Global| Mar 04 2016

Global| Mar 04 2016European GDP Reports Begin to Finalize: The End of Good News?

Summary

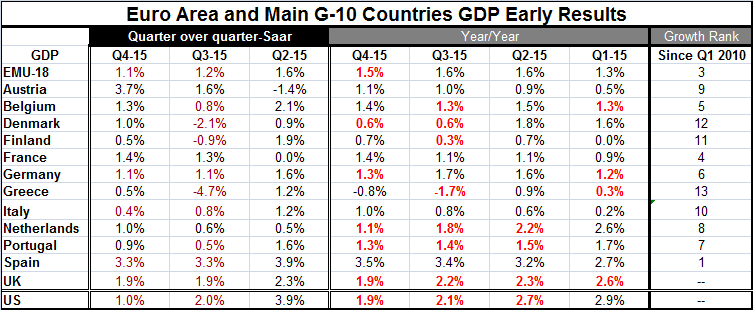

The table contains data from the EMU and for select EMU member countries as well as comparisons with the U.S. Quarterly GDP weakened in only four countries compared to their respective Q3 rates of growth. Year-over-year growth rates [...]

The table contains data from the EMU and for select EMU member countries as well as comparisons with the U.S. Quarterly GDP weakened in only four countries compared to their respective Q3 rates of growth. Year-over-year growth rates eased compared to their Q3 pace in only four countries, but growth also eased in the EMU as a whole. Year-over-year growth is negative only in Greece.

The table contains data from the EMU and for select EMU member countries as well as comparisons with the U.S. Quarterly GDP weakened in only four countries compared to their respective Q3 rates of growth. Year-over-year growth rates eased compared to their Q3 pace in only four countries, but growth also eased in the EMU as a whole. Year-over-year growth is negative only in Greece.

We can look at growth back to early 2010, when growth rates largely turned positive again. On that basis, the countries with the strongest growth rates relative to their own performance during this period are Spain, Italy, the EMU region itself plus Finland, France and Greece. Greece gets in the top echelon despite its still negative growth rate because its growth had been even worse in the earlier part of the period. Growth is weakest relative to its past performance in the U.K. (EU member), Germany followed by Denmark (EU member) and the Netherlands.

Absolute and relative growth performance is generally quite different for this period. However, for the EMU region as a whole, Portugal, Spain, Denmark, France, Austria and the Netherlands, the relative and absolute rankings are quite similar. But the absolute and relative rankings are quite different for the U.K., Greece, Finland, Italy and Germany.

Germany still has relatively strong growth (fifth best overall in absolute terms), but it has the 12th best relative to its history of growth. Germany is an important economy for Europe and it has slowed and now bears more of a burden with a growing migrant population. Germany's growth is no longer as strong relative to its past compared to other EMU members.

All this is just a way to say and to formalize that the growth lineup of European nations is shifting. We are seeing evidence of overall weaker growth in the recent PMI data (through February) and that is a whole different story than the one told in the table of GDP growth rates. Among the countries in the table, only Germany, Denmark and the U.K. have growth rates that run in the bottom 50% of their growth rate queue of data since Q1 2010. However, the PMI data for services and manufacturing tell us that there is more slowing in progress for Q1 2016.

Despite the various country differences, recent EMU quarterly growth rates hover close to 1%. The year-on-year pace at 1.5% is better but still not very impressive. When growth rates are low, the risk of serious consequences from backsliding is more of an ever present danger.

GDP momentum is less of a problem in the euro area. But what is a problem is the global slowdown that has elusive reasons stemming from China's turbulence to oil prices to geopolitical circumstances. Neither monetary policy narrowly defined nor its broader effects, including the induced impact on exchange rates, have been able to wrest Europe from the clutches of weakness. In truth, it's not a European problem as the U.S. and Japan are in the same soup.

Developing economies, China in particular, grew too fast and took too large of market share too quickly. Developed economies turned to the use of debt and leverage to sustain growth, but that was stopped by the financial crisis. In the aftermath, fiscal policy has been shunned and monetary policy extremes have had only a slightly ameliorative impact. As the developing world continues to slow, the output that has been relocated there still supports workers who spend less than in developed countries. Asians in particular have a higher marginal propensity to save so that as output has shifted to Asia and labor payments have been made to Asian workers instead of Western workers, the global multiplier from consumption has gotten smaller. In the early stages, the shift of growth to Asia was not an issue because there was so much investment to compensate. But now that has slowed too. The result is that everybody is slowing for related but slightly different reasons and monetary policy has not been enough to turn the tide. Low rates do not stimulate investment when there is chronic oversupply and demand is slipping. And consumers who fear for their jobs are less induced by low rates. Consumers also have been less induced to spend their savings from low oil prices. Of course, on a global basis, the commodity price drop cuts both ways. It has worsened the slowing in many developing economics that are raw material producers. Low commodity prices are, of course, helpful to consumer nations and hurtful to producer nations. But they also raise uncertainty as no one is sure where prices will settle so any investment project with a large energy component is put in limbo.

These factors explain a lot about why the slowdown has been so stubborn. It is not as simple as using fiscal policy instead of monetary policy although that would be helpful most places (not Japan and not the U.S.). The structural issues have simply painted policymakers into a corner. It may be some time before the paint dries. As we have seen, policy moves have not helped to speed the drying process.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief