Global| Mar 16 2016

Global| Mar 16 2016European Car Registrations Continue on the Road to Recovery

Summary

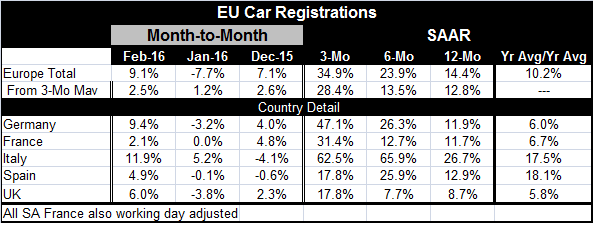

European car registrations rose by 9.1% in February and by 14.4% year-over-year marking another month of strong gains. The propensity for countries to post persistent gains in registrations has been rising as not only the strength of [...]

European car registrations rose by 9.1% in February and by 14.4% year-over-year marking another month of strong gains. The propensity for countries to post persistent gains in registrations has been rising as not only the strength of sales, but the stability of the gains has been improving in its consistency.

European car registrations rose by 9.1% in February and by 14.4% year-over-year marking another month of strong gains. The propensity for countries to post persistent gains in registrations has been rising as not only the strength of sales, but the stability of the gains has been improving in its consistency.

Italy is showing the strongest gains in February (11.9%) and it has the strongest (annual rate) gains over three-month, six-month and 12-month as well. Despite the pollution control scandal at Volkswagen, German registrations are next with a 9.4% gain in February and the second strongest three-month gain (47.1% pace), the second strongest six-month gain (26.3% pace) and the third strongest 12-month pace at 11.9%, just below Spain's 12.9% 12-month gain. France has the weakest sales in the EMU in the table, but U.K sales are weaker than the French sales on the progressive horizon even though U.K. sales are stronger in the month (up 6% in February).

Despite these enormous-looking rates of growth, including the year-over-year gains, vehicle registrations are still below levels that had prevailed before 2008 and the onset of the global recession and financial crisis by about 4.5%.

Still, Europe's story on autos tracks more or less with the U.S. experience which has seen vehicle sales rising more or less continuously in the recovery period and become a steady driver of consumer spending. The difference between Europe and the U.S. at the moment is that the U.S. sales have fully recovered and gotten to an historic peak level that in the past has been hard to sustain. U.S. sales may be reaching a point where auto sales growth will become uneven especially with its reliance on subprime credit and with auto loan delinquencies on the rise. In contrast, Europe's sales are still well below peak levels and sales have continued to power higher even in the face of several scandals including the one in Germany at Volkswagen.

It is far from clear how long the auto sector can continue to lead as it has. An auto purchase is a large multi-year consumer durable acquisition and rising purchases require either ongoing strong economic gains or an increasing willingness on the part of lenders to finance such sales even in less than robust economic times. So far these ingredients have been present in both the U.S. and in Europe. In China, another fast growing auto market, we have seen sales begin to vacillate as China's growth has slowed. The auto sector traditionally is a highly cyclical sector. Ongoing recovery in auto sales/registrations should signal ongoing economic expansion. But should any waffling appear in the sector it could be a sign of uneven economics time to come.

Europe's growth has not been very strong, but it has plugged ahead steadily. Right now the ECB is trying to encourage banks to lend with various support schemes so there may be an appetite for banks and other financial institution to continue to provide auto loans. Despite uneven growth in Europe, vehicle registrations have strong momentum and remain consistent in the main markets, as the table makes abundantly clear. But as a market for a large durable good purchases or an investment good purchase, we should keep our eye on these trends to see if registrations continue to show ongoing robustness or not. The auto sector is not exactly a canary in a coal mine. But it is an important cyclical indicator as well as an important economic sector.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief