Global| Jan 28 2021

Global| Jan 28 2021European Commission Index Backs Off

Summary

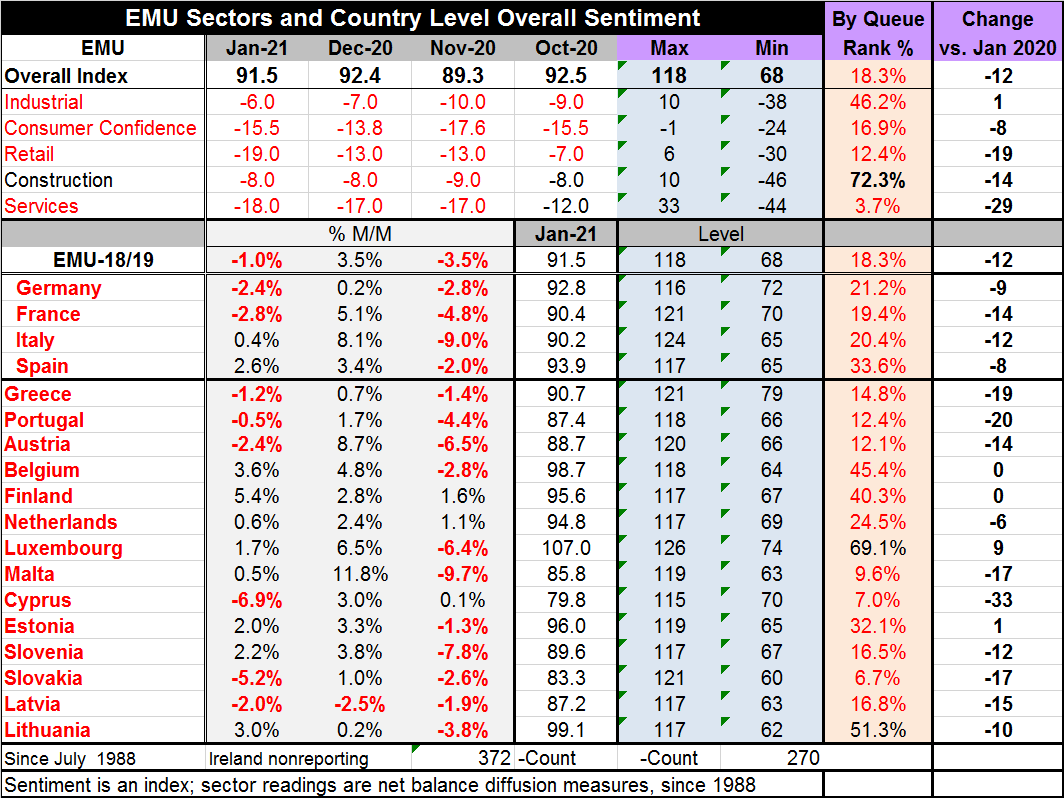

The European Commission Index for the EMU area fell to 91.5 in January from 92.4 in December. It ranks in the lower 18.3% of all indexes released since 1988 (its queue or rank standing). The EMU index fell by 1% month-to-month. Among [...]

The European Commission Index for the EMU area fell to 91.5 in January from 92.4 in December. It ranks in the lower 18.3% of all indexes released since 1988 (its queue or rank standing). The EMU index fell by 1% month-to-month. Among the eighteen early reporting EMU members, eight show month-to-month declines; included in that number are the two largest EMU economies, Germany and France. This follows a month in which only one country took a step back and that followed a month where only three countries logged month-to-month increases. The virus can lead to stop/go policies that do that to the economy.

The European Commission Index for the EMU area fell to 91.5 in January from 92.4 in December. It ranks in the lower 18.3% of all indexes released since 1988 (its queue or rank standing). The EMU index fell by 1% month-to-month. Among the eighteen early reporting EMU members, eight show month-to-month declines; included in that number are the two largest EMU economies, Germany and France. This follows a month in which only one country took a step back and that followed a month where only three countries logged month-to-month increases. The virus can lead to stop/go policies that do that to the economy.

Broad weakness since the virus struck

Of course, the driving force for this volatility and the step back in January is the spread of the virus. EMU member economics have been hard hit - again. The far-right hand column shows the change in the various country- and in EMU-sector indexes since January 2020, just before the virus began to show up on European radar screens. Compared to January, only two EMU members have net stronger EU Commission readings, these are Luxembourg and Estonia, two of the smallest economies in the EMU. However, Belgium and Finland have readings that are unchanged on that timeline. The hardest hit members are in order, Cyprus, Portugal, Greece, Malta and Slovakia, Latvia, France and Austria, Italy and Slovenia, and Lithuania. That list comprises, in order from worst to less-affected, all the countries with double-digit declines in their respective EU indexes from January 2020 to January 2021. Germany, Spain and the Netherlands round out the list of EMU countries with declines as they each have declines in single digits on that timeline.

EMU-wide industry is mostly decaying

Of the five special EMU-wide indexes, four of them show net declines since January. Only the industrial sector has an increase since January 2020 – and that increase is a skinny gain of one point. The services sector has been clobbered, falling by 29 points. Retailing was crushed, dropping 19 points. Construction, the only index with a queue standing above its median (above 50%), still shed 14 points. Consumer confidence, helped by special government support programs, across the EMU region, lost only 8 points.

Most sectors weaken month-to-month

On the month, the industrial sector gains one point with the construction industry unchanged. Consumer confidence, retailing and services weakened month-to-month.

Weak queue standings across the board

Among EMU member countries, only Luxembourg and Lithuania have queue standing metrics above the 50% mark, which puts them above their historic median readings.

Poor momentum...But it's viral-nomics that matter

The graphic does not inspire confidence. Among the four largest EMU members, there is only evidence of an ongoing loss in momentum in train – not much good news. But we know the future is not about economic momentum; it is about the ability to contain and defeat the virus. That fight is on with a number of challenges remaining as new variants of the virus have caused it to spread faster, to become more lethal in some places and morph enough to raise questions about the efficacy of the vaccines already developed. So far, no mutation of the virus has put it outside the realm of containment by the vaccines that have been developed, but that is now one of the new concerns that such a thing might happen.

Risks, rewards… reality

Were the virus to mutate in such a way that developed vaccines were no longer effective, the immunity conferred to date by inoculations or gained through a natural herd-immunity process of infection would go by the boards and leave the whole population at risk to the new strain- partly protected from the old one but vulnerable to the new one. No one wants to go back to square one on virus-fighting. That puts an added premium on speed to shut down the spread before the virus can mutate further. As 2021 begins early in the year, we once again can see the potential of a great risk. However, with a pandemic already in play and a nasty virus already in circulation, there is also the challenge of containing that. With effective vaccines developed, 2020 ended with hope. But as we began to take the steps to use the vaccines, the reality of the difficulty of such a rollout and the limitations of vaccine production plus the potential shiftiness of the virus itself have brought back the reality of facing a challenge with a still uncertain future. Corralling the virus is not just a matter of time. It will be a matter of effort and of luck, hoping that new strains do not arise before the spread can be controlled corralled, and hopefully, eliminated. Meanwhile, stay safe and do your part.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief