Global| Sep 17 2020

Global| Sep 17 2020European Car Registration Comeback Falls Short

Summary

The graph clearly depicts two recent hammer blows to European car registrations. The first came in the wake of the emissions scandals in 2018. The second, of course, is the recent episode with the coronavirus, the ensuing recession, [...]

The graph clearly depicts two recent hammer blows to European car registrations. The first came in the wake of the emissions scandals in 2018. The second, of course, is the recent episode with the coronavirus, the ensuing recession, and the impact of lockdown policies on sales of all sorts of items - including cars.

The graph clearly depicts two recent hammer blows to European car registrations. The first came in the wake of the emissions scandals in 2018. The second, of course, is the recent episode with the coronavirus, the ensuing recession, and the impact of lockdown policies on sales of all sorts of items - including cars.

It is 'too-soon' to conclude that the rebound in sales will fall short of restoring normalcy to sales levels for vehicles, but so far it has not done so and in August the recovery thrust lost momentum and backtracked.

However, this is not necessarily the failure of an incomplete recovery, but it is coming as Europe is being faced with some new virus outbreaks. Today, in fact, WHO issued a warning of 'a very serious situation unfolding in Europe.' Such a warning is not going to be beneficial for European car sales and registrations. As a result, the European Covid-19 recovery may turn out to be much more drawn out.

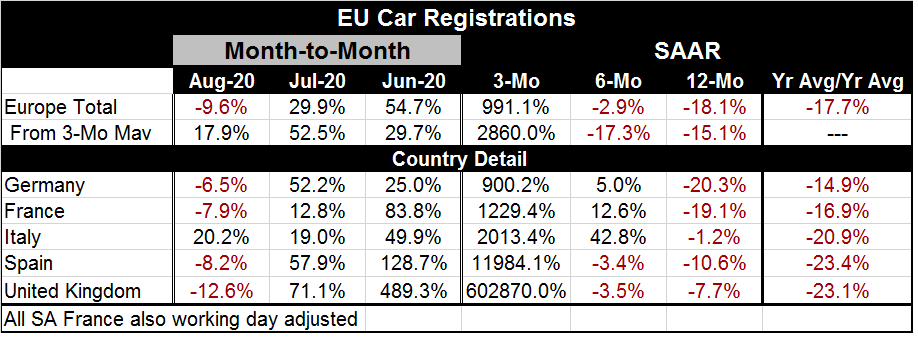

The data table shows a set of results that looks a lot like other series from this time period. There are declines in registrations over 12 months and declines over six months (with some exceptions, but not an exception for the overall gauge). And then there is a moon-shot recovery with growth rates, the likes of which we never usually see even in recoveries…except we are seeing growth rates like these for a lot of economic time-series in Europe and in the U.S. because of the odd nature of this 'cultivated' recession and instant-release recovery. The table shows enormous (and not annualized!) growth rates for June and July registrations across the board. But then August brings a new reality. In August, there are declines 'everywhere' month-to-month except for Italy and except for the smoothed three-month average (no surprise there).

The very, very smoothed series, year-average-over-year-average, which looks at the percentage change of the last 12-month average to the 12-month period prior to that, shows registrations down 17% overall and down by 14% to 23% across individual countries.

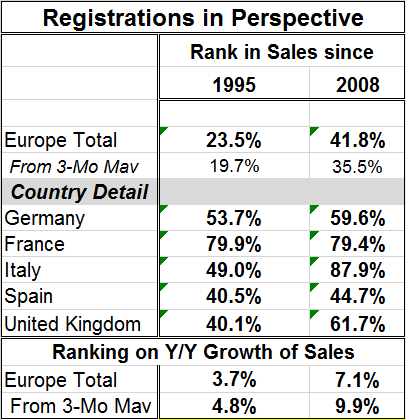

This table presents a ranking of sales for two periods of sales since 1995 and since 2008. Overall sales are stronger over the shorter period (since 2008) but still have only a 41.8 percentile standing below their median. However, the individual countries are mostly above their median for sales since 2008. Spain is the exception.

This table presents a ranking of sales for two periods of sales since 1995 and since 2008. Overall sales are stronger over the shorter period (since 2008) but still have only a 41.8 percentile standing below their median. However, the individual countries are mostly above their median for sales since 2008. Spain is the exception.

Without country detail, I rank the year-on-year growth rate of sales at the bottom of the table. On that basis, sales are extremely weak, in their lower ten percentile or worse in both periods. We know that year-on-year growth rates are negative and that is reflected in these rankings.

Looking ahead, we have this warning form WHO about the COVID-19 situation in Europe being dangerous. Still, there was a pick-up being forecast in a report issued yesterday offered by the OECD. Yesterday the Federal Reserve in the U.S. also upped its outlook for growth. Today the IFW-Kiel forecast takes a slightly less downbeat assessment of the German economy, building on positive statement from the German finance minister yesterday. Change is afoot! There appears to still be two-sided risk in play. Forecasts are being raised mostly on momentum, as performance has begun to turn up sooner or faster than expected. But the virus trumps momentum. If the WHO is right and if the virus has another outbreak in Europe, the method used to contain it is to shut down or otherwise impede the economy and that stops momentum in its tracks. So while forecast upgrades are nice to see, the proof of the forecast will be in the behavior of the virus.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief