Global| Jan 16 2014

Global| Jan 16 2014European Auto Sales Ramp Up

Summary

Auto registrations in Europe rose smartly in December. EU auto sales rose by 5.2% after falling 8% in November and rising 8.3% in October. However, through all that the volatility is clear net gains in auto sales and registrations. [...]

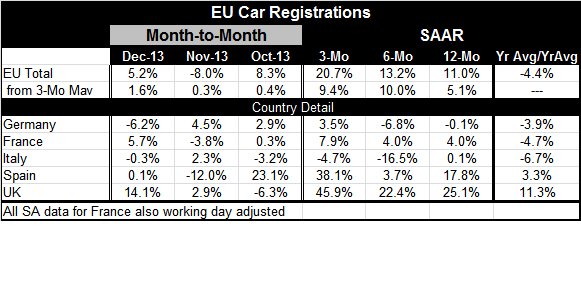

Auto registrations in Europe rose smartly in December. EU auto sales rose by 5.2% after falling 8% in November and rising 8.3% in October. However, through all that the volatility is clear net gains in auto sales and registrations. Over three months EU registrations rose at a 20.7% annual rate. That compares to a 13.2% annual rate over six months and an 11% annual rate over 12 months. Over shorter horizons sales are growing faster, a clear attribute acceleration.

Auto registrations in Europe rose smartly in December. EU auto sales rose by 5.2% after falling 8% in November and rising 8.3% in October. However, through all that the volatility is clear net gains in auto sales and registrations. Over three months EU registrations rose at a 20.7% annual rate. That compares to a 13.2% annual rate over six months and an 11% annual rate over 12 months. Over shorter horizons sales are growing faster, a clear attribute acceleration.

Despite that, intra-year progress sales fell by 4.4% year-over-year (meaning year average over year average) for 2013 compared to 2012. However, it is clear from the pattern that what was really happening was that sales were weak at the beginning of the year and improving later in the year. Looking at the performance of three-month moving averages, sales rose 5.1% over 12 months and then rose at roughly a 10% pace over both three months and six months. Those are good numbers.

Turning to the large countries in the Monetary Union, German registrations fell by 6.2% in December after rising 4.5% in November and 2.9% in October. German sales do not show a clear pattern, however. They are up at a 3.5% annual rate over three months but down at a strong negative pace of 6.8% over six months; yet they are only down a 0.1% rate over 12 months. Still, year-over-year average sales in Germany were down 3.9% which is just slightly faster than their decline in 2012. Germany is clearly an enigma economy. While it has been doing better throughout 2013 as its exports performed and its trade surplus has surpassed China's, domestic expenditures in Germany are not setting the world on fire. Its auto sales in 2013 shrank more than they did in 2012. Germany is an economy much more obsessed with production than with consumption. That makes it unusual and more like Asian economies. German workers who have had severe adverse historic connections to terrible economic climates including hyperinflation have carried in the modern era a willingness to sacrifice for stability.

While France is showing some progress in auto registrations, its year-over-year (average) numbers still show a shrinkage in sales of 4.7%. Registrations in December in France grew by 5.7%, bouncing back from a 3.8% drop in November. Sales in France are gathering momentum as registrations grow to a 7.9% annual rate over three months compared with a 4.0% pace over six months and 12 months.

Italy's registrations were still down a substantial 6.7% for the year average in 2013 compared to 2012. They are showing some signs of progress but certainly not of strength. In December registrations fell by 0.3%, down from a 2.3% gain in November but up from a 3.2% drop in October. Over the last three months Italian registrations fell at a 4.7% annual rate, better than its 16.5% annual rate drop over six months; over 12 months sales have actually eked out a gain of 0.1%.

Spain is a clear success story. Its registrations rose 3.3% year average over year average; a solid gain and the best among the large EMU countries. Spain's sales are still volatile, registrations are up by 0.1% in December after falling 12% in November and rising 23.1% in October. Spain's sales are up over 12 months at a 17.8% annual rate; that tapered off to a 3.7% gain over six months but surged back to a 38.1% gain over three months. Judging from auto sales, Spain has righted itself.

The UK simply continues to pound out great numbers. UK registrations are up 11.3% year-over-year on average data; an extraordinarily strong pace compared to other European countries. The UK gains in December were 14.1%, building on a 2.9% rise in November after a 6.3% drop in October. In the final three months of the year, UK auto registrations expanded at a 45.9% annual rate, up from a 22.4% annual rate over six months and a 25.1% annual rate over 12 months. The UK manufacturing sector continues to perform and the auto sector continues to lead.

The auto sector is important. In the US economy autos have been the one part of the economy, or sales and have continued to push higher through the expansion. An automobile is simply an important thing for the modern consumer. When the economy is healthy, auto sales are good. Therefore, we take this recovery in the auto sector as a positive indication of how the European Union and the Monetary Union are doing.

As we look at the final three months, Italy is only one of the main countries in the euro zone to show sales declines. Even Germany, which had a surprisingly lackluster and weak year - for all the success of its manufacturing sector and improvement in the services sector- managed to put on a gain over the last three months. Auto registrations will continue to be an important indicator of the ongoing expansion of the Monetary Union in 2014. 2013 seems to have ended on a high note.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.