB to fold up the tent on negative interest rate policy despite the ongoing inflation undershoot. It is actually a strange position for experts who designed the ECB mandate to assure that the ECB would hit its target and would not be distracted by other events. But here they are looking to remove policies that should act to help the ECB hit its inflation target because they are unconventional and have not been effective enough.

Law of unintended consequences... What to do when your L.U.C. runs out?

Of course, this is the law of unintended consequences at work. The Bundesbank's experts who were the principle designers of the ECB and meant to insulate it from the ‘tampering' of other EMU members who might want to cause the ECB policy to deviate from its long-term path for the sake of policy accommodation. Instead, it is these same experts that are trying to dismantle potentially helpful polices of monetary accommodation because they feel they are inappropriate even though target-missing continues unexpectedly on the downside.

How bad has the target missing been?

From January 1998, the ECB has hit its year-on-year inflation objective only about 25% of the time. Over that period, inflation has run at a compounded a pace of 1.7% with the core HICP rising at a pace of 1.5%. Since the financial crisis from December 2009 to date, the headline and core rates are expanding at a 1.4% pace. All of these results are well below the just under 2% pace that is supposed to define policy. These may not seem like large undershoots, but from 1996 the current month's price level is too low by about 7.5%. From the end-2008, the price level is too low by about 6.8%. There are short falls from an assumed path of the HICP of 2% per year. And these are significant misses.

Yet, policy in Europe is obsessed with the tools of policy instead of the performance of policy. With this episode, it is clear that ECB hawks have no policy purity but instead the same biases as any other policymaker. As much as they touted their rules as the best, they have not been as supportive of hitting the established policy goal which is supposed to be the holy grail of policy when it is missed on the downside. Their real rule seems to be anything less than 2% and that is not what other countries agreed to. The German policy hawks simply display their preference for a conventional policy low inflation and opposition to any monetary innovation.

The current situation

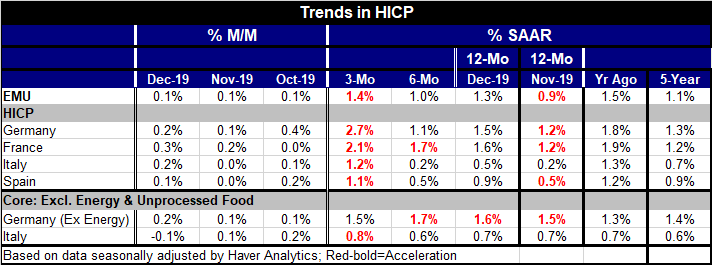

The current policy situation finds headline inflation up by 0.1% in each of the last three months. That is an inflation rate of 1.2% and is well below the just less than 2% mandate. But over three months, the actual inflation increase is at a 1.4% pace; that is down from a 1% pace over six months an only marginally stronger than the 1.3% gain over 12 months. But all of these results have one thing in common: they are all still too weak.

Country performance

German inflation is up by 1.5% over 12 months and French inflation by 1.6%. German inflation eases over six months but like France sees the pace of inflation rise to a pace over 2% over the last three months. Italy and Spain remain as inflation laggards a situation that is almost humorous compared to the inflation conditions in these four countries when the EMU was first formed. Inflation in Spain and in Italy also show some increased pressure over three months compared to 12 months, but their pace for inflation is about half of what prevails in Germany and in France.

Core or ex-energy inflation

Core or ex-energy metrics are provided for Germany and for Italy. In Italy, inflation at the core level is steady and still at an underwhelming pace. In Germany, a hotter economy with exceptionally low unemployment, ex-energy inflation is running at a 1.5% to 1.7% pace over these periods.

Summing up

However, energy prices are being pressured up and we visited those trade-offs yesterday in a discussion of the PPI. Events in the Middle East have created the first worries in a long while that oil supplies could be disrupted. Gold prices have been rising in reaction to the global risks. Today oil prices are backtracking from their recent gains and stocks are making a halting recovery and markets are recalibrating the risks. With the oil price in flux, there is some jolt to what has been a lethargic inflation process. And with this extensive ongoing inflation undershoot, it is now clear that Europe has a real divide in how various members look at monetary policy and in the choices they are willing to make – ECB directive or not. There are both monetary policy Hawks and Doves that are ready to set the agreed rules of the ECB operation and to pursue another agenda from time to time. It remains to be seen how much that reality has affected the monetary union, its stability and the trust that other investors have in it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief