Global| Jul 17 2018

Global| Jul 17 2018European Car Registrations Show Modest Rebound

Summary

European car registrations rose by 0.4% in June, a much slower pace than the 5.7% gain in May. Still, over three months, registrations are fading. Over six months, registrations have a strong 14.9% gain. But over 12 months, a [...]

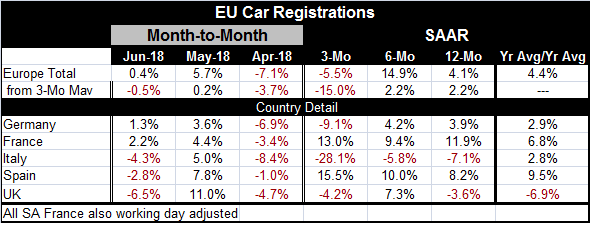

European car registrations rose by 0.4% in June, a much slower pace than the 5.7% gain in May. Still, over three months, registrations are fading. Over six months, registrations have a strong 14.9% gain. But over 12 months, a calculation where seasonality is more effectively muted, registrations are up by 4.1%.

European car registrations rose by 0.4% in June, a much slower pace than the 5.7% gain in May. Still, over three months, registrations are fading. Over six months, registrations have a strong 14.9% gain. But over 12 months, a calculation where seasonality is more effectively muted, registrations are up by 4.1%.

Calculating growth rates from a three-month averages gives a more consistent and weaker picture. On that basis, registrations fall at an annual rate of 15% over three months, then rise at a pace of just 2.2% over both six months and 12 months. European car registrations are slowing.

Country detail shows that sales fell in three of the five reporting nations in June as well as over three months. A ‘super-smoothed’ series that looks at percentages calculated as the most recent 12-month average over the previous 12-month average shows that overall registrations are up at a 4.4% pace on that basis. The data show a strong 9.5% gain in Spain, a 6.8% rise in France, 2.9% growth in Germany, and 2.8% in Italy, compared to a 6.9% decline in U.K. registrations. The super-smoothed data span a period of 24 months and highlight the Brexit impact on vehicle sales in the U.K.

The chart compares the evolution of car registration to the evolution of real retail sales levels in the EMU. Real retail sales seem to have somewhat better momentum over the last year compared to vehicle registrations. Retail sales volumes are still riding their long recovery trends while vehicle registrations have slowed and fallen off that recovery path.

The EU commission indexes show that there is a widespread slowing in the EMU that has been in place for about one year. From early 2016 through early 2017, there has been revival and that helped to motivate the ECB to begin planning for normalcy. But as is often the case, by the time the date for making the policy change crept closer, the economic circumstance of Europe has changed. There is a debate in the U.S. about whether the same forces are at work slowing the U.S. economy or if fiscal policy is going to trump the global weakness and inject strength into the development of GDP. In the U.S. recent data, revisions have made the upcoming Q2 GDP figure loom stronger after a milquetoast Q1. In any event, neither Europe nor the U.S. (nor Japan for that matter) has any inflation as a result of economic revival. However, the U.S. has just recently begun to hit its inflation target after over five years of undershooting. Now we can watch and see how the central bank in the U.S. deals with its new found flexibility since it is no longer behind the eight ball of an annual inflation miss.

The EU commission indexes show that there is a widespread slowing in the EMU that has been in place for about one year. From early 2016 through early 2017, there has been revival and that helped to motivate the ECB to begin planning for normalcy. But as is often the case, by the time the date for making the policy change crept closer, the economic circumstance of Europe has changed. There is a debate in the U.S. about whether the same forces are at work slowing the U.S. economy or if fiscal policy is going to trump the global weakness and inject strength into the development of GDP. In the U.S. recent data, revisions have made the upcoming Q2 GDP figure loom stronger after a milquetoast Q1. In any event, neither Europe nor the U.S. (nor Japan for that matter) has any inflation as a result of economic revival. However, the U.S. has just recently begun to hit its inflation target after over five years of undershooting. Now we can watch and see how the central bank in the U.S. deals with its new found flexibility since it is no longer behind the eight ball of an annual inflation miss.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief