Global| May 05 2015

Global| May 05 2015Europe's PPI Gets Ready to Shift

Summary

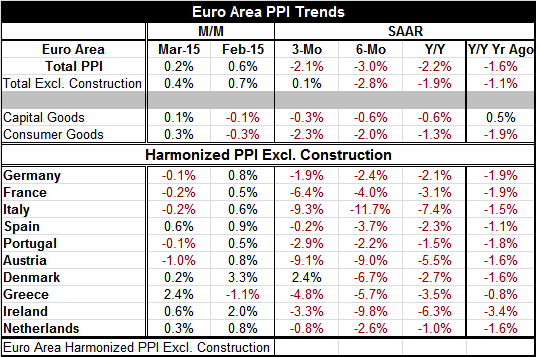

The component year-over-year trends do not show much evidence of a shift in the PPI trend. But in the table it is clear from the monthly data that the period of price declines is coming to an end. This is certainly true unless oil [...]

The component year-over-year trends do not show much evidence of a shift in the PPI trend. But in the table it is clear from the monthly data that the period of price declines is coming to an end. This is certainly true unless oil prices unravel again.

The component year-over-year trends do not show much evidence of a shift in the PPI trend. But in the table it is clear from the monthly data that the period of price declines is coming to an end. This is certainly true unless oil prices unravel again.

Of the ten countries in the table, none of them have price declines in each of the last two months. Half of them have price increases (month-to-month) in March and, of those, four have price increases in both February and March. Inflation is encroaching.

For the EMU as a whole, the PPI is up month-to-month in consecutive readings for March and February. Capital goods and consumer goods prices each are net higher in March after each had posted declines in February.

Still, the past trend shows that price declines dominate the landscape. Of the ten countries in the table, over three horizons: three-month, six-month and 12-month, (a total of 30 observations) there is only one positive entry in the table. That is for Denmark over the three-month horizon as prices rose at a 2.4% annual rate. All other countries/horizons show ongoing price declines.

Only France, Portugal and Austria show price decelerations that are ongoing at an increasing rate of deceleration from 12 months to six months to three months. All other countries show that the rate of decrease in prices slowed over three months compared to six months. For the EMU as a whole, the PPI drop slowed over three months compared to six months and the three-month pace of growth was slightly stronger that its 12-month pace. Germany, Spain, Denmark, Ireland, and the Netherlands also show less price deceleration over three months than over 12 months.

The stage is set for PPI prices to begin to increase. In its deliberations, the ECB tends to look at year-over-year results and those are going to be weak and negative for some months. But over just the last two months the headline PPI is expanding at a 4.8% annual rate. The ECB will be watching these shorter term dynamics as well.

As the ECB begins to reconsider its policy options, it will be looking at the HICP trends, not those from the PPI. But PPI prices are extra-sensitive and generally more volatile that consumer prices so the trends in the PPI are useful as guides to what may lie ahead when trends do change.

The ECB has only just launched its QE program. We could see some EMU members becoming uneasy with this program relatively soon if price developments continue in this upward direction. It is not at all that clear how the ECB will react as prices begin to rise if growth is still very weak. If inflation surpasses 2%, it is clear that the ECB would reverse course on stimulus to meet its price objective. But short of that mark, there is plenty of potential to ponder what the ECB will be doing in the months ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief