Global| Nov 16 2015

Global| Nov 16 2015European Inflation Remains Low but Its Prices Are not Falling

Summary

If Mario Draghi needed to see continued outright deflation to take more aggressive policy steps, he did not get what he wanted in October. The Haver Analytics seasonally adjusted HICP rises by 0.2% in October while the ECB's own [...]

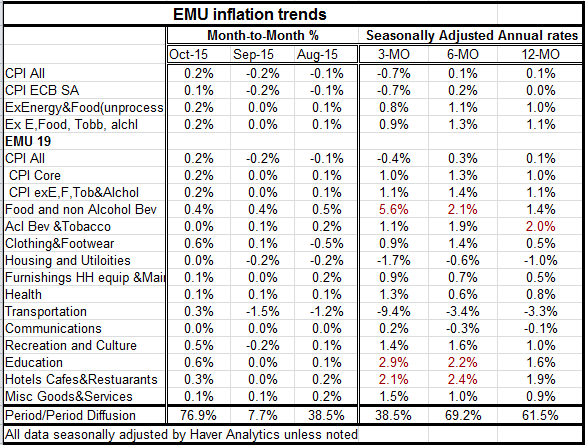

If Mario Draghi needed to see continued outright deflation to take more aggressive policy steps, he did not get what he wanted in October. The Haver Analytics seasonally adjusted HICP rises by 0.2% in October while the ECB's own seasonally adjusted index rises by 0.1% up from its preliminary flat estimate.

If Mario Draghi needed to see continued outright deflation to take more aggressive policy steps, he did not get what he wanted in October. The Haver Analytics seasonally adjusted HICP rises by 0.2% in October while the ECB's own seasonally adjusted index rises by 0.1% up from its preliminary flat estimate.

Still, prices and price trends remain weak. Inflation is still well below the ECBs objective.

We can summarize price trends by looking at trends in the headline and core (excluding energy and unprocessed food). Doing that we see, both the Haver and the ECB headline paces show a weak year-over year performance with falling prices on balance over three-months. Recall that the ECB target is an inflation rate just below 2%. None of these horizons show that that price recovery is in train. Core inflation in EMU is hovering without much trend above and below the 1% mark.

If we ask about what inflation trends are across various commodity groups, the diffusion statistic at the bottom of the table tells part of that story. Diffusion counts up the number of categories where inflation is rising period to period and expresses it as a percentage. That statistic shows widespread month-to-month price accelerations in October with nearly 77% of the categories showing prices rising faster than in September. But September only saw prices accelerating in less than 8% of their categories after accelerating in only 38% in August. The broader sequential data show us still tempered inflation results with diffusion at 38.5% over three-months. Over six months there are more categories with inflation accelerating than decelerating with diffusion at 69%; the same is true over 12 months comparing the current year-over-year inflation rate to the year-ago 12-month gain, that diffusion reading is at 61%, showing some acceleration. So we have one period with inflation decelerating in diffusion terms and two where it is accelerating.

Of course, we want to line up the diffusion readings with the inflation results for the same horizon. When we do this we see the ECB headline series showing some pickup in six months compared to 12-months. But headline inflation is lower over 12-months than it was one-year ago, using either ECB and Haver seasonal adjustment. Diffusion is not tracking period-to-period changes in inflation. When we see that diffusion changes are occurring without much change in the overall inflation rate itself, this may be because the calculated sector inflation changes are small or because changes are occurring in CPI items with small weights in the overall CPI.

When we look at magnitudes we find that out of 12 CPI categories and 3 horizons (3-Mo, 6-MO and 12-MO) there are 36 inflation rates calculated on these horizons. Only seven of 36 are rates are above the ECB mandated pace of 2% for overall inflation. Only four of 12 categories show inflation is on a persisting acceleration. Those accelerating categories are (1) food and nonalcoholic beverages, (2) Furnishings household equipment and utilities, (3) Education and (4) Misc. Goods and Services. Only two categories show steadily decelerating inflation. Those are (1) transportation and (2) alcoholic beverages and tobacco. Overall inflation measures show no clear inflation trends from 12-month to six months to 3-months.

Growth in Europe has been weak but there has been continued growth. There has not been any threat of setback. Unemployment rates are falling on a broad front across the EMU region but those rates have fallen slowly and in most member countries those rates are high in historic comparison. Austerity programs are in play and there are on sporadic problems with compliance in Greece and there may be new issues in Portugal where leftist factions are gaining in popularity and want to stop the policy of austerity there. With the terrorist attack in France there is now a new threat to growth as terrorist attacks can lead to consumers pulling back, and an overall setback to growth. Perhaps this means that it is now more likely that the ECB will launch a more stimulative effort. Inflation in EMU remains subpar and there is nothing in this month's report to suggest that inflation is heading back close to 2% any time soon. We should expect some stepped up effort from the ECB before year-end despite the fact that deflation did not worsen in this report.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief