Global| Mar 24 2014

Global| Mar 24 2014Europe Works Its Way Back Toward Normalcy, But Not Without Backsliding

Summary

The trend in the Markit composite PMI for the European Monetary Union advanced further in March even as the monthly readings backtracked to 53.2 from 53.3 in February. The 12-month, six-month and three-month moving averages show a [...]

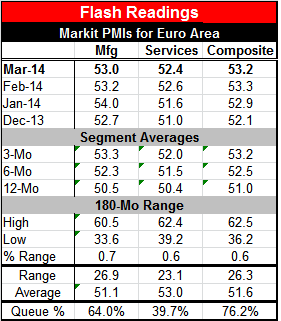

The trend in the Markit composite PMI for the European Monetary Union advanced further in March even as the monthly readings backtracked to 53.2 from 53.3 in February. The 12-month, six-month and three-month moving averages show a clear progression toward stronger values. The overall composite for the euro area sits in the 76th percentile of its historical queue implying that it is higher only 24% of the time, a reasonably firm standing.

The trend in the Markit composite PMI for the European Monetary Union advanced further in March even as the monthly readings backtracked to 53.2 from 53.3 in February. The 12-month, six-month and three-month moving averages show a clear progression toward stronger values. The overall composite for the euro area sits in the 76th percentile of its historical queue implying that it is higher only 24% of the time, a reasonably firm standing.

The readings for the individual sector indices show a slight step back in March. The composite index comes in at 53.2 which also is slightly lower than the 53.3 posted in February.

On balance the progress in the EMU continues to be in force as the progression of the three-month moving average from 12-months to six-months to three-months continues to improve for Germany and France as well as for the composite for the manufacturing index as well as for services.

The composite standing is in the 76th percentile of its historic queue on the border of the top 25%. However, the separate readings for services and manufacturing are weaker; manufacturing in the 64th percentile of its queue and services in the 39th percentile of its historic queue.

The flash reading for Germany backed off slightly this month. However, the good news is the improvement in France. The French overall PMI has moved up to 51.6, indicating expansion for the first time in five months. Its manufacturing index is at 51.9, and its services index is at 51.4. Both France's manufacturing and services indices have moved from an indication of contraction to an indication of expansion in March.

Germany's sector readings show the same a queue standing, the same relative position, for its manufacturing and services sectors, indicating balanced growth. For France its services sector is lagging the improvement in manufacturing; the same is true for the euro area.

The good news is that improvement continues in the euro area and the better news is that it has spread to include France, the euro area's second largest economy and one where growth has been in flux. However, the manufacturing sector continues to lead the improvement and the services sector continues to lag; the services sector is the sector most responsible for job growth which also continues to lag.

Difficulties in the euro area remain. Spain has just seen a large demonstration by people wanting more jobs, more domestic opportunity and less austerity. These sorts of things are going to become more commonplace in the euro area as it moves into recovery and as the core countries surge ahead and the peripheral countries are left behind. Since there is no euro area-wide mechanism to provide assistance to the former austerity countries, they will continue to have some version of austerity imposed. Since that means they will not be able to use fiscal policy to improve the plight of their unemployed workers, there will be continued tensions in the euro area even as it improves.

This reality may not mean that Europe has gone out of the frying pan into the fire. But it means that policymakers are going to continue to have to struggle to deal with unrest among the members of their electorate and from this the euro area itself will see continuing unrest and divisive tensions. How that will interact with the need for political cohesion in the face of the new geopolitical threat on its near-border in the Ukraine is hard to say.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.